Sold! Big corporates speed up big pivot

Large listed Australian companies have recently been divesting major assets, such as Wesfarmers’ proposed demerger of Coles. (Getty)

A decade on from BHP Billiton’s monster bid for Rio Tinto in 2008, one of Australia’s biggest ever attempted takeovers, the nation’s largest listed companies are displaying a very different mood towards large deals.

It’s all about getting simpler, smaller and more tech savvy.

“The M&A of the future won’t be the M&A of the past,” says Jamie Garis, managing director of corporate advisory firm Luminis Partners. “For a lot of big companies, it’s going to be how you address the customer, the technology, the smarter plays and how you bring shareholders on that journey because they may not come cheap too.”

Wesfarmers made the latest move last week with plans to offload its UK business Homebase, less than two months after announcing the proposed demerger of its self-described “mature” Coles supermarkets business as part of a strategy to invest more capital in higher growth businesses.

Elsewhere, Telstra has announced plans to become a “world class technology company”, banks have been selling parts of wealth management operations and shareholders in Westfield Corporation last week waved through its $US24.7 billion sale to Unibail-Rodamco almost 60 years after being co-founded by Frank Lowy.

But a less high profile aspect of the Westfield deal included the spin-off of 90 per cent of OneMarket, the company’s early-stage retail technology company formerly known as Westfield Labs that would have around $US200 million of cash and be chaired by Mr Lowy’s son, Steven.

Westfield co-founder Frank Lowy may be selling Westfield Corporation, but the Lowy’s aren’t exiting corporate life. (Getty)

“OneMarket is an exciting technology business,” Frank Lowy told investors last week at his final annual general meeting, noting that the “evolution” of the retail environment meant retailers needed to find ways to compete more effectively.

“We are optimistic about the future of the business,” Mr Lowy continued about OneMarket, which intends to help bring together “retailers, shopping venues, brands and technology companies”.

Writing in The Australian Financial Review this month, Bennelong Australian Equity Partners investment director Julian Beaumont said the run of demergers and asset sales by large companies, including Rupert Murdoch’s move to sell the bulk of 21st Century Fox, was notable and being partly driven by the challenges they faced, including new and online competition. Other observers say global markets have further eaten away the benefits flowing from economies of scale.

Garis says many large incumbent companies with strong market positions weren’t only staring down technology disruption, but a second major theme: tightening regulation and compliance.

And the winds of change are blowing around the world.

The Fox Studios in Los Angeles, part of the 21st Century Fox assets slated for sale. (Getty)

