To drive innovation through SMEs, start up businesses in Australia need more options to access funding overall, says Business Bank Chief Executive, David Lindberg. (Getty Images)

In many ways, the saying “the more things change, the more they stay the same” says a lot about the economy and banking today – if you flip it.

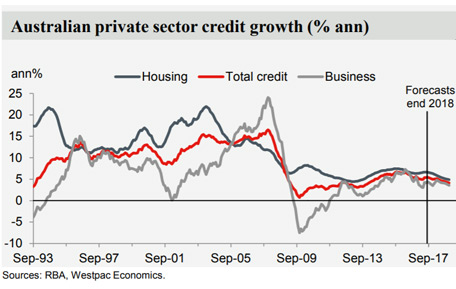

On the surface, everything looks the same. GDP growth, unemployment, interest rates and the outlook for business credit growth – it’s all roughly in line with a year ago.

But on the ground, so much is changing for business.

Services – for example tourism, hospitality, health – now comprise roughly 70 per cent of the Australian economy and employ nine out of 10 people, up from 60 per cent and eight, respectively, just three years ago.

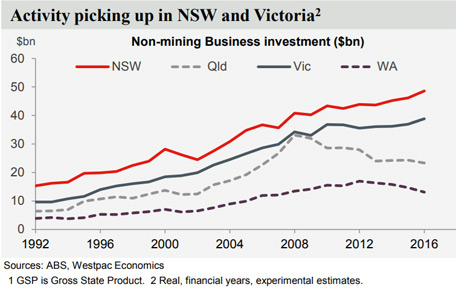

Of course, conditions have varied across the nation with a clear shift from the west of the country to the east as the end of the mining investment boom and challenges in regional economies coincided with stronger growth in Sydney and Melbourne.

But perhaps one of the biggest changes in recent times is that small businesses are now firmly the engine room of the economy, making up 96 of all Australian businesses and employing more than 4.5 million people.

In fact, for the third year in a row, credit growth in our portfolio will be three times faster in SME than the larger end of town as Westpac continues to support the sector. And the majority of these small businesses are serving other small businesses with a lot of the engagement with large businesses being around collaboration as they outsource a lot of innovation to SMEs.

Recently, talk has again emerged that banks are withholding funding from SMEs. It’s actually a far from new debate, having been around since at least the 1960s when The Vernon Committee of Economic Inquiry (1965) was conducted. And even though several inquiries have been done since, the recent reigniting of the debate is unwarranted.

Some facts around the issue may help explain why.

At Westpac, we currently approve 93 per cent of loan applications from SMEs, in line with our average approval rate since 2009. Similarly, Deloitte estimates suggest that approximately 90 per cent of SMEs do not have a problem accessing finance. Our SME loan book is currently $50 billion with another $30bn pre-approved finance ready to support demand, and last year grew at 6 per cent, faster than our broader business lending growth of 4 per cent, which was in line with the market.

Many observers claim that new capital regulations have led banks to shun business lending in favour of home loans, or that lending is constrained by banks’ slow and cumbersome processes.

But our experience suggests these claims are untrue. While banks are required to hold more capital for business loans, in general, than mortgages, our approval rates and growth rates show we are committed to supporting SMEs and efficiently allocating capital to areas of the economy with the strongest demand, increasingly from sectors such as agribusiness, healthcare, education and professional services. And many of these loans have also been on great terms amid increased competition in business lending that has driven interest rates down to their lowest absolute level since the early 1990s.

On the technology front, we have invested heavily to improve customer experience and processes, in the last financial year alone providing $2.5bn in loans to SMEs through LOLA, a simplified online loan platform that reduces processing times and credit decisions for customers. Other initiatives that support businesses include Westpac Live for Business, Genie and Connect Now, as well as partnerships such as Assembly, Lantern Pay, and Flare HR.

Westpac business bank chief executive David Lindberg speaking yesterday at an event in Sydney.

