Personal Banking

WHEN IT COMES TO BANKING WE CAN BE YOUR DOUBLE YOU

Explore our range of personal products, tools and resources to help find solutions for you.

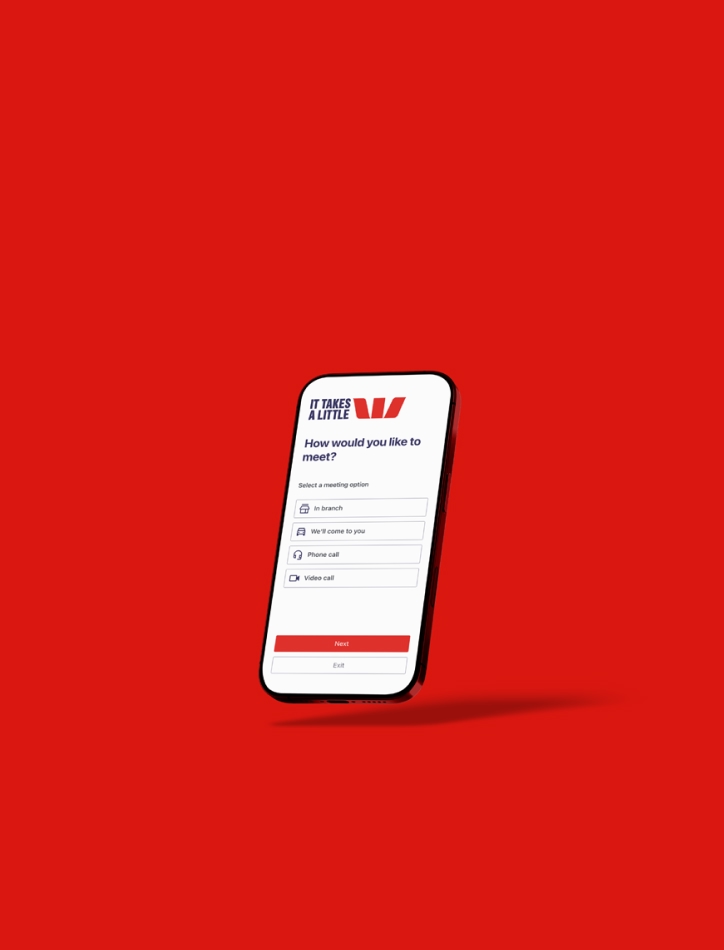

BOOK A HOME LENDER IN MINUTES

DOUBLE YOUR $50

Find, cancel, save

Tools and calculators

Prepare for your next life moment

Investing in property

Buying a car

Moving to Australia

Setting up kids banking

Explore Australia’s Best Banking App^

-

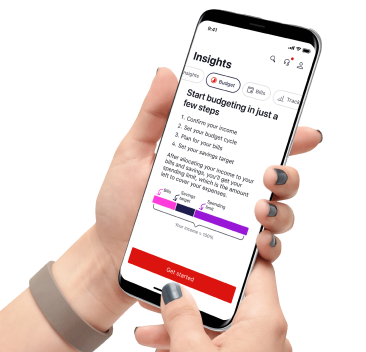

Budget Planner

See your available cash at a glance, organise the day-to-day or save for something special with our Budget Planner tool.

-

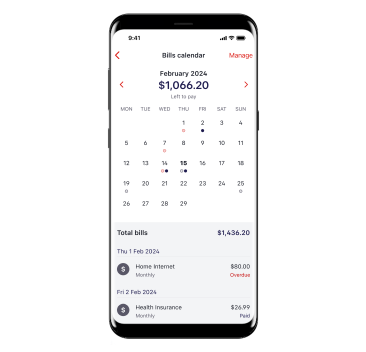

Bills Calendar

Don't miss a payment with Bills Calendar reminders. You can also add, track and review your regular expenses all in one place.

-

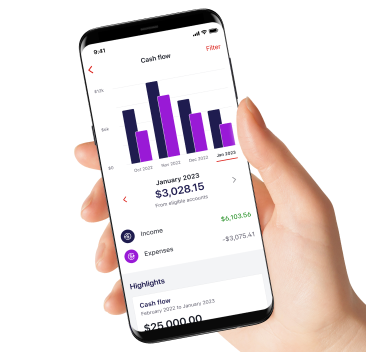

Get spend and cash flow insights

Track your month-to-month Cash flow and spot areas where you could be making savings with your spend sorted in Categories.

Articles to help you make smarter money choices

-

How to avoid shopping scams

Worries about online shopping scams? Follow these six simple steps to help keep you safe. -

Help buying your first home

Let's explore a few tips that may help you pay down your mortgage faster. -

Car finance options

A car loan is only one of serveral ways you can borrow money to buy a car. Look at your options. -

Investment property costs

Tips that could help you make the most of potential profits.

Contact us through the Westpac App

Things you should know

^ This claim is based on The Forrester Digital Experience Review™ of 4 Australian mobile banking apps in Q3 2025. Future findings are subject to change. Forrester does not endorse any company or brand, nor their products or services, nor advise anyone to select them based on this review. If you want to learn more, go to the Forrester website.