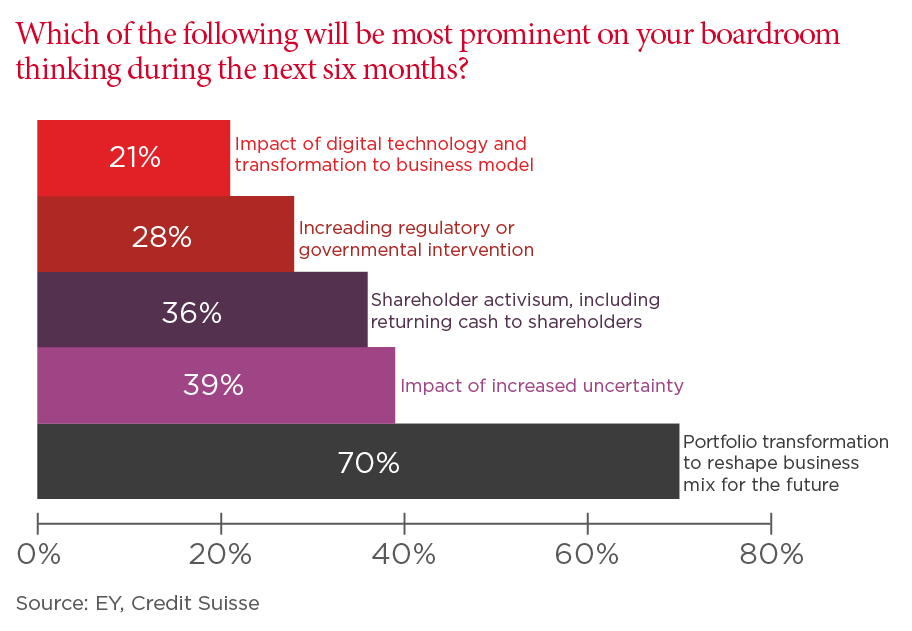

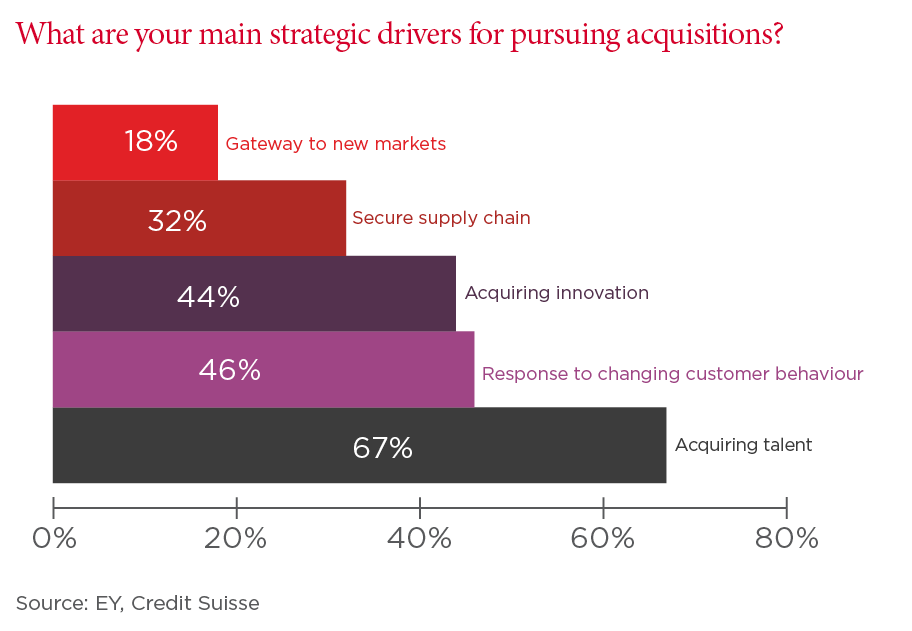

According to EY’s biannual Global Capital Confidence Barometer survey of more than 2500 executives released in April, 67 per cent cited talent acquisition as a main strategic driver for pursuing M&A and almost three-quarters saw portfolio transformation – buying and selling assets – as the top priority ahead for boards.

“Follow the smart money – people are keeping the capital light businesses that are new generation. When you see a Lowy or a Murdoch – two of the canniest investors of the last half century – exit legacy assets, then it is pause for thought as to the seismic changes we’re seeing across markets,” Garis says.

A quick trail of the money in recent times from Australia’s top 20 listed companies shows that while large acquisitions are mostly out, small investments are still in.

Alongside the rise of innovation labs and hubs in recent years, several large companies have set up or invested in venture capital funds to help best position for the fast evolving 21st century.

Westpac this month committed a further $50 million to venture capital group Reinventure for its third fund and a unit trust, building on the $100m already committed across two funds that have invested in 20 start-ups and technology-driven companies. The likes of National Australia Bank, IAG and Telstra also have so-called corporate venture capital, or CVC, groups to learn from and leverage new technologies.

While CVC’s have existed for some time and structures vary, NAB Ventures investment associate Lucinda Hankin told the CeBIT Australia conference in Sydney this month that corporates were primarily using them to invest in start-ups, founders and technologies where there was shared “strategic value”, which for the “big incumbents” included innovating faster and keeping up with rising customer expectations.

She said the strategic aspect was a key difference to more traditional venture capital funds, which were often solely focused on the financial return of an investment.

A company that has attracted both NAB Ventures and Reinventure is BRICKX, which buys properties and on-sells “bricks”, or an interest in the property, to investors. In a recent interview with Westpac Wire, BRICKX chief Anthony Millet said working with investors interested in its business was “about us having a joint alignment on a big dream on a big asset class that could actually have a really big impact on people”.

“As we see the banks move from being a product centric organisation to actually a customer centric organisation, if housing affordability, trying to save for a housing deposit is a problem and the banks don’t necessarily have within their wheel house the product that’s doing it, then by partnering with someone like a BRICKX is an opportunity to engage with people in a product that means something to them and help people achieve their goals,” he said.

Westpac chief Brian Hartzer cited Westpac’s recent rollout of new technology built in partnership with Assembly Payments – one of Reinventure’s first investments – at the bank’s interim results earlier this month. Some of the other investments in Reinventure’s portfolio are focused on cyber security, data, artificial intelligence and payments.

Westpac CEO Brian Hartzer says Reinventure’s investments are helping the bank leverage technology. (Emma Foster)

“While we do have a lot of effort going into the here and now of risk and compliance management, we've absolutely got an eye on setting Westpac up to thrive in the future,” Mr Hartzer said at the time.

According to a paper by US-based consulting group Bain last year, a key benefit of divestitures is the “fuel for the company to pump back into its core”. It also found those engaging in focused divestment outperformed “inactive companies” by about 15 per cent over a 10-year period, as measured by total shareholder return.

Closer to home, Wesfarmers, for example, made the point that the demerger of Coles would notably boost its return on capital, citing how 60 per cent of group capital employed was tied up in the supermarkets business, compared to the 34 per cent of group divisional earnings produced as at December.

Similar challenges are being felt across industries.

In a major report in March, a team of Morgan Stanley’s equity analysts found banks in Europe, the US, South Korea, Japan and Turkey could save $US35 billion in the coming three years and claimed "technology will be the future battleground for differentiation".

Locally in the wake of the big four banks’ recent results, Morgan Stanley’s Sydney-based analyst Richard Wiles said the industry had to lift near-term investment to navigate the risks and leverage the revenue opportunities that would flow from the collision of “fintech innovation, mobile banking adoption, real-time payments, open banking proposals and comprehensive credit reporting”.

Macquarie analyst Victor German added that the opportunities were large for the banks to “redefine” their cost bases. “The financial services industry is still heavily reliant on manual processes and should be a significant beneficiary of digitalisation and automation,” he says.

The trick, Garis says, for large companies doing small acquisitions and investments to leverage cost saving and technology opportunities lies in ensuring they pick the right ones, and manage the cultural and operational differences.

“Big companies do scale really well. But big companies and entrepreneurial growth companies can be a bit oil and water and to some extent there have been winners and losers from investments,” he says.

“Those that get the mx right and ingest these next gen companies but not strangle them I think will be the winners of tomorrow.”