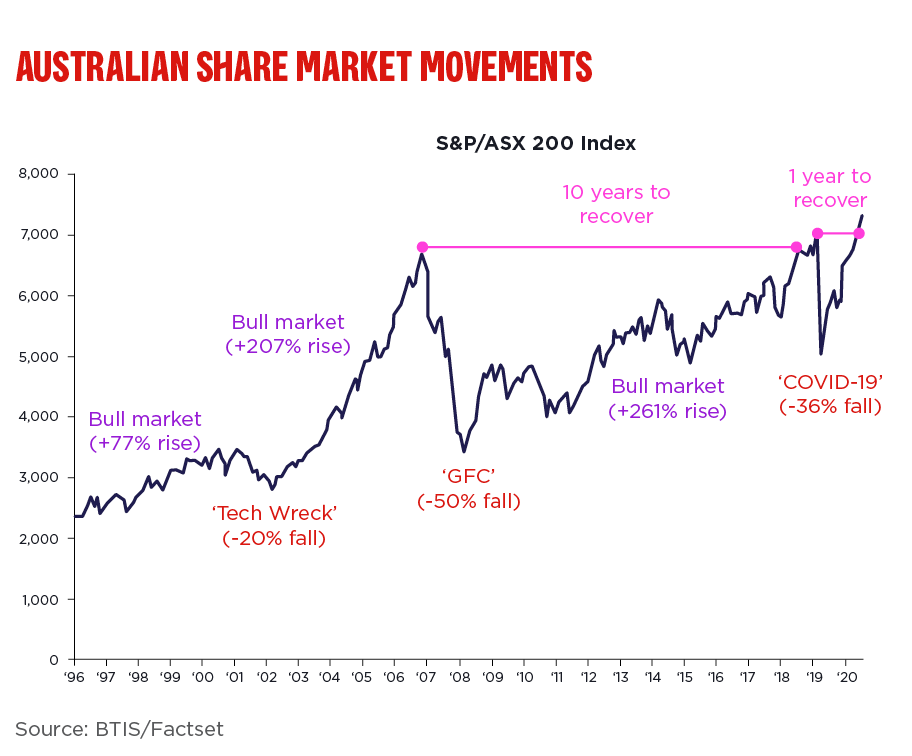

The impact of COVID-19 was sudden and unexpected, taking markets by surprise.

As many investors will no doubt recall, many asset classes quickly dived amid extreme volatility in March 2020, the Aussie stock market crashing almost 40 per cent over that month alone.

But super fund members who held their nerve and did not panic have been rewarded with a year of outstanding returns.

According to Chant West, the median growth fund was up 18 per cent for the year to June 2021, with many funds delivering returns in excess of 20 per cent.

How did this happen following the quickest and sharpest recession since the 1930s?

A quick recap of FY21

It’s worth remembering that markets are forward looking. And by July 2020, the world was looking a lot better than it did a few months earlier. Individuals, communities, businesses and governments had come together, adapting to new social norms to keep each other safe and economies going.

Soon enough, this quickly turned into full blown economic recovery as lockdowns and restrictions eased, record government spending circulated through economies and vaccines emerged.

In the US, despite its lowest ever gross domestic product number at the start of 2020, the S&P 500 posted one of its strongest monthly returns since 1986 in August 2020 and Joe Biden’s Presidential election win in November proved a further positive turning point.

In Asia, a resurgence in cases in India towards the end of the financial year, along with soaring inflation due to heavy rainfall and increased energy costs, weighed on the recovery. But in China, all the share market losses since the start of the pandemic had already been erased back in October, with growth remaining strong.

Meanwhile in Europe, after Brexit terms were agreed in December 2020 the focus shifted to vaccine rollouts and economic recovery, while in the UK, a gradual exit from lockdown in April lifted consumer confidence as the country hurtled towards this month’s “Freedom Day”.

Finally, in Australia, after a rocky start to FY21, plenty of support from government stimulus (think JobKeeper) and the Reserve Bank’s record low cash rate of just 0.10 per cent – not to mention it joining the “quantitative easing” party (bond buying) – helped the economic recovery surprise basically all forecasters at every turn.

How did financial markets respond?

