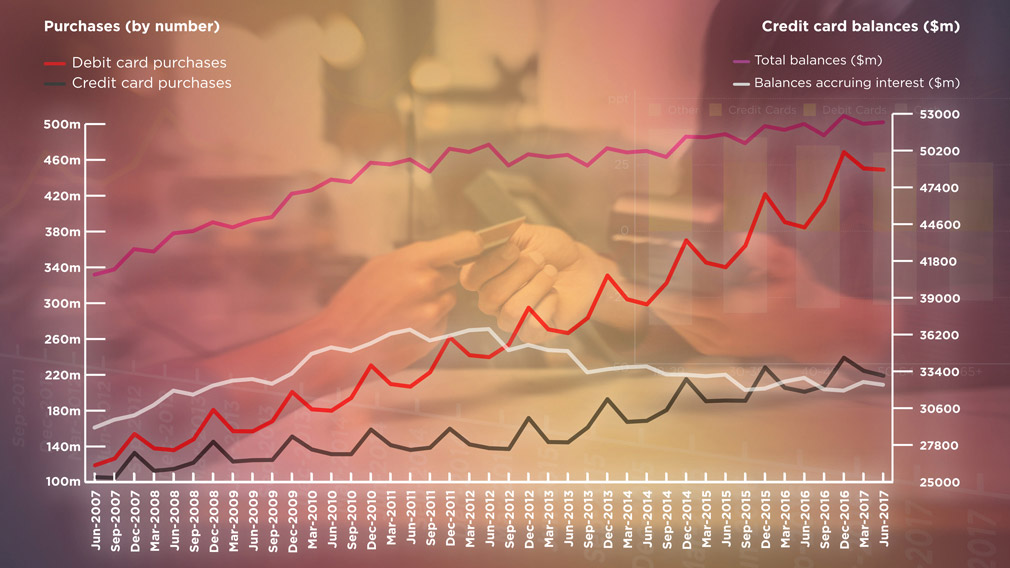

Debit cards are used for more than twice as many purchases as credit cards today, compared to roughly the same number 10 years ago, but Australians' total credit card balances continue to rise. (Source: Reserve Bank of Australia data, compiled by Westpac)

Around a decade ago, Australians began to change the way they paid with plastic, as debit cards started to overtake credit cards as the go-to payment method.

While perhaps an unstartling development to some, the data is anything but. Today, around twice as many purchases by number – around 449 million – are made using debit cards as with credit cards (about 219 million), according to Reserve Bank of Australia data, compared to ten years ago when the figures were roughly the same.

The shift has occurred amid a massive structural move towards digital payments that last year resulted in credit and debit cards, combined, overtaking cash as the most frequently used means of payment for the first time, according to the RBA. While the jury is out on their long-term widespread adoption, “cryptocurrencies” such as bitcoin have even become a payment method for some.

Yet despite the relative decline in how often credit cards are used, the outstanding debt on them has continued to slowly expand in the last decade to more than $52 billion. The size of the debt, particularly the $32bn accruing interest, has sparked heightened community and political interest in the market, comprised of at least 80 card providers and more than 250 products.

Banks have responded with a flurry of new credit card features, such as repayment instalment plans, while “fintech” operators have emerged with new ways to buy and pay back later, such as digital wallet provider Zip Money – in which Westpac recently made a $40m investment – and Afterpay.

All these factors have prompted the question of what’s driving the swing towards debit and whether some people even need a credit card?

According to Westpac’s head of cards Stephen Wooldridge, a blend of factors has prompted the shift, including generational change and technological progress enabling debit cards to be used to buy goods online and make contactless payments.

“Millennials are not as fond of credit as their grandparents may have been. A lot of them have grown up during the ‘credit crunch’ and are more wary of credit related products,” he says.

