How to create your first budget

A budget is a plan to help you manage the way you spend and save your money. If you’ve never created a budget before, here are some tips and steps to get started.

Why make a budget?

A budget could help you save money and may assist in making sure you have the right amount of money to pay for the things you need and want.

Having a budget can help you understand where your money goes – tracking your income (money in) and expenses (money out).

If you want to buy a larger item such as a bike, but you don’t have enough money right now, a budget could help you see how long it will take to save and to get it.

Tools you can use to make a budget

- Pencil and paper: A budget can be as simple as writing it down. It’s a good idea to have a notebook, and you can use a page for each week or month. A ruler and pen or marker will also come in handy to draw lines to separate your income and expenses on either side of the page. Fill in your numbers with a pencil (and have an eraser ready just in case things change).

- Spreadsheet: Programs like Excel or Google Sheets are like digital versions of a notepad. They have squares (cells) that you can type text and numbers into to keep track of your budget on your computer. Ask your parents if you aren’t sure if you have these programs, or if you need help using them.

Helpful Resource: We've already made a budget tracker in Excel that you may use to help manage your money.

Steps to create your first budget

Here are the key parts of a budget. You can line up these sections across the top of your paper or sheet, and then list the amounts and information below each heading:

- Money in: This is also called “income” and includes things like your allowance or pocket money, birthday money or money you may get for doing extra chores.

- Money out: This is also called “expenses” and includes things like buying snacks, going to the movies, or school lunches you pay for on your own.

- Description: List a description of how you earned or spent your money. For example, you can write things like “allowance”, “birthday gift”, “online game” or “lollies”. Adding a description helps you understand your habits and see where your money is coming from or going.

- Date: Adding the date next to the money that comes in and out can also help you look back and remember when you earned or spent money.

Fill in these items throughout the week or month. Once that period ends, you add it all up:

- Add up the money in

- Add up the money out

- Subtract the money in from the money out

You can also include your savings goal on your sheet, to help you see how close you are to reaching it.

And, when you have money saved one month, you can add it to the top of your sheet the next month and watch your money grow!