The business bank’s vision is to help make Australian businesses stronger. But we have to ensure we continue to lend responsibly and in the best interests of our customers.

To drive innovation through SMEs, start up businesses in Australia need more options to access funding overall, particularly equity via the likes of venture capital, crowdfunding, angel investors and high net worth individuals. Equity funding is less risky for the business owner, presents networking and mentoring opportunities, and helps with cash flow. As a nation, we need to do more to connect SMEs with different funding avenues, assist with financial literacy, and assist them to navigate and take advantage of the mega trends that are shaping our economy.

It’s worth remembering that most small established businesses do not borrow. For example, currently only one third of Westpac’s existing SME customer base have a business debt facility, as they often use internal equity and funding sourced from family.

In my view, all lending entities must meet responsible lending standards and allocate capital efficiently, which is why in other nations like the UK we’ve seen government initiatives tend to largely provide equity, guarantees alongside other financial institutions or small loans, in the scheme of things, to start-ups.

The number one thing our small business customers tell us they want from government is a reasonable reduction to red tape and a realisation that regulation is cumulative and sometimes a burden on their ability to conduct business.

That would enable businesses to respond to the rapid technological change occurring across all industries.

A new Westpac Future of Business (2017) report by Deloitte Access Economics found the adoption of new technology to be the biggest factor over the horizon for businesses in the next decade, ahead of changes in customers, staff and business systems. The two biggest I believe all businesses must embrace -- and not fear - are robotics and artificial intelligence, impacting Australia’s future.

The manufacturing sector for example, which has struggled since the GFC, still has enormous potential to grow through the use of robotics. It could be one of the turnaround stories of the next decade and we are already starting to see a revival, particularly in SA. It will be critical for these businesses to transition from traditional to advanced manufacturing in coming years, and we are ready to lend more to these businesses so they can seize these opportunities.

Also, think about the demographic problem we are facing – in 1975, there were 7.3 Australian workers for every one senior citizen over the age of 65 whereas in 2055 that number's going to fall to 2.7 workers for every senior in society. Automation has to play a role in creating efficiency and should be seen as an opportunity to make businesses better, not something to fear.

Fortunately business confidence is good and on a global scale we are doing well against our competitors. Our agricultural industry feeds millions of people.

Our resources sector helps build new cities. Our health and pharma industry has won many battles against disease and injury. And our technology sector is using our information to drive innovation across all industries.

More change is a given even though things may appear much the same. By taking steps to unlock their full potential and focusing on the bigger picture of the major trends of China, demographics and technology, Australian businesses will be well placed to meet the challenges and opportunities of the future.

David was appointed Chief Executive, Consumer in April 2019, responsible for all consumer distribution, digital, marketing, banking and insurance products and services under the Westpac, St.George, BankSA, Bank of Melbourne, BT, and RAMS brands. Prior to this, David was Chief Executive, Business Bank from June 2015, after three years as Chief Product Officer for the Group’s retail and business products, as well as overseeing the Group’s digital activities. Before joining Westpac in 2012, David was Executive General Manager, Cards, Payments & Retail Strategy at the Commonwealth Bank of Australia. David was also formerly Managing Director, Strategy, Marketing & Customer Segmentation at Australia and New Zealand Banking Group Limited and Vice President and Head of Australia for First Manhattan.

