Budget spend just a minor blip on RBA’s rate radar

Treasurer Jim Chalmers delivers the federal budget to parliament, May 2023. (Getty)

The government has delivered an expansionary budget by historical standards, but a sharp economic slowdown in the second half of the year means it’s unlikely to have much bearing on the outlook for interest rates.

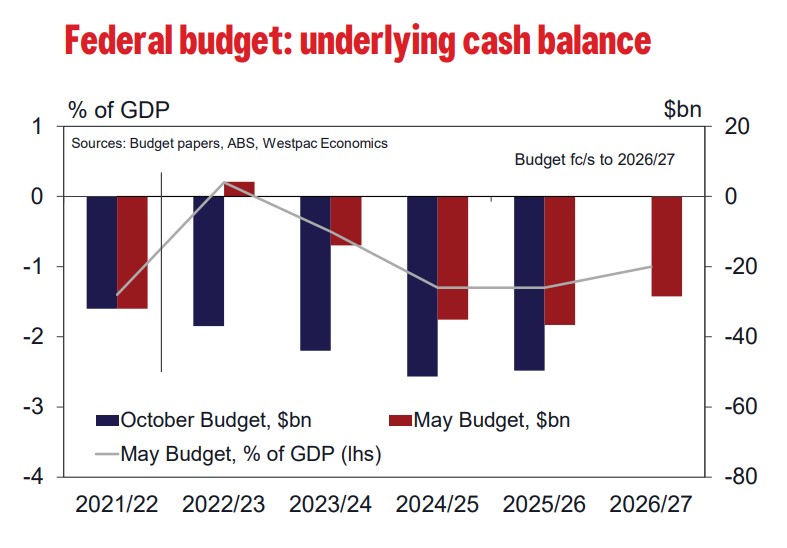

The starting point for the 2023 Budget is an improvement in the underlying cash position of $146 billion over the five years to 2026/27 compared to the October 2022 Budget.

Cumulative deficits over the period have been reduced to $126 billion, which means that the government has “saved” 86 per cent of the improvement over the five years.

The government might like you to think that the upgraded fiscal outlook is a direct result of its astute economic management. In reality, it’s just as much down to the Treasury, and the market, underestimating Australia’s prospects in October last year.

For example, the October Budget forecast that the iron ore price would fall from around $100 per ton to $55 between October 2022 and March 2023. That was too pessimistic, particularly given the commitment from producers to control output.

Even more important was an underestimate of the strength of the labour market, with a sustained 3.5 per cent jobless rate being considered unlikely.

In contrast, Westpac assesses that in the May budget the government is underestimating the likely weakness of the real economy in the key 2023/24 fiscal year. We expect that consumption growth will slow to only 0.7 per cent, with GDP growth at a sluggish 0.9 per cent. That compares with the government’s forecast of 1.5 per cent growth in consumption and GDP.

These assumptions are important for the interest rate debate.

By our measure this is an expansionary budget when compared with the ten budgets preceding the Covid period. Over that period net spending in the fiscal year immediately following the budget ranged up to 0.25 per cent of GDP, and up to 0.5 per cent of GDP over the three-year forecast period. In the 2023 budget, net new spending for 2023/24 equates to about 0.5 per cent of GDP, and 0.75 per cent over the period to 2025/26.

The Reserve Bank will be aware of these comparisons, but its unlikely to factor into their deliberations at the August Board meeting - the first meeting when we expect any decision to further raise rates to be a live possibility.

The key issues at that meeting will continue to be the unemployment rate; the extent to which underlying inflation has fallen during the June quarter; global developments, and the overall state of the economy.

As we saw in May, the Board considered that inflation was too high and the labour market still very tight, leading them to conclude that another hike was needed. Those factors could still be sufficient to see another increase in August, although we expect that evidence of the economic slowdown will be much clearer in August and, globally, central banks will be on hold.

The RBA will also be aware that the rollover of fixed rate housing loans into much higher floating rates will accelerate over the balance of the year. In its recent Statement on Monetary Policy the central bank calculated that since April 2022 average mortgage rates had increased by 225 basis points, compared to the increase in the cash rate of 375 basis points, despite banks consistently passing on the full cash rate increase to existing borrowers.

This reflects lags in the banks passing on their increases; strong competition for new loans; and the volume of fixed rates in the system which are unaffected by RBA policy.

However, it also means there is still significant monetary tightening to come in the economy, even if May’s hike does prove to be the RBA’s last.

We expect the average mortgage rate can still increase by up to 75 basis points as fixed rates convert into higher floating rates. That process, whereby average rates are rising even with the RBA on hold, should be an important consideration for the Board through the second half of 2023.

All things considered, we think the RBA will stay on hold in August. The spending boost from the budget will work through the economy in 2023/24 and the Board is likely to wait to assess the impact of that as the financial year unfolds.

Our assessment of the impact on the economy from the ongoing increases in average mortgage rates; the sharp economic slowdown that is already underway; and prospects for further falls in inflation are consistent with the RBA beginning its easing cycle from February next year.

That timing also aligns with expected cuts in the federal funds rate from the FOMC, which we expect to begin in late December this year.

If the expansionary budget is to have any major implications for monetary policy it will be in the timing of the start of the easing cycle. At worst those cuts might be delayed, but given our views on the broader economic slowdown, the stimulus in the budget is likely to be a secondary factor for the interest rate outlook.