Australian businesses have built up strong buffers to withstand choppy economic conditions ahead, while still keeping an eye out for growth opportunities, according to Westpac’s analysis of financing trends.

Small and medium-sized enterprises have been preparing for tough times by paying down debt where possible, increasing their liquid assets, maintaining credit lines and investing in their productive capacity, the snapshot from Westpac’s business banking team shows.

Cash deposits are about 15 per cent higher than pre-pandemic levels, partly reflecting the need for more working capital to meet higher operating costs but also an indication of robust balance sheets.

“Businesses are entering this economic slowdown from a position of strength,” says Shane Howell, managing director, business lending at Westpac. “They know their businesses better than ever after weathering the storm of COVID: They’ve had to learn and redefine every cost line, every input, every output.”

Shane Howell, head of business lending at Westpac. (Supplied)

There’s no doubt that the Reserve Bank’s aggressive series of interest rate hikes – lifting the cash rate by 4 percentage points in a little over a year – is hurting some parts of the economy.

As a result of these rate hikes, interest costs for businesses are up around 20 per cent from pre-pandemic levels, the Westpac data shows.

Businesses are also grappling with high input costs, which have risen as much as 30 per cent since the December quarter of 2019, and ongoing labour shortages.

“Despite pressures on input costs from rising inflation, business deposits have grown and our measure of businesses’ liquidity is around 30 per cent above pre-pandemic levels” says Besa Deda, chief economist at Westpac’s business bank and a co-author of the report.

In these challenging times some companies will have to make tough choices, Howell says, but he adds that the fittest firms will still find opportunities to grow.

“Businesses that are well managed, with a product mix that suits the economic environment, will take these opportunities now. They’ll look for distressed assets, they’ll look for a chance to take out a competitor. So you’ll still see plenty of activity, because this is when the cream rises to the top.”

He also sees a nuanced picture across the economy.

“You can’t look at whole sectors and make broad brush assumptions, everything is moving at different paces,” Howell says.

On the surface, the retail sector will struggle as households cut back their spending, but that will have a much bigger impact on discretionary items, such as fashion or electronics, while people will still need to buy their everyday groceries.

In travel and leisure, the high cost of international travel might mean Australians postpone that big overseas trip and opt to holiday closer to home, offering a boost to local operators.

Primary healthcare and pharmaceuticals are other areas Howell expects to perform well, even in a slowdown.

“Primary health has never been more important to all of us. COVID has shone a light on how much we all genuinely care about our health and well-being.”

Howell says demand is still robust across a broad range of business loans.

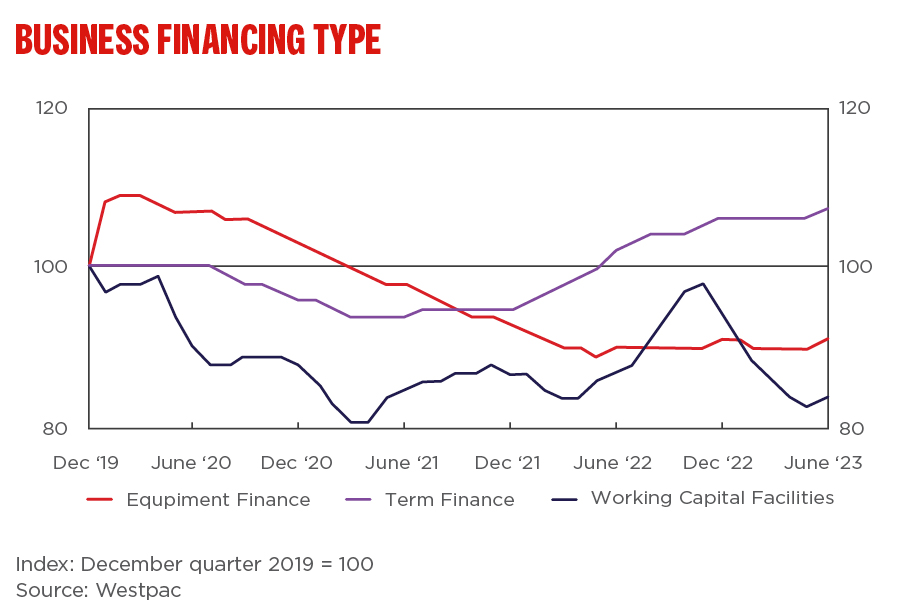

That’s supported by the Westpac report, which shows an upturn in demand for longer-term borrowing, while working capital loans have become less important in the SME funding mix - an indication that businesses are borrowing to invest rather than to operate.

Meanwhile, the share of approved lending that SMEs are using is around its lowest level since 2018, meaning they have a relatively large stock of funding available to draw on as the economy fluctuates.

“Usually, one of the first signs of stress is a big upturn in overdrafts, but we haven’t seen that yet - that’s a really positive sign,” says Howell.

The snapshot uses aggregated and de-identified data from around half a million Westpac small to medium-sized business customers, and was compiled by business bank economists in collaboration with Westpac’s data science and innovation team.