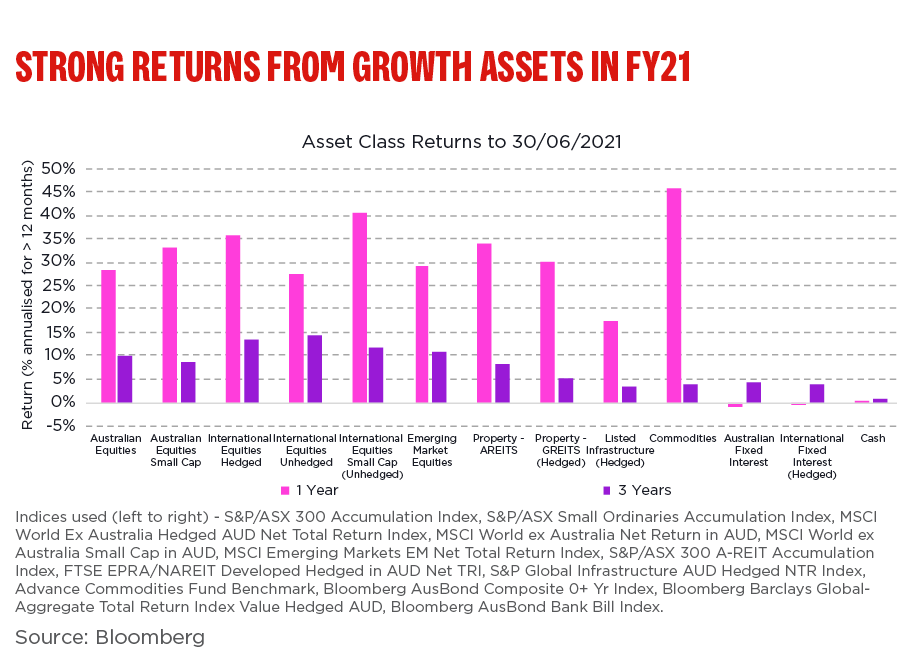

In turn, most major markets rallied hard, with several stock markets hitting record levels.

In particular, the Australian and US markets both experienced an extraordinary rebound following the economic policy support by provided by domestic and international governments.

While cash rates globally have been very low, or below zero since the start of the pandemic, cash and fixed interest unsurprisingly underperformed. But they still play an important defensive role in a diversified investment portfolio – providing some cushioning against large market falls, such as those experienced in March 2020.

BT’s super returns

Our younger “Lifestage” members were the big winners. Those born in the 1970s to 2000s have around 85 per cent invested in growth assets in their funds and as such have benefited from the strength in share markets with returns of between 25.1 per cent and 25.6 per cent , outperforming industry median returns.

With smaller allocations to growth assets, and a higher proportion of defensive assets (cash, fixed interest), our 1940s, 1950s and 1960s Lifestage members experienced more moderate returns. This is expected given our Lifestage funds are designed to gradually reduce members’ exposures to riskier assets, such as shares, as members approach retirement. However, returns for these members (between 8.4 per cent and 16.9 per cent) were also above industry median returns.

Looking Ahead

Whist we still have governments and central banks rolling out stimulus to aid the recovery, we are conscious of the current impacts of second and third waves of the virus, now in many mutating forms such as the Delta strain taking hold across Australia, the UK, the US and other markets.

Understandably, this is starting to unnerve markets.

However, it’s likely we’ll see more stability in markets in FY22 compared to the previous 12 months as many major economies gain momentum.

In Australia, despite the current lockdowns, record low interest rates – which are not expected to rise until 2023 (at the earliest) – unemployment below pre-COVID levels and support from governments and the banks, means we are well placed to get through this recent challenging outbreak.

Globally, trade and territorial challenges with China along with ongoing tensions in the Middle East – in addition to the Biden administration exerting its influence across the globe – need to be monitored. And it was only a little over a year ago that the European Union was dealing with the reality of Brexit, with the impacts remaining unclear.

But stepping back, over the long-term both listed markets and unlisted assets, such as property and infrastructure, continue to provide good opportunities to build long-term wealth.

As always, maintaining good diversification in super when investing is key because it reduces the exposure to single economic or market “black swans” or events.

And by avoiding panic and staying invested for the long term, investors can make the most of rebounding markets – as FY21 showed in spades.

This information of general nature only. It does not take into account your personal objectives, financial situation or needs and so you should consider its appropriateness, having regard to these factors and your personal circumstances before acting on it. Information from third parties is believed to be reliable however it has not been independently verified. While the information in this communication is provided in good faith, no warranty is given that it is accurate, reliable or free from error or omission. Past performance is not a reliable indicator of future performance. BT Funds Management Limited ABN 63 002 916 458 is the trustee of and issuer of interests in BT Super, which forms part of the Retirement Wrap ABN 39 827 542 991. A product disclosure statement (PDS) is available for each of these products by calling 132 135 or visiting bt.com.au.. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of interests in BT Super. An investment in BT Super is not an investment in, deposit with or any other liability of Westpac Banking Corporate ABN 33 007 457 141 (Westpac) or any other company in the Westpac Group. It is subject to investment risk, including possible delays in repayment or loss of income and principal invested. Westpac and its related entities do not stand behind or otherwise guarantee the capital value or investment performance of the BT Super product.