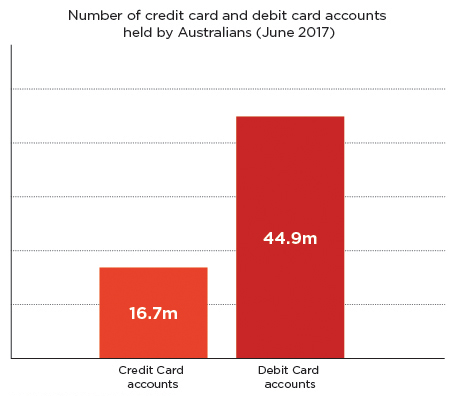

Indeed, the RBA’s recent triennial Consumer Payments Survey showed around 70 per cent of survey participants aged under 30 did not own a credit card last year, almost double the percentage of older Australians.

“The rate at which people are carrying forward a balance and therefore paying interest has been declining year on year for the last ten years, reflecting a move towards other types of financing, and a rise in debit, especially with ‘tap and pay’ becoming so widespread,” says Wooldridge.

“Connecting to a merchant isn’t as difficult as it used to be. Everyone is online. The number of options a customer has to settle a bill at a store is probably 10 times that of what it was.”

Just a decade ago, a credit card was just about the only way you could pay online. These days, most debit cards can be used in the online domain where credit cards used to be king.

Source: Reserve Bank of Australia data, compiled by Westpac.

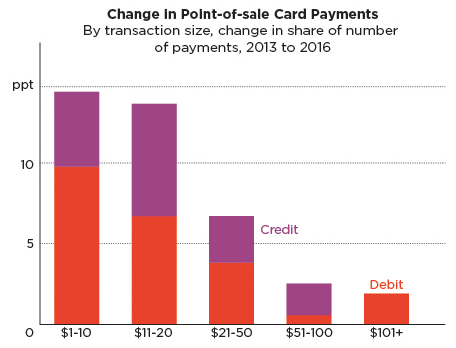

The RBA survey found 85 per cent of participants had a contactless card last year, compared with two-thirds of respondents in 2013. In terms of dollars spent, the RBA says around $21.9bn went through debit cards in June 2017, and $26.7bn on credit, continuing to narrow a gap from a decade ago when credit cards paid for more than twice as much.

“The recent growth in the relative use of cards was strongest for lower-value transactions, with consumers increasingly using debit (and to a lesser extent credit) cards for payments of $20 or less,” the RBA’s triennial Consumer Payments Survey says.

Source: RBA calculations, based on data from Colmar Brunton and Ipsos, compiled by Westpac.

The RBA says another contributor to the strong growth in debit card payments has been the “broader macroeconomic environment” as households became “less inclined to finance consumption using debt” since the global financial crisis. Reforms to “interchange fees” – payments between a merchant and cardholder’s bank – since the early 2000s may have also reduced the appeal of higher-cost credit cards, such as those offering “reward” programs.

Credit cards have provided regulatory, legal and reputational issues for banks around the world over the years, including in Australia. The profitability from credit cards has also remained relatively flat since 2010 despite lower funding costs as banks decreased some interest rates and changed their products, according to Westpac’s submission to a Senate inquiry into credit cards. But despite this, banks continue to invest in credit cards and believe they still serve a purpose for many people, namely convenient – and sometimes necessary – cash flow.

According to research from BT Financial Group, nearly a third of Australians say they always, or often, live pay cheque to pay cheque, and more than one in seven say they wouldn’t be able to handle a financial emergency over $500. Numerous surveys have found Americans to be similarly exposed to surprise calls for cash on short notice.

Credit cards are used by many to “smooth” irregularities in income and increase financial stability.

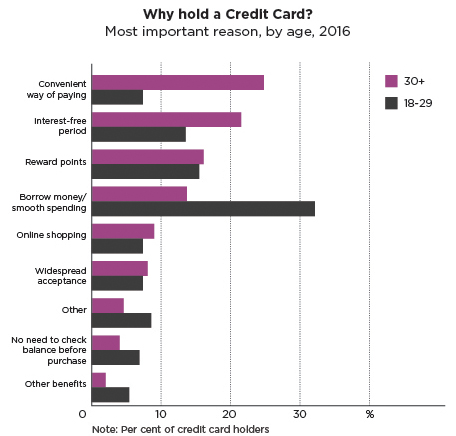

The RBA study found that age is a key factor: “A relatively small proportion of consumers aged under 30 cited the convenience of making payments as the most important reason for holding a credit card. Instead, they tended to perceive debit cards as more convenient for making payments and managing finances, but were more likely than older respondents to value the ability to use a credit card to borrow money or smooth spending.”

