The government's Intergenerational Report found that Australia's ageing population was likely to lead to slower economic growth and bigger budget deficits if current policy settings remain broadly unchanged. (Getty)

The key message in the government’s 2023 Intergenerational Report is a familiar one: As Australia’s population ages, the birth rate and economic growth will slow, putting increasing pressure on public finances.

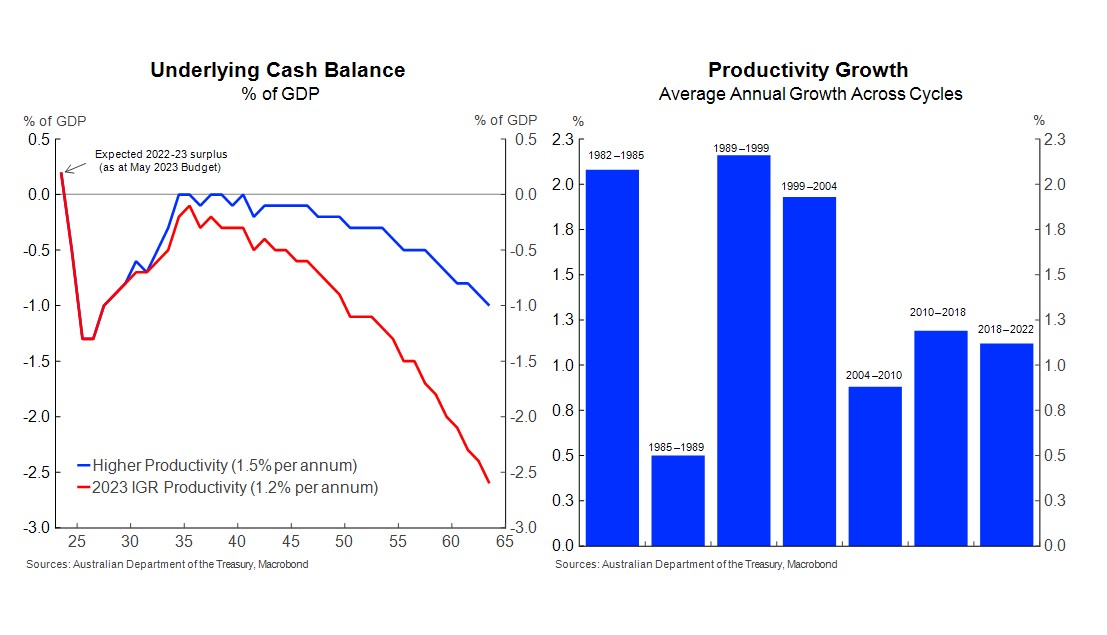

The projections provided in the IGR are sobering. The economy is expected to expand by an annual average rate of 2.2 per cent over the next 40 years, down from the 3.1 per cent recorded over the previous 40 years, while the budget bottom line is expected to go from a surplus in 2022-23 to a deficit of 2.6 per cent of GDP by 2062-63.

But it doesn’t have to be this way because the projections assume current policy settings remain broadly unchanged. It puts the onus on our policymakers and business leaders to grasp the nettle of reform, while harnessing technology to enable us to work smarter and more efficiently.

Failure to do so will see income growth slow over time and living standards fall.

An ageing population can put pressure on public finances in two ways. Firstly, by increasing government spending on provisions for health and aged care, and secondly by reducing the working age population, which lowers tax revenues.

A long-term sustainable way to keep growth and public finances on track is to improve productivity.

Productivity gains

In its simplest form, productivity refers to the output, or value, generated by a given set of inputs. Productivity increases when more value is created with the same set of inputs.

The potential gains are significant. The IGR estimates that if productivity gains were to run at an annual average rate of 1.5 per cent, rather than the assumed 1.2 per cent, the budget bottom line would improve by 1.6 per cent of GDP in 2062-63 – that’s close to $40 billion in today’s dollars. This will mean that on average working Australians will have higher incomes and pay a smaller share of their income in tax – a win, win.

But productivity doesn’t improve all by itself. It needs help from policy initiatives and regulatory reform, which take time to have an impact, as well as targeted investment from businesses.

Labor productivity - which measures the amount of output per hour of work – can be increased by better use of capital and new technology, as well as improving processes and workflow.

For example, hundreds of pharmacies across Australia have installed automatic dispensaries. This not only improves service time for prescriptions, it also gives the pharmacists more time for consultations with customers, improving the quality of the service.

Technology is a key part of the puzzle. The revolution in automation and artificial intelligence is fertile ground for productivity gains across a wide range of industries. Fast food chain McDonalds last year opened its first fully automated store in Texas using new technology to increase accuracy and order speed.

The key to unlocking these gains lies in allowing resources to flow freely to where they are valued most. That means removing any barriers and impediments, which can be done by reducing red tape and regulation.

And by removing barriers, you can also help improve competition. If businesses know new entrants can more easily enter markets, they will behave as if they are operating in a competitive market when it comes to taking risk, adopting new technologies and looking to innovate.

Investment challenge

Well targeted investment will also be vital in tackling the demographic challenges highlighted in the IGR. On that front, we need to be bolder - non-mining private business investment has gone sideways as a share of the economy since the end of the mining investment boom around 2012/13 .