Corrin Collocott was appointed BT's Chief Investment Officer in 2017, after joining BT Investment Solutions in 2015. He has responsibility for the BT Investment Solutions Investment Team and the investment management of all BTIS investment products and strategies spanning Investment, Super, SMA, Model Portfolios and bespoke strategies. His previous roles included Manager Investment Strategies at Sunsuper, roles across a variety of industries including Russell Investment Group, lnTech, MCA NZ Limited and Watson Wyatt Worldwide.

{"topicSelector":[{"tagId":"newsroom:topics/economy","name":"economy","description":"Explore more Economy insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Economy","url":"/news/topic.economy/"},{"tagId":"newsroom:topics/westpac","name":"westpac","description":"Stories featuring Westpac corporate news.","title":"Westpac","url":"/news/topic.westpac/"},{"tagId":"newsroom:topics/community","name":"community","description":"Explore more community insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Community","url":"/news/topic.community/"},{"tagId":"newsroom:topics/banking","name":"banking","description":"Explore more Banking insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Banking","url":"/news/topic.banking/"},{"tagId":"newsroom:topics/covid19","name":"covid19","description":"Stories influenced by the COVID-19 pandemic.","title":"COVID-19","url":"/news/topic.covid19/"},{"tagId":"newsroom:topics/sme","name":"sme","description":"Explore more Small Medium Enterprise insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"SME","url":"/news/topic.sme/"},{"tagId":"newsroom:topics/diversity","name":"diversity","description":"Explore more Diversity insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Diversity","url":"/news/topic.diversity/"},{"tagId":"newsroom:topics/property","name":"property","description":"Explore more Property insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Property","url":"/news/topic.property/"},{"tagId":"newsroom:topics/technology","name":"technology","description":"Explore more Technology insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Technology","url":"/news/topic.technology/"},{"tagId":"newsroom:topics/workplace","name":"workplace","description":"Explore more workplace insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Workplace","url":"/news/topic.workplace/"},{"tagId":"newsroom:topics/sustainability","name":"sustainability","description":"Explore more sustainability insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Sustainability","url":"/news/topic.sustainability/"},{"tagId":"newsroom:topics/scams","name":"scams","description":"Stories about the latest cyber scams news and trends. ","title":"Scams","url":"/news/topic.scams/"},{"tagId":"newsroom:topics/personalfinance","name":"personalfinance","description":"Explore more insights about personal finance, financial literacy and financial wellbeing. ","title":"Personal finance","url":"/news/topic.personalfinance/"},{"tagId":"newsroom:topics/career","name":"career","description":"Stories providing career insights, tips and trends.","title":"Career","url":"/news/topic.career/"},{"tagId":"newsroom:topics/billsbites","name":"billsbites","description":"Explore more insights from Bill Evans at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Bill\u0027s Bites","url":"/news/topic.billsbites/"},{"tagId":"newsroom:topics/social-enterprise","name":"social-enterprise","description":"Stories relevant to or featuring social enterprises.","title":"Social enterprise","url":"/news/topic.social-enterprise/"},{"tagId":"newsroom:topics/investing","name":"investing","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Investing","url":"/news/topic.investing/"},{"tagId":"newsroom:topics/leadership","name":"leadership","description":"Explore more Leadership insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Leadership","url":"/news/topic.leadership/"},{"tagId":"newsroom:topics/environment","name":"environment","description":"Explore more Environment insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Environment","url":"/news/topic.environment/"},{"tagId":"newsroom:topics/agribusiness","name":"agribusiness","description":"Explore more Agribusiness insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Agribusiness","url":"/news/topic.agribusiness/"},{"tagId":"newsroom:topics/wellbeing","name":"wellbeing","description":"Stories featuring wellbeing trends, insights and stories.","title":"Wellbeing","url":"/news/topic.wellbeing/"},{"tagId":"newsroom:topics/politics","name":"politics","description":"Explore more Politics insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Politics","url":"/news/topic.politics/"},{"tagId":"newsroom:topics/innovators","name":"innovators","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Innovators","url":"/news/topic.innovators/"},{"tagId":"newsroom:topics/fintech","name":"fintech","description":"Explore more Fintech insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Fintech","url":"/news/topic.fintech/"},{"tagId":"newsroom:topics/data","name":"data","description":"Explore