Source: Reserve Bank of Australia, compiled by Westpac.

Banks are acting to alleviate the pressure on customers that use credit cards for short term finance. Wooldridge says people may be “surprised at how many steps there are to safeguard customers” from the moment they apply, including investing in digital tools to make cards more secure and easy to use, such as payment plans and alerts to reduce debt.

Westpac recently launched Westpac Lite, a new low-rate credit card at 9.9 per cent, the sole card offered by the big four lenders with a rate below 10 per cent, for people who want a card for short term borrowing. At the same time, the bank introduced a payment instalment feature, SmartPlan, enabling customers to pay down their overall credit card balance or individual purchases through a series of instalments.

These investments form part of what it costs banks to provide credit cards, along with remediating for fraud, fraud protection, rewards and product benefits. Credit card are also “unsecured lending”, meaning banks have to factor in the cost of losses given there are no assets sitting behind the loan, which banks have argued is why interest rates are higher than mortgages, for example.

The RBA told the 2015 Senate inquiry into cards that the major banks’ interest rate on their entire credit card portfolios had fallen about 2 per cent since mid- 2011 to around 11.6 per cent.

Following the inquiry, the federal government in this year’s budget released the “first phase” of reforms that aim to “ensure that consumers can manage their credit card debts and help prevent the debt cycle that many Australians find themselves in”. The package includes stricter affordability assessments, simplifying how interest is calculated and requiring online options to cancel cards and reduce credit limits. In September, the corporate regulator ASIC confirmed it was engaging in a review of the consumer credit card industry to better understand the design and distribution of cards and how this might impact debt levels, including some focus on “balance transfers”.

ASIC’s MoneySmart website says that while credit cards are “convenient”, this did not mean they are free and consumers should try and avoid fees and interest by paying their cards on time, maximising credit card repayments, setting sensible credit limit and building up separate funds for emergencies over time.

Wooldridge says Westpac agrees with MoneySmart’s tips, and that banks are taking steps to educate customers on how to best use their cards and introduce innovations to give customers even greater control over their finances, which “can only be a good thing”.

He says this includes proactively encouraging customers with long standing credit card balances to consider transferring their debt to a structured personal loan with a lower interest rate, and “prompting” customers to optimise their borrowing by using other lower-cost options or tools like Smartplan.

Tips on how to stay in control of credit cards.

Ultimately, he says technology developments will see the concept of debit and credit cards, becoming more about the timing of when funds are transferred.

“Right now, I have my debit card and my credit card in my wallet – the historical way of me connecting with my accounts. When plastic disappears and we all have digital wallets, all it becomes is two se parate forms of paying – either up front with cash or after the fact with credit,” he says.

In the meantime, Australians’ appetite for debt may be unlikely to rise any time soon following a fall in the household savings rate from 10 per cent in late 2011 to below 5 per cent this year, according to Morgan Stanley analyst Chris Nicol. In an August report, he wrote that consumers were facing more intense cost of living pressures such as higher energy prices and feeling left behind any recovery in business conditions.

“All up, we think it will be difficult for consumers to continue to live at or beyond their means,” he wrote. Additional reporting: Michael Bennet

Westpac Banking Corporation ABN 33 007 457 141 AFSL and Australian credit licence 233714.

Emma Foster is a freelance writer. Previously, she led Westpac Wire and was a key contributor until December 2022. Prior to joining Westpac in 2013, she spent almost 20 years in corporate affairs and investor relations, primarily in large financial services and consultancy firms, in Australia, UK and Europe. She is also a photographer and podcaster.