Over the next 40 years the clean energy transition and artificial intelligence will give rise to new and exciting investment opportunities. While many of these will be of broad benefit to society, governments may have limited ability to use the public balance sheet to fund them, as they grapple with fiscal pressures.

As such, the private sector needs to pick up the slack, helping to fund investment in everything from large infrastructure projects to smaller capital works. We need policies that encourage the private sector to leverage its balance sheet and make these productivity-enhancing investments.

The choice is clear: under the status quo economic activity and income growth will slow and living standards fall. As a nation we need to be bold and innovative, embrace reform, and grasp the opportunities provided by technology to work smarter, not harder.

The 2023 Intergenerational Report, published by the Treasury, projects the outlook of the economy and the Australian Government’s budget to 2062-63.

Pat joined Westpac Group as a Senior Economist in August 2022. He covers a range of topics with a focus on the Australian economy and macroeconomic policy. He has also worked across several business lines, including Westpac Business Bank, St.George Bank, BankSA, Bank of Melbourne and BT. Prior to this, Pat was an economic adviser to the Federal Treasurer, the Hon Josh Frydenberg, during the COVID-19 pandemic. This involved advising the Federal Treasurer on the economy and appropriate macroeconomic policy settings, with a focus on taxation policy.

{"topicSelector":[{"tagId":"newsroom:topics/economy","name":"economy","description":"Explore more Economy insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Economy","url":"/news/topic.economy/"},{"tagId":"newsroom:topics/westpac","name":"westpac","description":"Stories featuring Westpac corporate news.","title":"Westpac","url":"/news/topic.westpac/"},{"tagId":"newsroom:topics/community","name":"community","description":"Explore more community insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Community","url":"/news/topic.community/"},{"tagId":"newsroom:topics/banking","name":"banking","description":"Explore more Banking insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Banking","url":"/news/topic.banking/"},{"tagId":"newsroom:topics/covid19","name":"covid19","description":"Stories influenced by the COVID-19 pandemic.","title":"COVID-19","url":"/news/topic.covid19/"},{"tagId":"newsroom:topics/sme","name":"sme","description":"Explore more Small Medium Enterprise insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"SME","url":"/news/topic.sme/"},{"tagId":"newsroom:topics/property","name":"property","description":"Explore more Property insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Property","url":"/news/topic.property/"},{"tagId":"newsroom:topics/diversity","name":"diversity","description":"Explore more Diversity insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Diversity","url":"/news/topic.diversity/"},{"tagId":"newsroom:topics/digital","name":"digital","description":"Explore more Digital insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Digital","url":"/news/topic.digital/"},{"tagId":"newsroom:topics/technology","name":"technology","description":"Explore more Technology insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Technology","url":"/news/topic.technology/"},{"tagId":"newsroom:topics/workplace","name":"workplace","description":"Explore more workplace insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Workplace","url":"/news/topic.workplace/"},{"tagId":"newsroom:topics/scams","name":"scams","description":"Stories about the latest cyber scams news and trends. ","title":"Scams","url":"/news/topic.scams/"},{"tagId":"newsroom:topics/sustainability","name":"sustainability","description":"Explore more sustainability insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Sustainability","url":"/news/topic.sustainability/"},{"tagId":"newsroom:topics/personalfinance","name":"personalfinance","description":"Explore more insights about personal finance, financial literacy and financial wellbeing. ","title":"Personal finance","url":"/news/topic.personalfinance/"},{"tagId":"newsroom:topics/career","name":"career","description":"Stories providing career insights, tips and trends.","title":"Career","url":"/news/topic.career/"},{"tagId":"newsroom:topics/billsbites","name":"billsbites","description":"Explore more insights from Bill Evans at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Bill\u0027s Bites","url":"/news/topic.billsbites/"},{"tagId":"newsroom:topics/social-enterprise","name":"social-enterprise","description":"Stories relevant to or featuring social enterprises.","title":"Social enterprise","url":"/news/topic.social-enterprise/"},{"tagId":"newsroom:topics/investing","name":"investing","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Investing","url":"/news/topic.investing/"},{"tagId":"newsroom:topics/leadership","name":"leadership","description":"Explore more Leadership insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Leadership","url":"/news/topic.leadership/"},{"tagId":"newsroom:topics/environment","name":"environment","description":"Explore more Environment insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Environment","url":"/news/topic.environment/"},{"tagId":"newsroom:topics/agribusiness","name":"agribusiness","description":"Explore more Agribusiness insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Agribusiness","url":"/news/topic.agribusiness/"},{"tagId":"newsroom:topics/wellbeing","name":"wellbeing","description":"Stories featuring wellbeing trends, insights and stories.","title":"Wellbeing","url":"/news/topic.wellbeing/"},{"tagId":"newsroom:topics/politics","name":"politics","description":"Explore more Politics insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Politics","url":"/news/topic.politics/"},{"tagId":"newsroom:topics/westpac-scholars","name":"westpac-scholars","description":"Stories featuring Westpac Scholars. ","title":"Westpac Scholars","url":"/news/topic.westpac-scholars/"},{"tagId":"newsroom:topics/innovators","name":"innovators","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Innovators","url":"/news/topic.innovators/"},{"tagId":"newsroom:topics/fintech","name":"fintech","description":"Explore more Fintech insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Fintech","url":"/news/topic.fintech/"},{"tagId":"newsroom:topics/data","name":"data","description":"Explore more data insights at Westpac Wire.","title":"Data","url":"/news/topic.data/"},{"tagId":"newsroom:topics/indigenous","name":"indigenous","description":"Explore more indigenous insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Indigenous","url":"/news/topic.indigenous/"},{"tagId":"newsroom:topics/payments","name":"payments","description":"Explore more Payments insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Payments","url":"/news/topic.payments/"},{"tagId":"newsroom:topics/history","name":"history","description":"Stories unearthed from Westpac\u0027s private archival collection. ","title":"History","url":"/news/topic.history/"},{"tagId":"newsroom:topics/podcast","name":"podcast","description":"Explore Westpac Wire\u0027s podcast series.","title":"Podcast","url":"/news/topic.podcast/"},{"tagId":"newsroom:topics/luciscall","name":"luciscall","description":"Explore more insights from Westpac\u0027s chief economist Luci Ellis at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Luci\u0027s Call","url":"/news/topic.luciscall/"},{"tagId":"newsroom:topics/startups","name":"startups","description":"Explore more Startups insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Startups","url":"/news/topic.startups/"},{"tagId":"newsroom:topics/currencies","name":"currencies","description":"Stories providing currencies insights, tips and trends.","title":"Currencies","url":"/news/topic.currencies/"},{"tagId":"newsroom:topics/opinion","name":"opinion","description":"Expert opinions and insights. ","title":"Opinion","url":"/news/topic.opinion/"},{"tagId":"newsroom:topics/asia","name":"asia","description":"Explore more Asia insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Asia","url":"/news/topic.asia/"},{"tagId":"newsroom:topics/analysis","name":"analysis","description":"Expert analysis on economic news and other trends.","title":"Analysis","url":"/news/topic.analysis/"},{"tagId":"newsroom:topics/superannuation","name":"superannuation","description":"Explore more Superannuation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Superannuation","url":"/news/topic.superannuation/"},{"tagId":"newsroom:topics/IWD","name":"IWD","description":"Stories focusing on International Women\u0027s Day, on 8 March annually. ","title":"IWD ","url":"/news/topic.IWD/"},{"tagId":"newsroom:topics/rework","name":"rework","description":"Stories of businesses pivoting in the face of the COVID-19 pandemic.","title":"Rework","url":"/news/topic.rework/"},{"tagId":"newsroom:topics/veterans","name":"veterans","description":"Explore more insights about defence force veterans at Westpac Wire.","title":"Veterans","url":"/news/topic.veterans/"},{"tagId":"newsroom:topics/commodities","name":"commodities","description":"Insights into commodities markets.","title":"Commodities","url":"/news/topic.commodities/"},{"tagId":"newsroom:topics/goodpair","name":"goodpair","description":"Explore more Good Pair stories, showing two people making a big difference together. ","title":"Good Pair","url":"/news/topic.goodpair/"},{"tagId":"newsroom:topics/10Qs","name":"10Qs","description":"\"10Qs with...\" is a series that asks leaders what makes them tick.","title":"10Qs","url":"/news/topic.10Qs/"},{"tagId":"newsroom:topics/deals","name":"deals","description":"Explore more Deals insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Deals","url":"/news/topic.deals/"},{"tagId":"newsroom:topics/regional","name":"regional","description":"Explore more Regional insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regional","url":"/news/topic.regional/"},{"tagId":"newsroom:topics/tax","name":"tax","description":"Explore more tax insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Tax","url":"/news/topic.tax/"},{"tagId":"newsroom:topics/regulation","name":"regulation","description":"Explore more Regulation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regulation","url":"/news/topic.regulation/"},{"tagId":"newsroom:topics/reinventure","name":"reinventure","description":"Explore more Reinventure insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Reinventure","url":"/news/topic.reinventure/"},{"tagId":"newsroom:topics/businesses-of-tomorrow","name":"businesses-of-tomorrow","description":"Stories featuring Westpac Businesses of Tomorrow program winners. ","title":"Westpac Businesses of Tomorrow","url":"/news/topic.businesses-of-tomorrow/"},{"tagId":"newsroom:topics/shareholders","name":"shareholders","description":"Stories relevant to Westpac shareholders.","title":"Shareholders","url":"/news/topic.shareholders/"},{"tagId":"newsroom:topics/climate","name":"climate","description":"Explore more climate insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Climate ","url":"/news/topic.climate/"},{"tagId":"newsroom:topics/esg","name":"esg","description":"Explore more insights on environmental, social and governance issues at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"ESG","url":"/news/topic.esg/"},{"tagId":"newsroom:topics/boardwalk","name":"boardwalk","description":"A series of in-depth podcast interviews with board directors to find out what\u0027s on their minds. ","title":"Board Walk","url":"/news/topic.boardwalk/"}]}