more data insights at Westpac Wire.","title":"Data","url":"/news/topic.data/"},{"tagId":"newsroom:topics/indigenous","name":"indigenous","description":"Explore more indigenous insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Indigenous","url":"/news/topic.indigenous/"},{"tagId":"newsroom:topics/payments","name":"payments","description":"Explore more Payments insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Payments","url":"/news/topic.payments/"},{"tagId":"newsroom:topics/history","name":"history","description":"Stories unearthed from Westpac\u0027s private archival collection. ","title":"History","url":"/news/topic.history/"},{"tagId":"newsroom:topics/podcast","name":"podcast","description":"Explore Westpac Wire\u0027s podcast series.","title":"Podcast","url":"/news/topic.podcast/"},{"tagId":"newsroom:topics/luciscall","name":"luciscall","description":"Explore more insights from Westpac\u0027s chief economist Luci Ellis at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Luci\u0027s Call","url":"/news/topic.luciscall/"},{"tagId":"newsroom:topics/startups","name":"startups","description":"Explore more Startups insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Startups","url":"/news/topic.startups/"},{"tagId":"newsroom:topics/currencies","name":"currencies","description":"Stories providing currencies insights, tips and trends.","title":"Currencies","url":"/news/topic.currencies/"},{"tagId":"newsroom:topics/opinion","name":"opinion","description":"Expert opinions and insights. ","title":"Opinion","url":"/news/topic.opinion/"},{"tagId":"newsroom:topics/asia","name":"asia","description":"Explore more Asia insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Asia","url":"/news/topic.asia/"},{"tagId":"newsroom:topics/analysis","name":"analysis","description":"Expert analysis on economic news and other trends.","title":"Analysis","url":"/news/topic.analysis/"},{"tagId":"newsroom:topics/superannuation","name":"superannuation","description":"Explore more Superannuation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Superannuation","url":"/news/topic.superannuation/"},{"tagId":"newsroom:topics/IWD","name":"IWD","description":"Stories focusing on International Women\u0027s Day, on 8 March annually. ","title":"IWD ","url":"/news/topic.IWD/"},{"tagId":"newsroom:topics/rework","name":"rework","description":"Stories of businesses pivoting in the face of the COVID-19 pandemic.","title":"Rework","url":"/news/topic.rework/"},{"tagId":"newsroom:topics/veterans","name":"veterans","description":"Explore more insights about defence force veterans at Westpac Wire.","title":"Veterans","url":"/news/topic.veterans/"},{"tagId":"newsroom:topics/commodities","name":"commodities","description":"Insights into commodities markets.","title":"Commodities","url":"/news/topic.commodities/"},{"tagId":"newsroom:topics/10Qs","name":"10Qs","description":"\"10Qs with...\" is a series that asks leaders what makes them tick.","title":"10Qs","url":"/news/topic.10Qs/"},{"tagId":"newsroom:topics/deals","name":"deals","description":"Explore more Deals insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Deals","url":"/news/topic.deals/"},{"tagId":"newsroom:topics/tax","name":"tax","description":"Explore more tax insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Tax","url":"/news/topic.tax/"},{"tagId":"newsroom:topics/regional","name":"regional","description":"Explore more Regional insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regional","url":"/news/topic.regional/"},{"tagId":"newsroom:topics/regulation","name":"regulation","description":"Explore more Regulation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regulation","url":"/news/topic.regulation/"},{"tagId":"newsroom:topics/reinventure","name":"reinventure","description":"Explore more Reinventure insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Reinventure","url":"/news/topic.reinventure/"},{"tagId":"newsroom:topics/businesses-of-tomorrow","name":"businesses-of-tomorrow","description":"Stories featuring Westpac Businesses of Tomorrow program winners. ","title":"Westpac Businesses of Tomorrow","url":"/news/topic.businesses-of-tomorrow/"},{"tagId":"newsroom:topics/shareholders","name":"shareholders","description":"Stories relevant to Westpac shareholders.","title":"Shareholders","url":"/news/topic.shareholders/"},{"tagId":"newsroom:topics/climate","name":"climate","description":"Explore more climate insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Climate ","url":"/news/topic.climate/"},{"tagId":"newsroom:topics/esg","name":"esg","description":"Explore more insights on environmental, social and governance issues at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"ESG","url":"/news/topic.esg/"},{"tagId":"newsroom:topics/boardwalk","name":"boardwalk","description":"A series of in-depth podcast interviews with board directors to find out what\u0027s on their minds. ","title":"Board Walk","url":"/news/topic.boardwalk/"}]}