Back in September at a lunch at Perth’s Hyatt Regency, Reserve Bank of Australia Governor Philip Lowe took the stage in front of a particularly receptive crowd.

The city had been at the heart of the mining investment boom, a period of record iron ore prices that Dr Lowe compared to the gold rush of the 1850s as Australia’s terms of trade soared to 150-year highs. Economic growth, jobs, wealth and confidence had flourished in a commodities cycle noone had ever experienced before. As previous RBA research showed, the boom “substantially increased Australian living standards” to the point where by 2013 real per capita household disposable income was up 13 per cent, real wages 6 per cent and the unemployment rate about 1.25 percentage points lower.

But as the investment boom petered out in recent years, Perth and other mining-exposed regions that arguably reaped the most riches have struggled the hardest.

“That boom, and its unwinding, has been central to the story of the Australian and Western Australian economies for more than a decade now,” Dr Lowe told diners in his speech “The Next Chapter”. “The new chapter will, almost certainly, have a different central theme.”

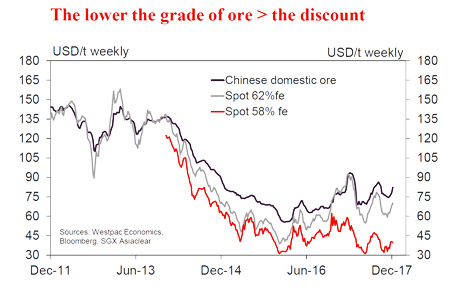

Source: Westpac Market Outlook 14 December 2017

As businesses grapple with similar questions around future drivers of growth, RBA Assistant Governor Luci Ellis last month furthered Dr Lowe’s sentiments in an address where she challenged ongoing talk that the economy required a “growth handover” from mining to housing construction, and now to infrastructure investment, and then to something else.

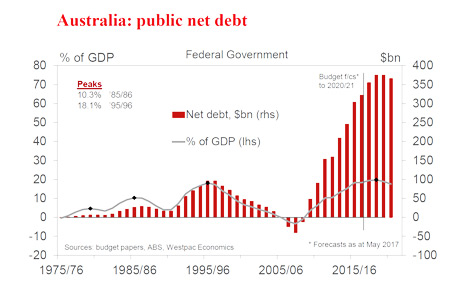

As 2017 comes to a close, the focus on future growth at a time of massive technological and demographic upheaval is intense across the nation, from business to politics to local communities. But with the mining boom in the rear view mirror, it’s occurring with a vastly different backdrop. According to Westpac’s economics research, the cumulative budget deficit from 2008-09 to 2016-17 came in at $350 billion, compared to a total surplus of $103bn in the eleven years to 2007-08 when the boom was firing up company tax revenues.

In a mid-year update this week, Treasurer Scott Morrison had some better news to end the year, projecting that the 2017-18 budget deficit would narrow to $23.6bn – some $5.8bn lower than the May Budget forecast – and pencilling in a larger return to surplus in 2021 on higher company tax revenue. The peak in government net debt of $363bn in 2018-19, equal to 19.2 per cent of GDP, was also lower than previously flagged, albeit about three times the average ratio recorded between 1971 and 2015, which included a few years of zero net debt in dollar terms just prior to the global financial crisis.

“We spent our windfall on the here and now,” think tank Per Capita argued in a 2012 paper into where the proceeds from the mining boom went.

Source: Westpac Bulletin 26 September 2017

From 2001-02 to 2007-08, Per Capita found that the boom generated a “windfall” to public coffers of at least $180bn over and above long-term GDP growth. They claimed that the Howard and Rudd governments used around $105bn paying off debt and funding long-term “savings vehicles”, such as The Future Fund. Around $25bn was used on tax cuts and concessions, such as fuel excise and voluntary superannuation contributions, while $50bn went towards various policy programs.

“It’s worth noting that even these numbers understate the size of the windfall - $180bn is a minimum estimate. Our analysis does not capture the scale of the tax concessions offered by changes made to superannuation tax arrangements in 2006,” the paper added.