{"topicSelector":[{"tagId":"newsroom:topics/economy","name":"economy","description":"Explore more Economy insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Economy","url":"/news/topic.economy/"},{"tagId":"newsroom:topics/banking","name":"banking","description":"Explore more Banking insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Banking","url":"/news/topic.banking/"},{"tagId":"newsroom:topics/digital","name":"digital","description":"Explore more Digital insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Digital","url":"/news/topic.digital/"},{"tagId":"newsroom:topics/diversity","name":"diversity","description":"Explore more Diversity insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Diversity","url":"/news/topic.diversity/"},{"tagId":"newsroom:topics/community","name":"community","description":"Explore more community insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Community","url":"/news/topic.community/"},{"tagId":"newsroom:topics/workplace","name":"workplace","description":"Explore more workplace insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Workplace","url":"/news/topic.workplace/"},{"tagId":"newsroom:topics/sustainability","name":"sustainability","description":"Explore more sustainability insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Sustainability","url":"/news/topic.sustainability/"},{"tagId":"newsroom:topics/technology","name":"technology","description":"Explore more Technology insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Technology","url":"/news/topic.technology/"},{"tagId":"newsroom:topics/property","name":"property","description":"Explore more Property insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Property","url":"/news/topic.property/"},{"tagId":"newsroom:topics/westpac","name":"westpac","description":"Stories featuring Westpac corporate news.","title":"Westpac","url":"/news/topic.westpac/"},{"tagId":"newsroom:topics/sme","name":"sme","description":"Explore more Small Medium Enterprise insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"SME","url":"/news/topic.sme/"},{"tagId":"newsroom:topics/innovators","name":"innovators","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Innovators","url":"/news/topic.innovators/"},{"tagId":"newsroom:topics/leadership","name":"leadership","description":"Explore more Leadership insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Leadership","url":"/news/topic.leadership/"},{"tagId":"newsroom:topics/covid19","name":"covid19","description":"Stories influenced by the COVID-19 pandemic.","title":"COVID-19","url":"/news/topic.covid19/"},{"tagId":"newsroom:topics/investing","name":"investing","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Investing","url":"/news/topic.investing/"},{"tagId":"newsroom:topics/startups","name":"startups","description":"Explore more Startups insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Startups","url":"/news/topic.startups/"},{"tagId":"newsroom:topics/personalfinance","name":"personalfinance","description":"Explore more insights about personal finance, financial literacy and financial wellbeing. ","title":"Personal finance","url":"/news/topic.personalfinance/"},{"tagId":"newsroom:topics/agribusiness","name":"agribusiness","description":"Explore more Agribusiness insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Agribusiness","url":"/news/topic.agribusiness/"},{"tagId":"newsroom:topics/scams","name":"scams","description":"Stories about the latest cyber scams news and trends. ","title":"Scams","url":"/news/topic.scams/"},{"tagId":"newsroom:topics/billsbites","name":"billsbites","description":"Explore more insights from Bill Evans at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Bill\u0027s Bites","url":"/news/topic.billsbites/"},{"tagId":"newsroom:topics/data","name":"data","description":"Explore more data insights at Westpac Wire.","title":"Data","url":"/news/topic.data/"},{"tagId":"newsroom:topics/environment","name":"environment","description":"Explore more Environment insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Environment","url":"/news/topic.environment/"},{"tagId":"newsroom:topics/payments","name":"payments","description":"Explore more Payments insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Payments","url":"/news/topic.payments/"},{"tagId":"newsroom:topics/fintech","name":"fintech","description":"Explore more Fintech insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Fintech","url":"/news/topic.fintech/"},{"tagId":"newsroom:topics/politics","name":"politics","description":"Explore more Politics insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Politics","url":"/news/topic.politics/"},{"tagId":"newsroom:topics/career","name":"career","description":"Stories providing career insights, tips and trends.","title":"Career","url":"/news/topic.career/"},{"tagId":"newsroom:topics/social-enterprise","name":"social-enterprise","description":"Stories