3 steps in planning to fund my child’s education

Minutes to read: 4 minutes

Minutes to read: 4 minutes

Having a child can be a wonderful experience bringing love and joy to many families. And like many people we want the best for our children including a good school education.

To get the education we want for our children it is going to cost money. To have a good chance of having the money, like many things in life, it helps to set goals and plan for it. And the sooner you do this, the more achievable it will be.

A good education means different things to different people. There are lot of factors that go into deciding which school we send out children to. These may include, where we live, where we went to school, where our children’s friends are going to school, our child’s needs, how far is the school, convenience, the principal, teachers and the school, the academic results of the school and how much it will cost.

Will our children go to the same school from kindergarten to year 12 or will they go to one kindergarten / primary school and then a different high school?

For some people, this choice is simple and easy, for others they can tend to agonise and debate this for some time. Whichever type of parent you are, you will come to a decision and it will probably be the right one for your children.

Whatever choice we make for our children’s education it will cost money. Not just the school fees, but other education costs such as:

Your child is likely to be at school for 13 years (Kindergarten to Year 12) and according to the Futurity Investment Group Planning for Education Index the total national estimated average cost of education for a child starting school in 2021 split between capital city school and regional schools are:

| Government | Catholic | Independent | |

|---|---|---|---|

| Capital city | $81,823 |

$140,433 |

$340,882 |

| Regional | $66,603 |

$107,678 |

$140,197 |

These costs are an average only and will vary from state to state and school to school. For example, the average cost for an independent school in Sydney is $448,035 over those 13 years. We recommend you investigate the costs with the schools you have chosen taking all education costs into consideration.

And while you may not be able to change the school fees of the school you choose, you may be able to save money in other areas, by purchasing 2nd hand clothing, textbooks and computer/tablets or shopping around for better deals on these items. Planning ahead for the school year and picking up stationery and other required materials when they are on sale can also save you money.

It is a good idea to revisit your cost estimate each year as education costs are likely to increase and have increased faster than inflation in the past.

Once your school has been chosen and your estimated costs identified you have a clear goal to focus on and it is time to set up your education savings plan.

Firstly, find out how much you need to save each pay period, by taking your estimated total cost of education and dividing it by how many years until your child finishes year 12.

The example below (using the Futurity Investment Group Planning for Education Index) shows the difference in how much needs to be saved regularly if you start saving when your child is born as opposed to when they start school.

| Government School | Catholic School | Independent School | |

|---|---|---|---|

| Estimated cost for (Kindergarten to Year 12) 13 years | $81,823 | $140,433 | $340,882 |

| Start when child is born | 18 years | 18 years | 18 years |

| Save Yearly1 | $4,546 | $7,802 | $18,938 |

| Save Monthly1 | $379 | $651 | $1,579 |

| Save Weekly1 | $88 | $151 | $365 |

| Start when child starts school | 13 years | 13 years | 13 years |

| Save Yearly1 | $6,295 | $10,803 | $26,222 |

| Save Monthly1 | $525 | $901 | $2186 |

| Save Weekly1 | $122 | $208 | $505 |

Having done this calculation, you have a good idea how much you need to regularly save.