The researchers took aim at the spending of the $75bn on tax cuts and policy programs, arguing it locked in reduced tax levels and increased spending that could not be sustained when economic circumstances inevitably changed. They cited how government spending to GDP grew from 22.1 per cent in 2002 to 25.4 per cent after the GFC hit and stimulus flowed.

In this week’s mid-year update, the government revealed this ratio would likely fall to 24.9 per cent of GDP by 2021, which it claimed was only slightly above the 30 year historical average.

The mining boom has been central to the story of the Australian economy more than a decade. (Getty)

In a note, UBS economist George Tharenou said the Mid-Year Economic & Fiscal Update “finally showed a turning point after a decade of fiscal slippage” that provided “some fiscal room for household tax cuts in the May-18 Budget”, a move recently flagged by the government.

Westpac economists, however, expressed caution around the government’s growth forecasts for the economy. They noted that while Westpac was a little more optimistic for this financial year, the economy would likely slowdown in 2018-19 to 2.5 per cent, below the government and the RBA’s forecasts, mainly due to their softer view on household consumption growth and residential construction.

Mr Morrison was upbeat and argued that growth was becoming “broader-based” as the global economy had further strengthened. Commodity prices were uncertain, he added, recognising how they can both positively and negatively affect the budget and debt position in a nation as rich in natural resources as Australia.

Looking further out in her November lecture, the RBA’s Ms Ellis also struck an upbeat tone and urged moving on from always searching for the “engines of growth” and “identifiable external triggers”. She pointed out that construction-related booms could only ever run for so long, that the mining investment boom had now triggered an exports boom and that other sectors, such as tourism and manufacturing, that had been “squeezed” out in prior years could help pick up the slack. Longer term, she said “underlying growth” would also be shaped by population, participation and productivity, or the “three P’s” economists have long claimed determined the ups and downs of economies.

“Next time somebody asks you ‘where’s the growth going to come from?', you can answer: ‘from all of us, trying new things, and gradually getting a bit better at what we do.’ We don't need to wait for something external to make it happen,” she implored.

For the next few years at least, Westpac chief economist Bill Evans this week reiterated his view that the RBA would hold the cash rate at a record low 1.5 per cent in 2018 and 2019. Or as Deutsche Bank economist Adam Boyton wrote this week ahead of a potential federal election next year: “The more interesting policy moves in 2018 may … end up being political and fiscal, as opposed to monetary.”

Michael Bennet was inaugural Editor of Westpac Wire from June 2017 to December 2021. He joined Westpac after more than 12 years in journalism, most recently at The Australian as the national newspaper’s banking reporter based in Sydney. Michael has worked at various News Corp publications and other media companies covering industries including financial services, resources, industrials, markets and economics. He is originally from Perth, Western Australia, where he also wrote across magazines covering the arts with a focus on music.

