Home Loan Portability

When you’re selling a property and buying a new one, your home loan may be able to move with you, saving you all the hassles of refinancing.

What is Portability?

Portability is a home loan feature that allows you to keep your home loan when selling by changing the property securing the mortgage from your current property to a new one. Sometimes called a substitution of security, it means you can avoid all the hassles and costs involved with refinancing and opening a new home loan. It also gives you the flexibility to fix your interest rate when you want. If you require an increase to the loan, this must be done either before, or after the application has been finalised - remember if you have a fixed rate loan, break costs may apply.

Why portability could be your home loan’s superpower

No hassles

Keep your current home loan to keep your interest rate, repayments, features and set-ups, like direct debit and offset.

No break costs

You can avoid break costs on your fixed rate home loan when replacing the security (property tied to your loan), as long as no other changes are made to the loan.

Avoid upfront costs

By porting your home loan you could save both time and money, avoiding the potential upfront costs of a new loan.

Faster turnaround

Porting your loan reduces both prep and paperwork, meaning it’s generally faster than applying for a new loan.

How do I get started?

Westpac home loan portability application

How to complete the online form

Once you’ve spoken to a home loan expert, you can port your Westpac home loan by applying online for a change of security. Provide details of:

1. The representative or home loan expert that you’ve spoken to

2. Your current property and new property (if available), including settlement dates

3. Ensure you request to keep your loan open

4. Under Additional information please type Application for portability.

We’ll then get back in touch with you.

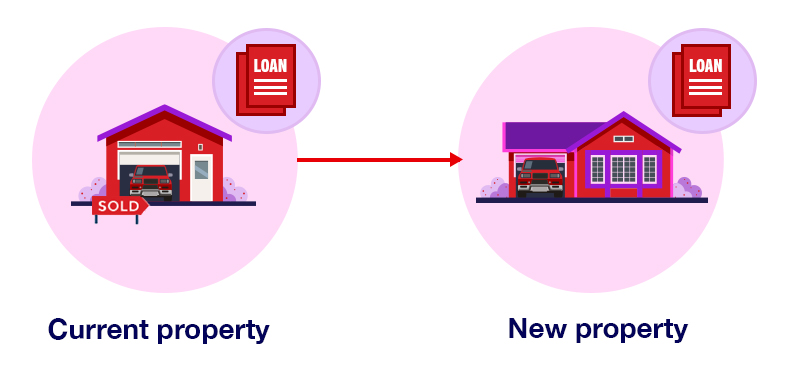

Two ways to use portability on your home loan

How same time settlement works

Use this option when you’re buying and selling at the same time, for an easy transfer of your home loan security.

Your current property is held as security on your existing mortgage. When you sell and buy a new property, the settlement dates are aligned, meaning the loan security is simply transferred from your current property to the new property. All you need to do is keep paying your home loan repayments as normal.

To apply for same time settlement

After contacting your local home loan expert, you’ll need to complete the Property and Security Request Form before you sell your current property or buy your new one. Provide details of:

1. The representative or home loan expert that you’ve spoken to

2. Your current and new properties including settlement date

3. Ensure you request to keep your loan open

4. Under Additional information please type Application for portability.

We’ll then be in touch with next steps.

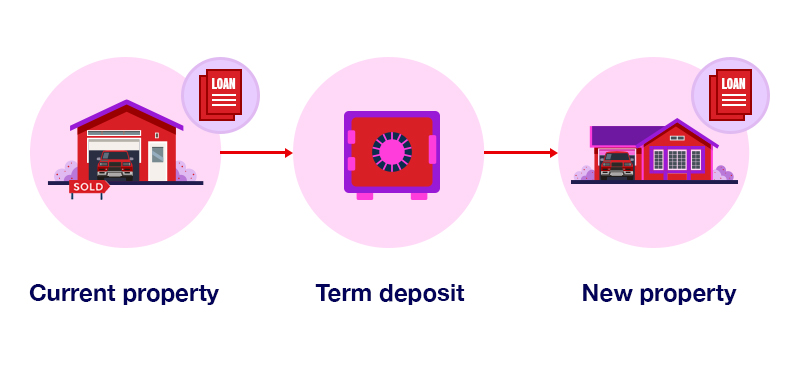

How deferred settlement works

When you’ve sold but not bought yet, or you’re waiting for settlement, this option gives you up to 6 months extra.

You’ve sold your current property, but not bought or settled yet on a new property, meaning there is no property to secure against the existing mortgage. That’s when a term deposit can be set up to use as security against the mortgage for up to 6 months (conditions apply). Then once you’re ready to settle on the new property, the term deposit is closed and the loan security is transferred over to the new property. Throughout the whole process, all you need to do is keep paying your home loan repayments as normal.

To apply for deferred settlement

After contacting your local home loan expert, you’ll need to complete the Property and Security Request Form before you sell your current property so that a term deposit can be set-up, as temporary security for the loan. Provide details of:

1. The representative or home loan expert that you’ve spoken to

2. Your current property including settlement date

3. Ensure you request to keep your loan open

4. Under Additional information please type Application for portability.

We’ll then be in touch with next steps.

Frequently asked questions

The general rule for portability is like-for-like substitution, which basically means switching the property being held as the mortgage security on the home loan with a property of equal or greater value. A valuation may be required for the new property.

To find out if you can port your loan, contact your local home loan expert before completing the Property and Security Request Form. If ineligible, you’ll have the option to start a new home loan application.

Most standard home loans are eligible provided your new property meets our security and lending criteria.

Portability is not available for the following scenarios:

- Using commercial security as substitute

- Existing loans taken out by non-residents

- Sustainable Upgrades Home Loans or Sustainable Upgrades Investment Loans

- Home Loans that fall under the Australian Government 5% Deposit Scheme.

- Loans with a delinquency history

- Loans where a settlement or limit increase is pending (which must be completed first)

- Existing bridging loans.

To find out if your loan is eligible, contact your local home loan expert before completing the Property and Security Request Form.

You can still port your loan, but you’ll need to apply and finalise any loan increases first.

No. The term deposit has been set up purely to secure the existing mortgage until you purchase the new property. The amount held in the term deposit as security matches the home loan limit. Throughout the process, you’ll need to keep paying your home loan repayments as normal.

You can still port your current home loan, but you’ll need to apply for a new bridging loan to cover the new home purchase until you sell your property. Once you have sold your property, we’ll close the bridging loan and then substitute the new property as the mortgage security for your current home loan.

To discuss portability before applying, you may need to speak to your local home lender. To contact your local home loan expert:

1. Enter your postcode in the Find a lender search feature below

2. Select Go to all results

3. Then select Experts to find their contact details.

Or you can visit your local branch.

Things you should know

Conditions, credit criteria, fees and charges apply. Residential lending is not available for Non-Australian Resident borrowers.

This information is general in nature and has been prepared without taking your personal objectives, circumstances and needs into account. You should consider the appropriateness of the information to your own circumstances and, if necessary, seek appropriate professional advice.

Any tax information described is general in nature and it is not tax advice or a guide to tax laws. We recommend you seek independent, professional tax advice applicable to your personal circumstances.

Credit provided by Westpac Banking Corporation ABN 33 007 457 141 AFSL and Australian credit licence 233714.