Consumer sentiment gets reality check in March index

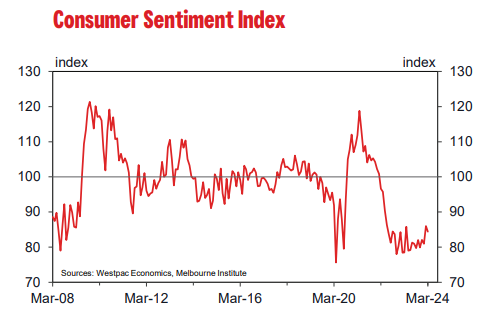

The Westpac Melbourne Institute consumer sentiment index declined by 1.8 per cent in March to a reading of 84.4, from 86.0 in February, remaining in deeply pessimistic territory.

The decline comes as a reality check after a modest pick-up in the index in recent months had offered glimmers of hope that cost of living pressures might be starting to ease.

This latest update shows that improvements are coming slowly and have been offset somewhat by renewed concerns about the economic outlook. The sub-index asking about economic conditions in the next 12 months dropped by 4.5 per cent.

Growth in the December quarter of last year was a sluggish 0.2 per cent, according to national accounts data published in early March, which may have played a part in the weakness we saw in that sub-index.

Inflation is still the dominant concern for consumers.

The March survey included additional questions about which news topics consumers recall and how favourable or unfavourable these were viewed. Inflation remains the topic they remembered most, although recall levels eased below 50 per cent, from highs above 60 per cent seen last year. The negativity around the issue has also become less intense.

Other parts of the survey showed only modest adjustments from the prior month. Assessments of whether now is a good time to buy a dwelling improved a little, even as affordability challenges remain acute for many, while expectations around the labour market were largely unchanged.

Consumers remain uncertain about the path for interest rates and that looks to be the biggest impediment to a faster pick-up in sentiment.

The index reading among those surveyed prior to the Reserve Bank’s March rate decision came in at 94.9, dropping sharply to 79.3 among those questioned after the decision to leave the cash rate on hold.

The implication is that while few would have been expecting rates to be cut, there may have been hopes for a more positive message on inflation and the interest rate outlook. As it turned out, the RBA Governor did not rule out the possibility of further rate rises following the March meeting.

The survey showed 40 per cent of respondents expect mortgage rates to be higher in the next 12 months, with 20 per cent seeing them about the same and 20 per cent expecting them to be lower. So overall, there’s still a degree of edginess around the outlook for RBA policy.

While consumer sentiment remains entrenched in deep pessimism, there are some pockets of society that are feeling a bit more upbeat. People that own investment properties, for example, are net positive, and people in Western Australia are also quite positive relative to the rest of the country.

At the other end of the spectrum, the older age groups and Gen-Xers are feeling less optimistic, which is probably a reflection of poor housing affordability and high debt servicing costs.

Overall, the slight dip in the headline index for March shows that it’s slow going for the consumer as they continue to await an all-clear signal from the RBA on interest rates.

To read Matt’s full report, visit WestpacIQ.