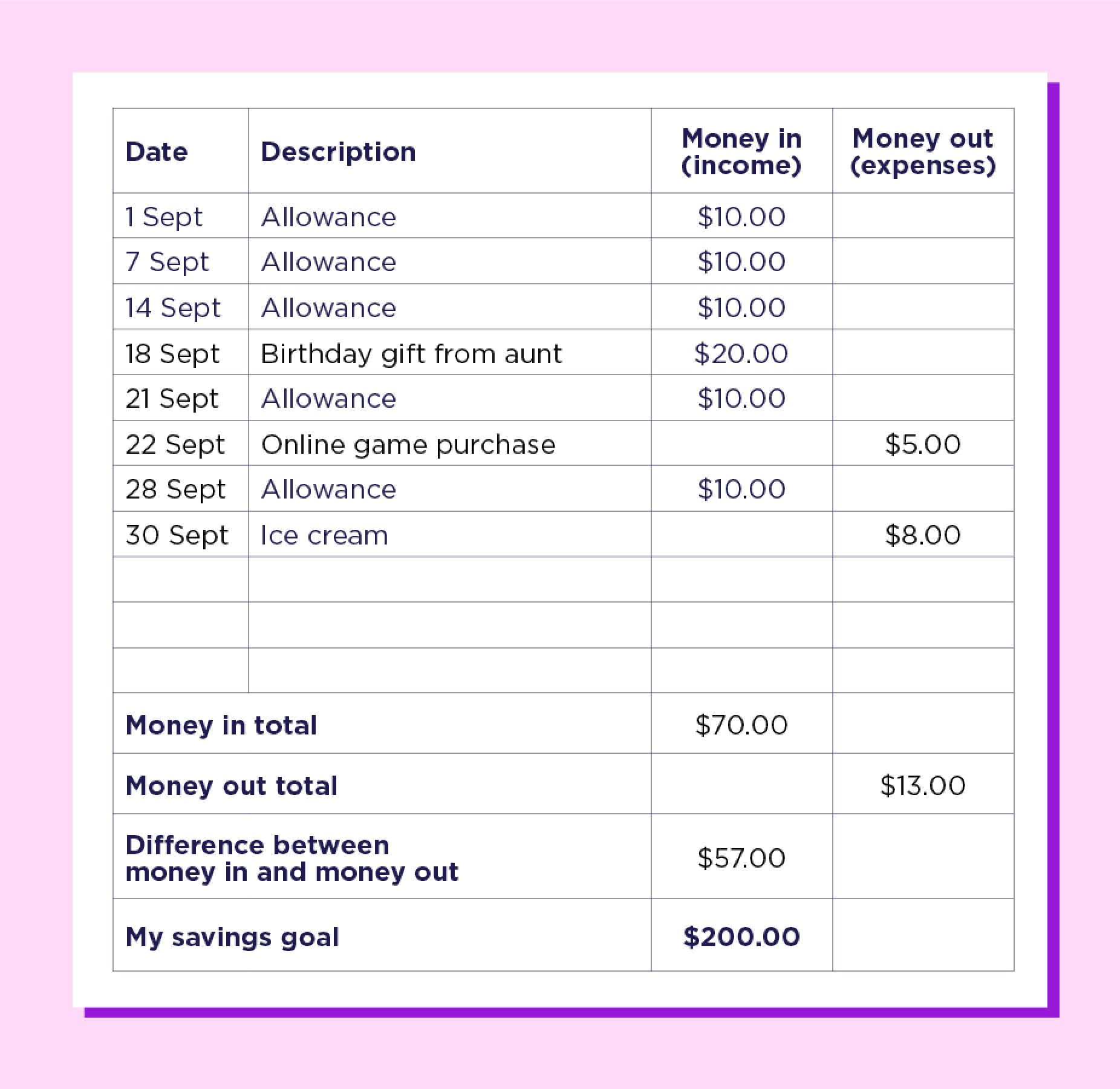

Here’s an example of what a budget looks like on a spreadsheet. You can also follow a similar format if you are writing it down:

In this example, the difference between the money in and out is $57. This means you’ve saved $57 during that month.

When you go to make the next sheet, you can take this amount and put it at the top so that it will be added in the next total.