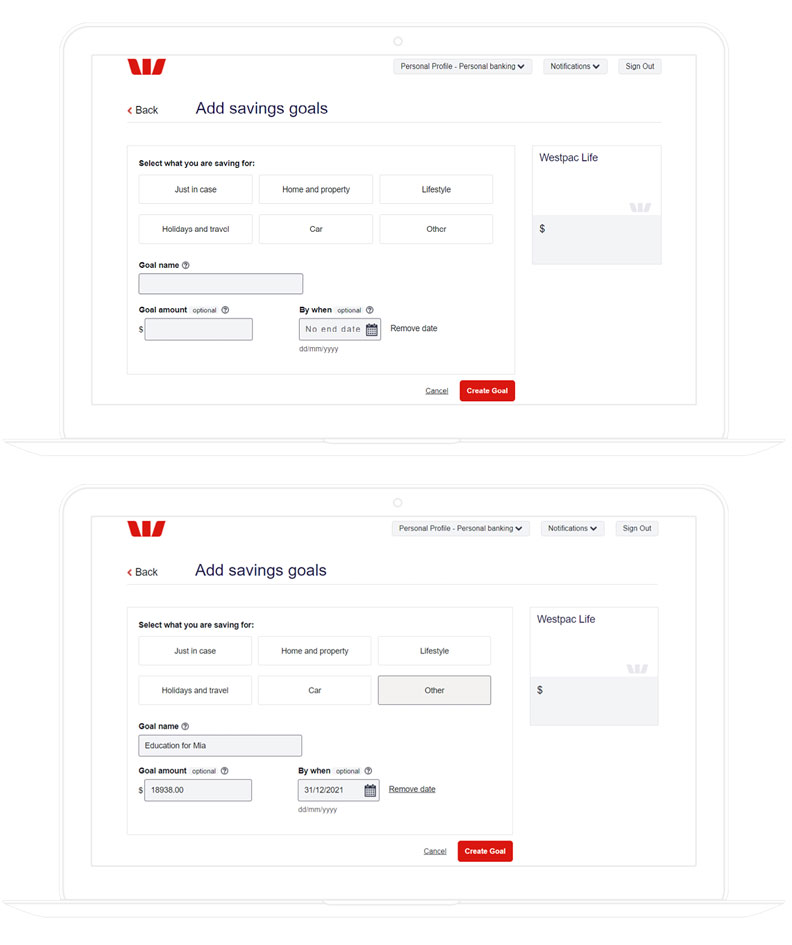

To reach any savings goals, it can help if you put the money aside into a separate account that will make you pause and think before spending it.

Set up a recurring transfer into the account to make the saving automatic. If you set the transfer up on the same day you get paid it will not take long before you do not miss the money in your everyday bank account.

If you can name the account that you are transferring the money into, such as “Education for Mia”, it can help in keeping you focused on the goal and not using the money for other purposes.

Use an annual target to aim for, instead of the whole target. An annual target is less scary than the whole 13 years of education. It also allows you to change the target each year due to changing circumstances.

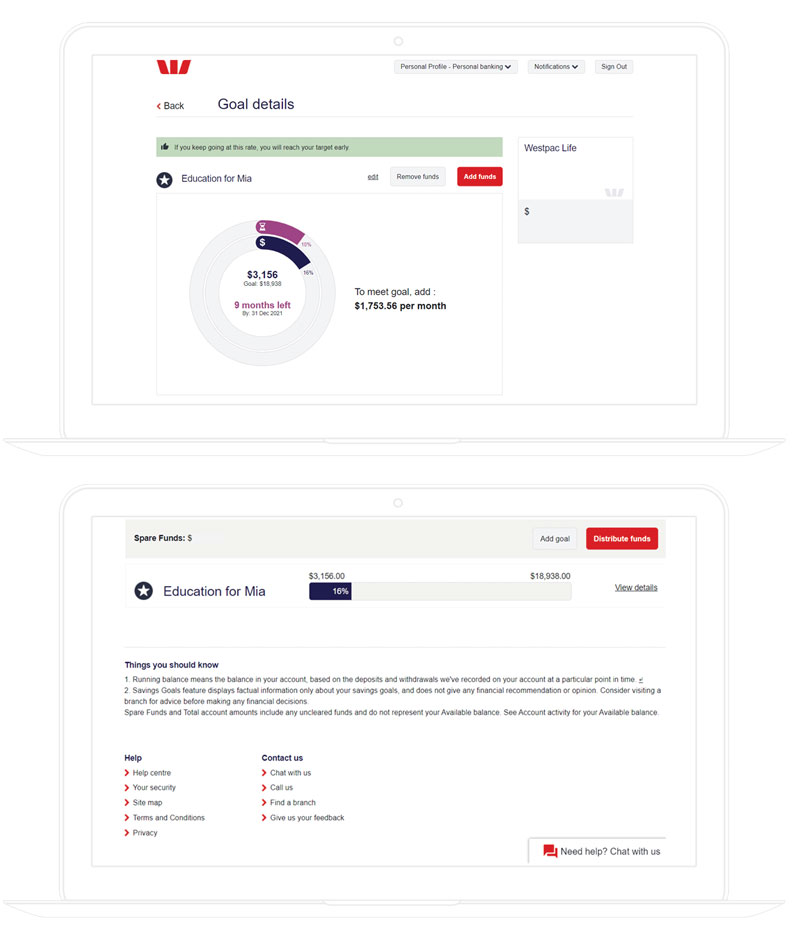

Once you have set up your goals, targets and recurring transfers set up it can help you stick to your goal by checking on your progress every now and then. Some people find checking their balances are enough while others find a visual representation such as the example from the Westpac Life account below.

Saving for your child’s education may help reduce any financial stress you may feel and allow you and your child to concentrate on getting the education they deserve.

1 All calculation results have been rounded up to the nearest dollar.

This article is from Westpac’s financial education specialists, continuing the legacy of Sir Alfred Davidson in helping you create a better financial future.

This information is general in nature and has been prepared without taking your objectives, needs and overall financial situation into account. For this reason, you should consider the appropriateness or the information to your own circumstances and, if necessary, seek appropriate professional advice.

The taxation position described is a general statement and should only be used as a guide. It does not constitute tax advice and is based on current tax laws and their interpretation.