{"topicSelector":[{"tagId":"newsroom:topics/economy","name":"economy","description":"Explore more Economy insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Economy","url":"/news/topic.economy/"},{"tagId":"newsroom:topics/banking","name":"banking","description":"Explore more Banking insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Banking","url":"/news/topic.banking/"},{"tagId":"newsroom:topics/digital","name":"digital","description":"Explore more Digital insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Digital","url":"/news/topic.digital/"},{"tagId":"newsroom:topics/diversity","name":"diversity","description":"Explore more Diversity insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Diversity","url":"/news/topic.diversity/"},{"tagId":"newsroom:topics/community","name":"community","description":"Explore more community insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Community","url":"/news/topic.community/"},{"tagId":"newsroom:topics/workplace","name":"workplace","description":"Explore more workplace insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Workplace","url":"/news/topic.workplace/"},{"tagId":"newsroom:topics/sustainability","name":"sustainability","description":"Explore more sustainability insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Sustainability","url":"/news/topic.sustainability/"},{"tagId":"newsroom:topics/technology","name":"technology","description":"Explore more Technology insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Technology","url":"/news/topic.technology/"},{"tagId":"newsroom:topics/property","name":"property","description":"Explore more Property insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Property","url":"/news/topic.property/"},{"tagId":"newsroom:topics/westpac","name":"westpac","description":"Stories featuring Westpac corporate news.","title":"Westpac","url":"/news/topic.westpac/"},{"tagId":"newsroom:topics/sme","name":"sme","description":"Explore more Small Medium Enterprise insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"SME","url":"/news/topic.sme/"},{"tagId":"newsroom:topics/innovators","name":"innovators","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Innovators","url":"/news/topic.innovators/"},{"tagId":"newsroom:topics/leadership","name":"leadership","description":"Explore more Leadership insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Leadership","url":"/news/topic.leadership/"},{"tagId":"newsroom:topics/covid19","name":"covid19","description":"Stories influenced by the COVID-19 pandemic.","title":"COVID-19","url":"/news/topic.covid19/"},{"tagId":"newsroom:topics/investing","name":"investing","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Investing","url":"/news/topic.investing/"},{"tagId":"newsroom:topics/startups","name":"startups","description":"Explore more Startups insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Startups","url":"/news/topic.startups/"},{"tagId":"newsroom:topics/personalfinance","name":"personalfinance","description":"Explore more insights about personal finance, financial literacy and financial wellbeing. ","title":"Personal finance","url":"/news/topic.personalfinance/"},{"tagId":"newsroom:topics/agribusiness","name":"agribusiness","description":"Explore more Agribusiness insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Agribusiness","url":"/news/topic.agribusiness/"},{"tagId":"newsroom:topics/scams","name":"scams","description":"Stories about the latest cyber scams news and trends. ","title":"Scams","url":"/news/topic.scams/"},{"tagId":"newsroom:topics/billsbites","name":"billsbites","description":"Explore more insights from Bill Evans at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Bill\u0027s Bites","url":"/news/topic.billsbites/"},{"tagId":"newsroom:topics/data","name":"data","description":"Explore more data insights at Westpac Wire.","title":"Data","url":"/news/topic.data/"},{"tagId":"newsroom:topics/environment","name":"environment","description":"Explore more Environment insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Environment","url":"/news/topic.environment/"},{"tagId":"newsroom:topics/payments","name":"payments","description":"Explore more Payments insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Payments","url":"/news/topic.payments/"},{"tagId":"newsroom:topics/fintech","name":"fintech","description":"Explore more Fintech insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Fintech","url":"/news/topic.fintech/"},{"tagId":"newsroom:topics/politics","name":"politics","description":"Explore more Politics insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Politics","url":"/news/topic.politics/"},{"tagId":"newsroom:topics/career","name":"career","description":"Stories providing career insights, tips and trends.","title":"Career","url":"/news/topic.career/"},{"tagId":"newsroom:topics/social-enterprise","name":"social-enterprise","description":"Stories