Fun ways to stay on track

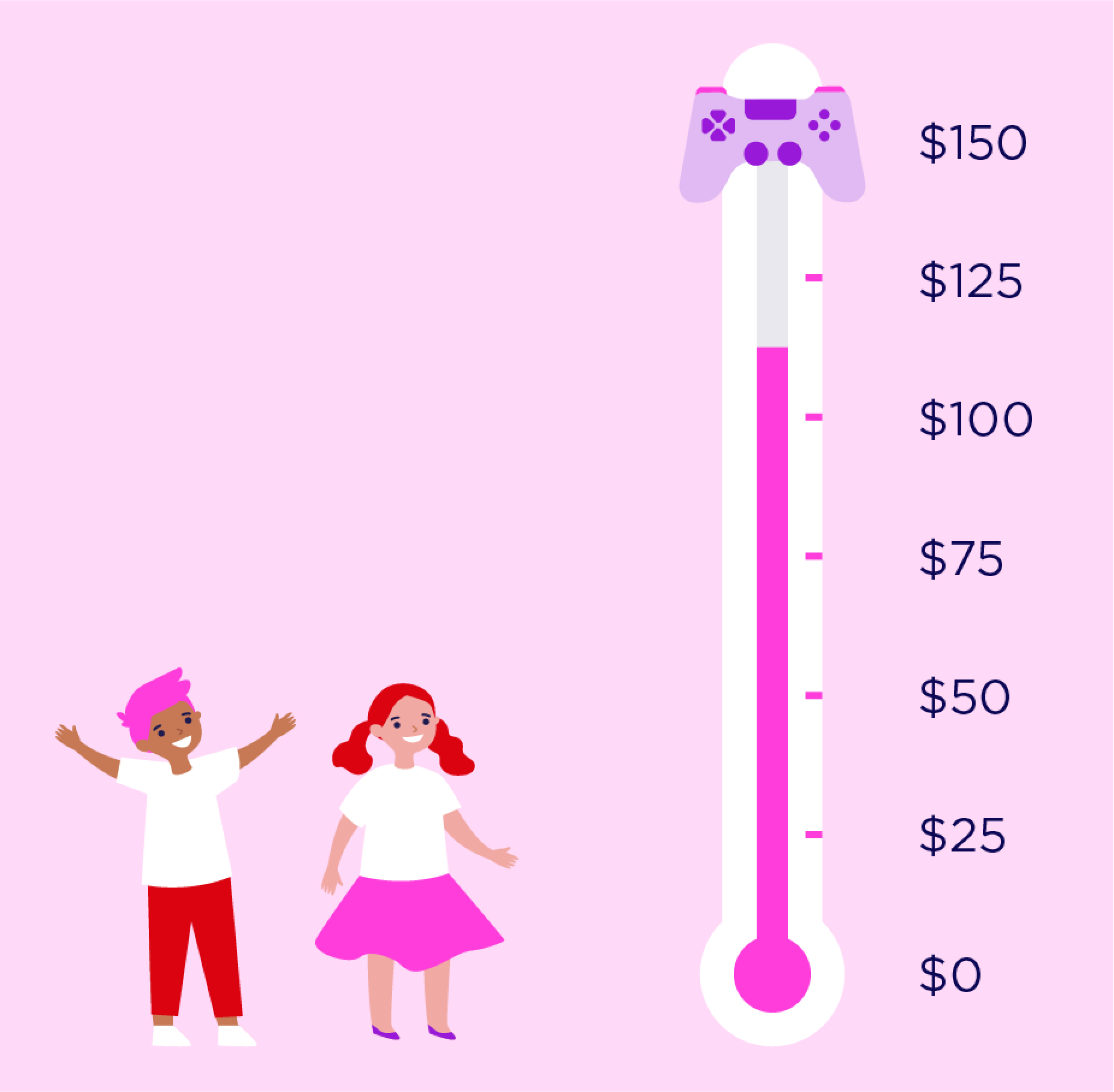

- Savings thermometer: Draw a big thermometer on a piece of paper with the numbers going up to your goal. For example, if your goal is to save $200 you can start with $0 at the bottom and write numbers in intervals of $10 ($10, $20, $30, $40 and so on) all of the way up to the top. Each time you reach a new milestone you can colour in the thermometer up to that point!

- Sticker chart: Similar to the thermometer idea, you can create a chart with milestones ($10, $20, $30) leading up to your goal, and add a sticker every time you hit a milestone.

- Containers: Use envelopes, piggy banks or jars and label them – one for savings, one for spending. It’s fun to watch the savings fill up!

- Westpac tools: If you have a transaction account with Westpac, you can use the Westpac App’s Budget Tools to track your income (money in) and spending (money out). The app also has a Savings goal feature that allows you to create a personalised goal and set up an automatic transfer of money from the transaction account to the savings account.

It’s ok if things don’t go to plan

If you haven’t had as much money come in or you spent more than you expected, remember that things can change and sometimes things can happen unexpectedly.

Take a look back at your budget to understand what you spent more on or why you had less money come in and see if there is anything you can do differently next time.

For example, if you got less money for your birthday than you thought you would, or the cost to catch the bus has increased, these are things you can’t control. But if you got less allowance because you didn’t do your chores, or you spent extra money on snacks — these are things you can consider changing next time around.

Watch: Useful guide on how to save

Saving not only helps you get what you want, but it also means you're prepared for when you might need a bit extra.

Things you should know

1. Bump Bonus interest: You will be eligible for bonus interest if during the month (subject to transaction processing times):

a. your account balance has not fallen below $0; and

b. you (or someone on your behalf) have made a deposit of any amount; and

c. the account balance on the last business day of the month is higher than the account balance on the last business day of the previous month.

Interest paid into your account does not qualify as a deposit in terms of bonus interest eligibility.