While it’s hard to predict how the economy will evolve in the months ahead, there are two business trends Howell will be watching closely.

First is the high level of inventories.

“Wholesalers have record levels of inventories: businesses need to clear stock, they’re seeing consumer demand fall away and a lot of them are trying to push product.”

That could lead to hefty discounting, which will help the RBA in its battle to contain inflation.

On the other hand, savings rates also rose to record levels during the pandemic as lockdowns restrained spending, while households also took the opportunity to get ahead on their mortgage payments.

“In aggregate, there’s still a lot of money that needs to be eaten away before you work through those buffers.”

James Thornhill was appointed as editor of Westpac Wire in May 2022. Prior to joining the bank, he was a business and financial journalist with more than two decades of experience with international newswires. Most recently, he was a resources correspondent for Bloomberg, covering the mining and energy sectors, and previously reported on a broad range of topics from economics and politics to currency and bond markets. Originally from the UK, he’s had stints working in London, New York and Singapore, but is now happily settled in Sydney.

{"topicSelector":[{"tagId":"newsroom:topics/economy","name":"economy","description":"Explore more Economy insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Economy","url":"/news/topic.economy/"},{"tagId":"newsroom:topics/banking","name":"banking","description":"Explore more Banking insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Banking","url":"/news/topic.banking/"},{"tagId":"newsroom:topics/digital","name":"digital","description":"Explore more Digital insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Digital","url":"/news/topic.digital/"},{"tagId":"newsroom:topics/workplace","name":"workplace","description":"Explore more workplace insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Workplace","url":"/news/topic.workplace/"},{"tagId":"newsroom:topics/diversity","name":"diversity","description":"Explore more Diversity insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Diversity","url":"/news/topic.diversity/"},{"tagId":"newsroom:topics/sustainability","name":"sustainability","description":"Explore more sustainability insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Sustainability","url":"/news/topic.sustainability/"},{"tagId":"newsroom:topics/community","name":"community","description":"Explore more community insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Community","url":"/news/topic.community/"},{"tagId":"newsroom:topics/technology","name":"technology","description":"Explore more Technology insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Technology","url":"/news/topic.technology/"},{"tagId":"newsroom:topics/property","name":"property","description":"Explore more Property insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Property","url":"/news/topic.property/"},{"tagId":"newsroom:topics/innovators","name":"innovators","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Innovators","url":"/news/topic.innovators/"},{"tagId":"newsroom:topics/sme","name":"sme","description":"Explore more Small Medium Enterprise insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"SME","url":"/news/topic.sme/"},{"tagId":"newsroom:topics/westpac","name":"westpac","description":"Stories featuring Westpac corporate news.","title":"Westpac","url":"/news/topic.westpac/"},{"tagId":"newsroom:topics/leadership","name":"leadership","description":"Explore more Leadership insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Leadership","url":"/news/topic.leadership/"},{"tagId":"newsroom:topics/covid19","name":"covid19","description":"Stories influenced by the COVID-19 pandemic.","title":"COVID-19","url":"/news/topic.covid19/"},{"tagId":"newsroom:topics/investing","name":"investing","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Investing","url":"/news/topic.investing/"},{"tagId":"newsroom:topics/startups","name":"startups","description":"Explore more Startups insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Startups","url":"/news/topic.startups/"},{"tagId":"newsroom:topics/agribusiness","name":"agribusiness","description":"Explore more Agribusiness insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Agribusiness","url":"/news/topic.agribusiness/"},{"tagId":"newsroom:topics/billsbites","name":"billsbites","description":"Explore more insights from Bill Evans at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Bill\u0027s Bites","url":"/news/topic.billsbites/"},{"tagId":"newsroom:topics/data","name":"data","description":"Explore more data insights at Westpac Wire.","title":"Data","url":"/news/topic.data/"},{"tagId":"newsroom:topics/personalfinance","name":"personalfinance","description":"Explore more insights about personal finance, financial literacy and financial wellbeing. ","title":"Personal finance","url":"/news/topic.personalfinance/"},{"tagId":"newsroom:topics/payments","name":"payments","description":"Explore more Payments insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Payments","url":"/news/topic.payments/"},{"tagId":"newsroom:topics/environment","name":"environment","description":"Explore more Environment insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Environment","url":"/news/topic.environment/"},{"tagId":"newsroom:topics/fintech","name":"fintech","description":"Explore more Fintech insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Fintech","url":"/news/topic.fintech/"},{"tagId":"newsroom:topics/scams","name":"scams","description":"Stories about the latest cyber scams news