relevant to or featuring social enterprises.","title":"Social enterprise","url":"/news/topic.social-enterprise/"},{"tagId":"newsroom:topics/indigenous","name":"indigenous","description":"Explore more indigenous insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Indigenous","url":"/news/topic.indigenous/"},{"tagId":"newsroom:topics/regulation","name":"regulation","description":"Explore more Regulation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regulation","url":"/news/topic.regulation/"},{"tagId":"newsroom:topics/wellbeing","name":"wellbeing","description":"Stories featuring wellbeing trends, insights and stories.","title":"Wellbeing","url":"/news/topic.wellbeing/"},{"tagId":"newsroom:topics/superannuation","name":"superannuation","description":"Explore more Superannuation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Superannuation","url":"/news/topic.superannuation/"},{"tagId":"newsroom:topics/westpac-scholars","name":"westpac-scholars","description":"Stories featuring Westpac Scholars. ","title":"Westpac Scholars","url":"/news/topic.westpac-scholars/"},{"tagId":"newsroom:topics/asia","name":"asia","description":"Explore more Asia insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Asia","url":"/news/topic.asia/"},{"tagId":"newsroom:topics/podcast","name":"podcast","description":"Explore Westpac Wire\u0027s podcast series.","title":"Podcast","url":"/news/topic.podcast/"},{"tagId":"newsroom:topics/history","name":"history","description":"Stories unearthed from Westpac\u0027s private archival collection. ","title":"History","url":"/news/topic.history/"},{"tagId":"newsroom:topics/businesses-of-tomorrow","name":"businesses-of-tomorrow","description":"Stories featuring Westpac Businesses of Tomorrow program winners. ","title":"Westpac Businesses of Tomorrow","url":"/news/topic.businesses-of-tomorrow/"},{"tagId":"newsroom:topics/tax","name":"tax","description":"Explore more tax insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Tax","url":"/news/topic.tax/"},{"tagId":"newsroom:topics/luciscall","name":"luciscall","description":"Explore more insights from Westpac\u0027s chief economist Luci Ellis at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Luci\u0027s Call","url":"/news/topic.luciscall/"},{"tagId":"newsroom:topics/goodpair","name":"goodpair","description":"Explore more Good Pair stories, showing two people making a big difference together. ","title":"Good Pair","url":"/news/topic.goodpair/"},{"tagId":"newsroom:topics/opinion","name":"opinion","description":"Expert opinions and insights. ","title":"Opinion","url":"/news/topic.opinion/"},{"tagId":"newsroom:topics/currencies","name":"currencies","description":"Stories providing currencies insights, tips and trends.","title":"Currencies","url":"/news/topic.currencies/"},{"tagId":"newsroom:topics/deals","name":"deals","description":"Explore more Deals insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Deals","url":"/news/topic.deals/"},{"tagId":"newsroom:topics/veterans","name":"veterans","description":"Explore more insights about defence force veterans at Westpac Wire.","title":"Veterans","url":"/news/topic.veterans/"},{"tagId":"newsroom:topics/analysis","name":"analysis","description":"Expert analysis on economic news and other trends.","title":"Analysis","url":"/news/topic.analysis/"},{"tagId":"newsroom:topics/IWD","name":"IWD","description":"Stories focusing on International Women\u0027s Day, on 8 March annually. ","title":"IWD ","url":"/news/topic.IWD/"},{"tagId":"newsroom:topics/rework","name":"rework","description":"Stories of businesses pivoting in the face of the COVID-19 pandemic.","title":"Rework","url":"/news/topic.rework/"},{"tagId":"newsroom:topics/10Qs","name":"10Qs","description":"\"10Qs with...\" is a series that asks leaders what makes them tick.","title":"10Qs","url":"/news/topic.10Qs/"},{"tagId":"newsroom:topics/commodities","name":"commodities","description":"Insights into commodities markets.","title":"Commodities","url":"/news/topic.commodities/"},{"tagId":"newsroom:topics/quarterlife","name":"quarterlife","description":"Explore more Quarter Life insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Quarter Life","url":"/news/topic.quarterlife/"},{"tagId":"newsroom:topics/shareholders","name":"shareholders","description":"Stories relevant to Westpac shareholders.","title":"Shareholders","url":"/news/topic.shareholders/"},{"tagId":"newsroom:topics/climate","name":"climate","description":"Explore more climate insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Climate ","url":"/news/topic.climate/"},{"tagId":"newsroom:topics/esg","name":"esg","description":"Explore more insights on environmental, social and governance issues at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"ESG","url":"/news/topic.esg/"}]}