HOME OPEN: Price boom only just begun

Westpac senior economist Matthew Hassan discusses new dwelling price forecasts. (Josh Wall)

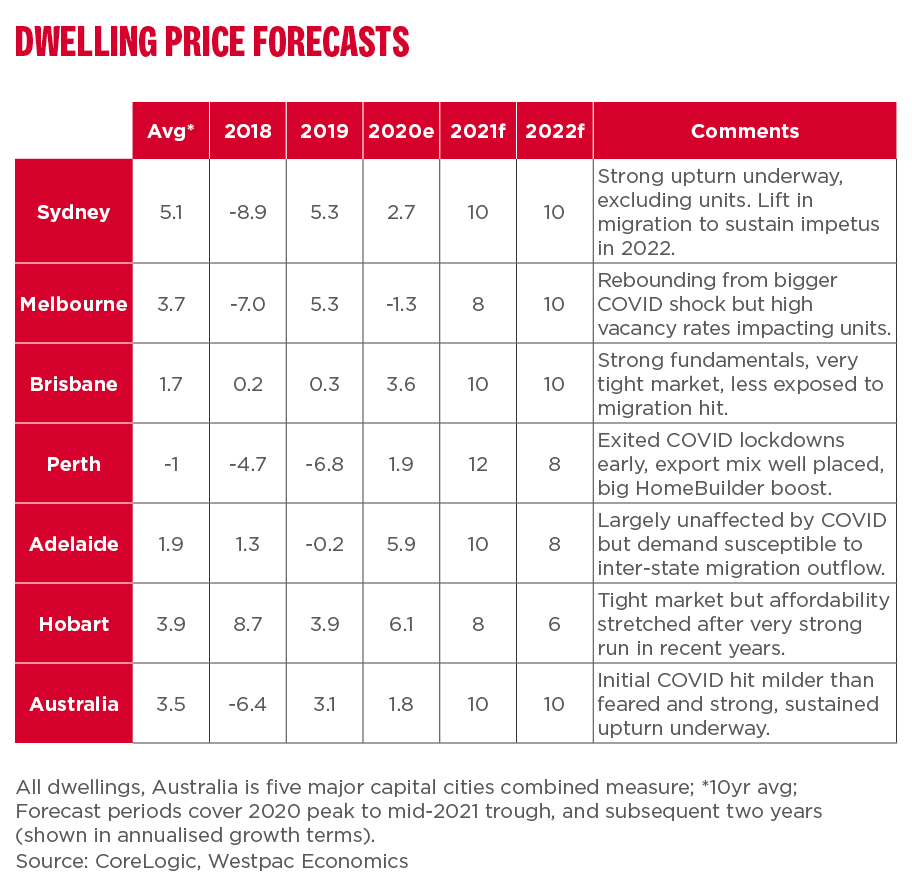

Australia’s housing markets are well and truly on the up, many looking to be in rude health.

Last year’s COVID-19 reopening rebound, which included a significant catch-up for months lost to lockdowns, has given way to a stronger, more broad-based surge as low interest rates fire up demand. Meanwhile, the economic backdrop has also improved as the vaccine roll-outs get underway, central banks are showing little sign of withdrawing their super–stimulatory policy support, credit supply is abundant and many households are cashed up from government supports and not being able to spend as freely as normal.

As our first Housing Pulse for 2021 details, momentum is very convincing with stock on market now very tight in most segments.

In fact, today we revised up our dwelling price outlook with growth now forecast to run at 10 per cent in 2021 and 2022. By 2023, we expect prices to flatten out as rising fixed-term interest rates and macro prudential measures by the Council of Financial Regulators aimed at reining in the associated lift in leverage from the boom cool the market.

But these headwinds are not expected to emerge until 2022 with prudential measures likely to be timed for the second half of 2022.

In the near term, the key risks to our forecasts lie in the questions around the extent to which investor activity lifts and the impact of weak migration inflows. However, both may be bigger issues for the market’s next correction phase rather than the current upswing. Indeed, the key areas of weakness – Sydney and Melbourne high rise markets – now look likely to be a more minor drag on the rest of the broader market.

The bottom line?

The housing market has strong, broad momentum that looks to be lifting further and will remain well supported by monetary conditions and the improving economy.

The information in this article is general information only, it does not constitute any recommendation or advice; it has been prepared without taking into account your personal objectives, financial situation or needs and you should consider its appropriateness with regard to these factors before acting on it. Any taxation position described is a general statement and should only be used as a guide. It does not constitute tax advice and is based on current tax laws and our interpretation. Your individual situation may differ and you should seek independent professional tax advice. You should also consider obtaining personalised advice from a professional financial adviser before making any financial decisions in relation to the matters discussed.