relevant to or featuring social enterprises.","title":"Social enterprise","url":"/news/topic.social-enterprise/"},{"tagId":"newsroom:topics/indigenous","name":"indigenous","description":"Explore more indigenous insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Indigenous","url":"/news/topic.indigenous/"},{"tagId":"newsroom:topics/regulation","name":"regulation","description":"Explore more Regulation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regulation","url":"/news/topic.regulation/"},{"tagId":"newsroom:topics/wellbeing","name":"wellbeing","description":"Stories featuring wellbeing trends, insights and stories.","title":"Wellbeing","url":"/news/topic.wellbeing/"},{"tagId":"newsroom:topics/superannuation","name":"superannuation","description":"Explore more Superannuation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Superannuation","url":"/news/topic.superannuation/"},{"tagId":"newsroom:topics/westpac-scholars","name":"westpac-scholars","description":"Stories featuring Westpac Scholars. ","title":"Westpac Scholars","url":"/news/topic.westpac-scholars/"},{"tagId":"newsroom:topics/asia","name":"asia","description":"Explore more Asia insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Asia","url":"/news/topic.asia/"},{"tagId":"newsroom:topics/podcast","name":"podcast","description":"Explore Westpac Wire\u0027s podcast series.","title":"Podcast","url":"/news/topic.podcast/"},{"tagId":"newsroom:topics/history","name":"history","description":"Stories unearthed from Westpac\u0027s private archival collection. ","title":"History","url":"/news/topic.history/"},{"tagId":"newsroom:topics/businesses-of-tomorrow","name":"businesses-of-tomorrow","description":"Stories featuring Westpac Businesses of Tomorrow program winners. ","title":"Westpac Businesses of Tomorrow","url":"/news/topic.businesses-of-tomorrow/"},{"tagId":"newsroom:topics/tax","name":"tax","description":"Explore more tax insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Tax","url":"/news/topic.tax/"},{"tagId":"newsroom:topics/luciscall","name":"luciscall","description":"Explore more insights from Westpac\u0027s chief economist Luci Ellis at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Luci\u0027s Call","url":"/news/topic.luciscall/"},{"tagId":"newsroom:topics/goodpair","name":"goodpair","description":"Explore more Good Pair stories, showing two people making a big difference together. ","title":"Good Pair","url":"/news/topic.goodpair/"},{"tagId":"newsroom:topics/opinion","name":"opinion","description":"Expert opinions and insights. ","title":"Opinion","url":"/news/topic.opinion/"},{"tagId":"newsroom:topics/currencies","name":"currencies","description":"Stories providing currencies insights, tips and trends.","title":"Currencies","url":"/news/topic.currencies/"},{"tagId":"newsroom:topics/deals","name":"deals","description":"Explore more Deals insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Deals","url":"/news/topic.deals/"},{"tagId":"newsroom:topics/veterans","name":"veterans","description":"Explore more insights about defence force veterans at Westpac Wire.","title":"Veterans","url":"/news/topic.veterans/"},{"tagId":"newsroom:topics/analysis","name":"analysis","description":"Expert analysis on economic news and other trends.","title":"Analysis","url":"/news/topic.analysis/"},{"tagId":"newsroom:topics/IWD","name":"IWD","description":"Stories focusing on International Women\u0027s Day, on 8 March annually. ","title":"IWD ","url":"/news/topic.IWD/"},{"tagId":"newsroom:topics/rework","name":"rework","description":"Stories of businesses pivoting in the face of the COVID-19 pandemic.","title":"Rework","url":"/news/topic.rework/"},{"tagId":"newsroom:topics/10Qs","name":"10Qs","description":"\"10Qs with...\" is a series that asks leaders what makes them tick.","title":"10Qs","url":"/news/topic.10Qs/"},{"tagId":"newsroom:topics/commodities","name":"commodities","description":"Insights into commodities markets.","title":"Commodities","url":"/news/topic.commodities/"},{"tagId":"newsroom:topics/quarterlife","name":"quarterlife","description":"Explore more Quarter Life insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Quarter Life","url":"/news/topic.quarterlife/"},{"tagId":"newsroom:topics/shareholders","name":"shareholders","description":"Stories relevant to Westpac shareholders.","title":"Shareholders","url":"/news/topic.shareholders/"},{"tagId":"newsroom:topics/climate","name":"climate","description":"Explore more climate insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Climate ","url":"/news/topic.climate/"},{"tagId":"newsroom:topics/esg","name":"esg","description":"Explore more insights on environmental, social and governance issues at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"ESG","url":"/news/topic.esg/"}]}