{"topicSelector":[{"tagId":"newsroom:topics/economy","name":"economy","description":"Explore more Economy insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Economy","url":"/news/topic.economy/"},{"tagId":"newsroom:topics/banking","name":"banking","description":"Explore more Banking insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Banking","url":"/news/topic.banking/"},{"tagId":"newsroom:topics/digital","name":"digital","description":"Explore more Digital insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Digital","url":"/news/topic.digital/"},{"tagId":"newsroom:topics/diversity","name":"diversity","description":"Explore more Diversity insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Diversity","url":"/news/topic.diversity/"},{"tagId":"newsroom:topics/community","name":"community","description":"Explore more community insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Community","url":"/news/topic.community/"},{"tagId":"newsroom:topics/workplace","name":"workplace","description":"Explore more workplace insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Workplace","url":"/news/topic.workplace/"},{"tagId":"newsroom:topics/sustainability","name":"sustainability","description":"Explore more sustainability insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Sustainability","url":"/news/topic.sustainability/"},{"tagId":"newsroom:topics/technology","name":"technology","description":"Explore more Technology insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Technology","url":"/news/topic.technology/"},{"tagId":"newsroom:topics/property","name":"property","description":"Explore more Property insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Property","url":"/news/topic.property/"},{"tagId":"newsroom:topics/westpac","name":"westpac","description":"Stories featuring Westpac corporate news.","title":"Westpac","url":"/news/topic.westpac/"},{"tagId":"newsroom:topics/sme","name":"sme","description":"Explore more Small Medium Enterprise insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"SME","url":"/news/topic.sme/"},{"tagId":"newsroom:topics/innovators","name":"innovators","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Innovators","url":"/news/topic.innovators/"},{"tagId":"newsroom:topics/leadership","name":"leadership","description":"Explore more Leadership insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Leadership","url":"/news/topic.leadership/"},{"tagId":"newsroom:topics/covid19","name":"covid19","description":"Stories influenced by the COVID-19 pandemic.","title":"COVID-19","url":"/news/topic.covid19/"},{"tagId":"newsroom:topics/investing","name":"investing","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Investing","url":"/news/topic.investing/"},{"tagId":"newsroom:topics/startups","name":"startups","description":"Explore more Startups insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Startups","url":"/news/topic.startups/"},{"tagId":"newsroom:topics/personalfinance","name":"personalfinance","description":"Explore more insights about personal finance, financial literacy and financial wellbeing. ","title":"Personal finance","url":"/news/topic.personalfinance/"},{"tagId":"newsroom:topics/agribusiness","name":"agribusiness","description":"Explore more Agribusiness insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Agribusiness","url":"/news/topic.agribusiness/"},{"tagId":"newsroom:topics/scams","name":"scams","description":"Stories about the latest cyber scams news and trends. ","title":"Scams","url":"/news/topic.scams/"},{"tagId":"newsroom:topics/billsbites","name":"billsbites","description":"Explore more insights from Bill Evans at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Bill\u0027s Bites","url":"/news/topic.billsbites/"},{"tagId":"newsroom:topics/data","name":"data","description":"Explore more data insights at Westpac Wire.","title":"Data","url":"/news/topic.data/"},{"tagId":"newsroom:topics/environment","name":"environment","description":"Explore more Environment insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Environment","url":"/news/topic.environment/"},{"tagId":"newsroom:topics/payments","name":"payments","description":"Explore more Payments insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Payments","url":"/news/topic.payments/"},{"tagId":"newsroom:topics/fintech","name":"fintech","description":"Explore more Fintech insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Fintech","url":"/news/topic.fintech/"},{"tagId":"newsroom:topics/politics","name":"politics","description":"Explore more Politics insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Politics","url":"/news/topic.politics/"},{"tagId":"newsroom:topics/career","name":"career","description":"Stories providing career insights, tips and trends.","title":"Career","url":"/news/topic.career/"},{"tagId":"newsroom:topics/social-enterprise","name":"social-enterprise","description":"Stories relevant to or featuring social enterprises.","title":"Social enterprise","url":"/news/topic.social-enterprise/"},{"tagId":"newsroom:topics/indigenous","name":"indigenous","description":"Explore