How much do you need for a house deposit?

Are you a first home buyer? Work out the deposit you’ll need upfront to meet the purchase price, other costs you need to bear in mind when buying a home, and ways to get into your home sooner.

Are you a first home buyer? Work out the deposit you’ll need upfront to meet the purchase price, other costs you need to bear in mind when buying a home, and ways to get into your home sooner.

The first step in getting a house deposit together to buy your new home is to know what kind of price range you should be looking at. Knowing your price range will mean you can look at a potential home without worrying if it’s within your budget.

Check our Affordability Calculator. It’ll give you a good idea of your borrowing power and the range of property purchase prices that might work for your financial situation. You can also use our repayment calculator to see how interest rate, repayment type and loan term could affect your repayments.

Once you’ve found a house that fits your budget, it’s time to work out what deposit you can put down. A larger deposit means you’ll need to borrow less, which means you’ll pay less interest and potentially lower your monthly repayments.

Usually, 20% of the full value of the house is a good amount to aim for as a deposit. You can still get a loan if you have a smaller deposit, but you may need to take out Lenders Mortgage Insurance (LMI) which adds an additional cost to your loan.

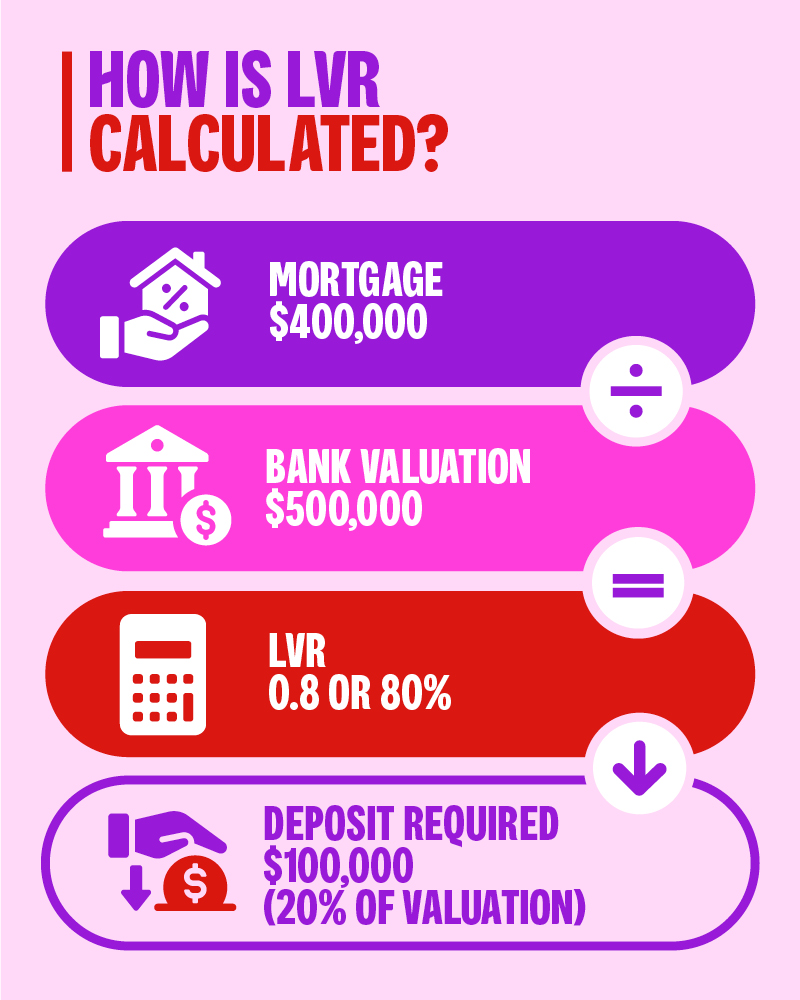

Most lenders will use a loan to value (LVR) calculation to assess the amount they are willing to lend for a home loan. LVR is the amount of your loan compared to the bank’s valuation of your property, expressed as a percentage.

For example, a loan of $400,000 to buy a property worth $500,000 results in a loan to value ratio of 80%. Banks place a limit on the loan to value ratio depending on things such as the type of property, the location and your financial position.

If the bank is lending you anything more than 80% LVR, you’ll generally need Lenders Mortgage Insurance.

| Example of deposit amounts | ||

|---|---|---|

| Full value of property | Minimum deposit | |

20% (no Lenders Mortgage Insurance) |

5% (with Lenders Mortgage Insurance) |

|

| $600,000 | $120,000 | $30,000 |

| $500,000 | $100,000 | $25,000 |

| $400,000 | $80,000 | $20,000 |

| $300,000 | $60,000 | $15,000 |

We may count 100% of your overtime and allowances to improve borrowing power and for medical practitioners, help you get into a home with a smaller deposit. Eligibility criteria applies.

There’s more to buying a home than just the cost of the house itself. There are some other upfront costs you’ll need to know about.

Stamp duty is a state and territory government tax that can fluctuate depending on things such as location, whether it’s a first home or an investment, and the price of the property. It’s important you take this into consideration when looking to buy a property – our Stamp duty calculator can help give you an idea of how much this may be.

Several legal steps are involved when buying property. Conveyancing (the sale and transfer of real estate) can include a property and title search, the review and exchange of the contract of sale, the transfer of the title, and other aspects too.

These can depend on the state or territory in which you live and who your lender is. Knowing whether these apply to you is also important. Find out more about the upfront costs of buying a home

Now you know your price range, how much you need for your deposit, and the other potential upfront costs. In addition to these, there are a few other factors that may affect the amount a lender is willing to loan you and the interest rate they might charge.

Your credit report and credit score help lenders assess your ability to repay and manage credit, which can affect the size of the loan and the interest rate. A higher credit score can see larger loans at lower rates, while a lower score might see the opposite.

Having a savings plan to help accumulate your deposit is a good way to show you can meet home loan repayments – also, make sure you’re making regular repayments on credit cards or other credit products you have, to help increase your credit score.

The government has a one-off payment that can be made to first-time home buyers, helping them towards their first home. The amount, criteria and details for a First Home Owner Grant vary across states and territories, so check with your lender or have a look at the Federal Government’s First Home Owner Grant site for more information.

Most lenders require a deposit of at least 20%, making saving for a deposit a real barrier to home ownership. With the Australian Government-initiated Home Guarantee Scheme, first-time home buyers could fast-track home ownership dreams with one of three guarantee options1.

For those with deposits less than 20% of the property’s value, Lenders Mortgage Insurance can help you.

Find out more about the potential costs you need to consider when buying a home.

You could become a homeowner sooner with government-backed grants and schemes when applying for your home loan.

Conditions, credit criteria, fees and charges apply. Residential lending is not available for Non-Australian Resident borrowers.

This information is general in nature and has been prepared without taking your personal objectives, circumstances and needs into account. You should consider the appropriateness of the information to your own circumstances and, if necessary, seek appropriate professional advice.

Any tax information described is general in nature and it is not tax advice or a guide to tax laws. We recommend you seek independent, professional tax advice applicable to your personal circumstances.

1You can find more information on the Scheme website.

Lenders mortgage insurance (LMI) is issued to Westpac Banking Corporation ABN 33 007 457 141 (Westpac) and insurers Westpac (it is not insurance you take out). This information does not take into account your personal circumstances. Terms, conditions and limitations apply.