and trends. ","title":"Scams","url":"/news/topic.scams/"},{"tagId":"newsroom:topics/politics","name":"politics","description":"Explore more Politics insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Politics","url":"/news/topic.politics/"},{"tagId":"newsroom:topics/regulation","name":"regulation","description":"Explore more Regulation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regulation","url":"/news/topic.regulation/"},{"tagId":"newsroom:topics/career","name":"career","description":"Stories providing career insights, tips and trends.","title":"Career","url":"/news/topic.career/"},{"tagId":"newsroom:topics/social-enterprise","name":"social-enterprise","description":"Stories relevant to or featuring social enterprises.","title":"Social enterprise","url":"/news/topic.social-enterprise/"},{"tagId":"newsroom:topics/indigenous","name":"indigenous","description":"Explore more indigenous insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Indigenous","url":"/news/topic.indigenous/"},{"tagId":"newsroom:topics/superannuation","name":"superannuation","description":"Explore more Superannuation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Superannuation","url":"/news/topic.superannuation/"},{"tagId":"newsroom:topics/wellbeing","name":"wellbeing","description":"Stories featuring wellbeing trends, insights and stories.","title":"Wellbeing","url":"/news/topic.wellbeing/"},{"tagId":"newsroom:topics/reinventure","name":"reinventure","description":"Explore more Reinventure insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Reinventure","url":"/news/topic.reinventure/"},{"tagId":"newsroom:topics/westpac-scholars","name":"westpac-scholars","description":"Stories featuring Westpac Scholars. ","title":"Westpac Scholars","url":"/news/topic.westpac-scholars/"},{"tagId":"newsroom:topics/asia","name":"asia","description":"Explore more Asia insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Asia","url":"/news/topic.asia/"},{"tagId":"newsroom:topics/podcast","name":"podcast","description":"Explore Westpac Wire\u0027s podcast series.","title":"Podcast","url":"/news/topic.podcast/"},{"tagId":"newsroom:topics/businesses-of-tomorrow","name":"businesses-of-tomorrow","description":"Stories featuring Westpac Businesses of Tomorrow program winners. ","title":"Westpac Businesses of Tomorrow","url":"/news/topic.businesses-of-tomorrow/"},{"tagId":"newsroom:topics/history","name":"history","description":"Stories unearthed from Westpac\u0027s private archival collection. ","title":"History","url":"/news/topic.history/"},{"tagId":"newsroom:topics/tax","name":"tax","description":"Explore more tax insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Tax","url":"/news/topic.tax/"},{"tagId":"newsroom:topics/opinion","name":"opinion","description":"Expert opinions and insights. ","title":"Opinion","url":"/news/topic.opinion/"},{"tagId":"newsroom:topics/goodpair","name":"goodpair","description":"Explore more Good Pair stories, showing two people making a big difference together. ","title":"Good Pair","url":"/news/topic.goodpair/"},{"tagId":"newsroom:topics/deals","name":"deals","description":"Explore more Deals insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Deals","url":"/news/topic.deals/"},{"tagId":"newsroom:topics/analysis","name":"analysis","description":"Expert analysis on economic news and other trends.","title":"Analysis","url":"/news/topic.analysis/"},{"tagId":"newsroom:topics/veterans","name":"veterans","description":"Explore more insights about defence force veterans at Westpac Wire.","title":"Veterans","url":"/news/topic.veterans/"},{"tagId":"newsroom:topics/IWD","name":"IWD","description":"Stories focusing on International Women\u0027s Day, on 8 March annually. ","title":"IWD ","url":"/news/topic.IWD/"},{"tagId":"newsroom:topics/currencies","name":"currencies","description":"Stories providing currencies insights, tips and trends.","title":"Currencies","url":"/news/topic.currencies/"},{"tagId":"newsroom:topics/rework","name":"rework","description":"Stories of businesses pivoting in the face of the COVID-19 pandemic.","title":"Rework","url":"/news/topic.rework/"},{"tagId":"newsroom:topics/luciscall","name":"luciscall","description":"Explore more insights from Westpac\u0027s chief economist Luci Ellis at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Luci\u0027s Call","url":"/news/topic.luciscall/"},{"tagId":"newsroom:topics/10Qs","name":"10Qs","description":"\"10Qs with...\" is a series that asks leaders what makes them tick.","title":"10Qs","url":"/news/topic.10Qs/"},{"tagId":"newsroom:topics/quarterlife","name":"quarterlife","description":"Explore more Quarter Life insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Quarter Life","url":"/news/topic.quarterlife/"},{"tagId":"newsroom:topics/commodities","name":"commodities","description":"Insights into commodities markets.","title":"Commodities","url":"/news/topic.commodities/"},{"tagId":"newsroom:topics/shareholders","name":"shareholders","description":"Stories relevant to Westpac shareholders.","title":"Shareholders","url":"/news/topic.shareholders/"},{"tagId":"newsroom:topics/climate","name":"climate","description":"Explore more climate insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Climate ","url":"/news/topic.climate/"},{"tagId":"newsroom:topics/esg","name":"esg","description":"Explore more insights on environmental, social and governance issues at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"ESG","url":"/news/topic.esg/"},{"tagId":"newsroom:topics/boardwalk","name":"boardwalk","description":"A series of in-depth podcast interviews with board directors to find out what\u0027s on their minds. ","title":"Board Walk","url":"/news/topic.boardwalk/"}]}