more indigenous insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Indigenous","url":"/news/topic.indigenous/"},{"tagId":"newsroom:topics/regulation","name":"regulation","description":"Explore more Regulation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regulation","url":"/news/topic.regulation/"},{"tagId":"newsroom:topics/wellbeing","name":"wellbeing","description":"Stories featuring wellbeing trends, insights and stories.","title":"Wellbeing","url":"/news/topic.wellbeing/"},{"tagId":"newsroom:topics/superannuation","name":"superannuation","description":"Explore more Superannuation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Superannuation","url":"/news/topic.superannuation/"},{"tagId":"newsroom:topics/westpac-scholars","name":"westpac-scholars","description":"Stories featuring Westpac Scholars. ","title":"Westpac Scholars","url":"/news/topic.westpac-scholars/"},{"tagId":"newsroom:topics/reinventure","name":"reinventure","description":"Explore more Reinventure insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Reinventure","url":"/news/topic.reinventure/"},{"tagId":"newsroom:topics/asia","name":"asia","description":"Explore more Asia insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Asia","url":"/news/topic.asia/"},{"tagId":"newsroom:topics/podcast","name":"podcast","description":"Explore Westpac Wire\u0027s podcast series.","title":"Podcast","url":"/news/topic.podcast/"},{"tagId":"newsroom:topics/history","name":"history","description":"Stories unearthed from Westpac\u0027s private archival collection. ","title":"History","url":"/news/topic.history/"},{"tagId":"newsroom:topics/businesses-of-tomorrow","name":"businesses-of-tomorrow","description":"Stories featuring Westpac Businesses of Tomorrow program winners. ","title":"Westpac Businesses of Tomorrow","url":"/news/topic.businesses-of-tomorrow/"},{"tagId":"newsroom:topics/tax","name":"tax","description":"Explore more tax insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Tax","url":"/news/topic.tax/"},{"tagId":"newsroom:topics/luciscall","name":"luciscall","description":"Explore more insights from Westpac\u0027s chief economist Luci Ellis at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Luci\u0027s Call","url":"/news/topic.luciscall/"},{"tagId":"newsroom:topics/goodpair","name":"goodpair","description":"Explore more Good Pair stories, showing two people making a big difference together. ","title":"Good Pair","url":"/news/topic.goodpair/"},{"tagId":"newsroom:topics/opinion","name":"opinion","description":"Expert opinions and insights. ","title":"Opinion","url":"/news/topic.opinion/"},{"tagId":"newsroom:topics/currencies","name":"currencies","description":"Stories providing currencies insights, tips and trends.","title":"Currencies","url":"/news/topic.currencies/"},{"tagId":"newsroom:topics/deals","name":"deals","description":"Explore more Deals insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Deals","url":"/news/topic.deals/"},{"tagId":"newsroom:topics/veterans","name":"veterans","description":"Explore more insights about defence force veterans at Westpac Wire.","title":"Veterans","url":"/news/topic.veterans/"},{"tagId":"newsroom:topics/analysis","name":"analysis","description":"Expert analysis on economic news and other trends.","title":"Analysis","url":"/news/topic.analysis/"},{"tagId":"newsroom:topics/IWD","name":"IWD","description":"Stories focusing on International Women\u0027s Day, on 8 March annually. ","title":"IWD ","url":"/news/topic.IWD/"},{"tagId":"newsroom:topics/rework","name":"rework","description":"Stories of businesses pivoting in the face of the COVID-19 pandemic.","title":"Rework","url":"/news/topic.rework/"},{"tagId":"newsroom:topics/10Qs","name":"10Qs","description":"\"10Qs with...\" is a series that asks leaders what makes them tick.","title":"10Qs","url":"/news/topic.10Qs/"},{"tagId":"newsroom:topics/commodities","name":"commodities","description":"Insights into commodities markets.","title":"Commodities","url":"/news/topic.commodities/"},{"tagId":"newsroom:topics/quarterlife","name":"quarterlife","description":"Explore more Quarter Life insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Quarter Life","url":"/news/topic.quarterlife/"},{"tagId":"newsroom:topics/shareholders","name":"shareholders","description":"Stories relevant to Westpac shareholders.","title":"Shareholders","url":"/news/topic.shareholders/"},{"tagId":"newsroom:topics/climate","name":"climate","description":"Explore more climate insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Climate ","url":"/news/topic.climate/"},{"tagId":"newsroom:topics/esg","name":"esg","description":"Explore more insights on environmental, social and governance issues at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"ESG","url":"/news/topic.esg/"},{"tagId":"newsroom:topics/boardwalk","name":"boardwalk","description":"A series of in-depth podcast interviews with board directors to find out what\u0027s on their minds. ","title":"Board Walk","url":"/news/topic.boardwalk/"}]}