How to calculate rental yield

.jpg)

If you’re considering investing in a property, it’s a good idea to understand the rental yield when trying to figure out the returns you might expect from your investment. Understanding rental yield can help you work out which properties and suburbs might be worth investing in. Let’s explore what rental yield is, how to calculate it, what classifies a ‘good’ rental yield, as well as other important things to consider.

Rental yield is simply the difference between the income you receive from renting out your property minus the overall costs of your investment. It’s often expressed as a percentage and the higher the percentage generally means greater cash flow and higher return on investment.

There are two different types of rental yield – gross rental yield and net rental yield – and both are calculated differently, providing (sometimes substantially) different figures.

Gross rental yield is a simpler calculation that looks at the amount of rental income you can receive over a year, measured against the market value of the property. While gross rental yield can be useful for determining a property’s general investment potential, it may not give you a completely realistic idea of your outgoings.

The net rental yield will give you a more accurate figure as it factors in the ongoing expenses of your investment property, which in some instances can be considerable. Expenses can include insurance, strata fees, repair costs and legal fees, to name a few.

Regardless of whether you’re calculating the gross or net figures, understanding rental yield is important for property investors as it can help determine what the ongoing return may be on your potential investment and whether it will work with your overall investment goals. Keeping track of your rental yield can also be beneficial for annual rental reviews on your property.

If you have questions about the different ways you can access equity and take out a new loan, our home loan specialists are here to help. Call us on 132 558 or visit a branch.

Gross rental yield and net rental yield are both calculated differently and can paint a different picture of an investment property.

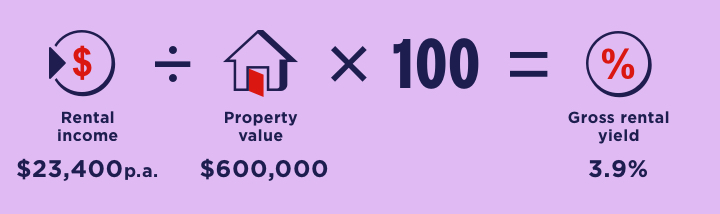

Calculating gross rental yield is less complicated. Simply take the weekly/monthly rent to work out the annual rental income, then divide it by the property’s purchase cost and multiply it by 100, so you get a percentage.

Gross rental yield example:

The gross rental yield is 3.9%

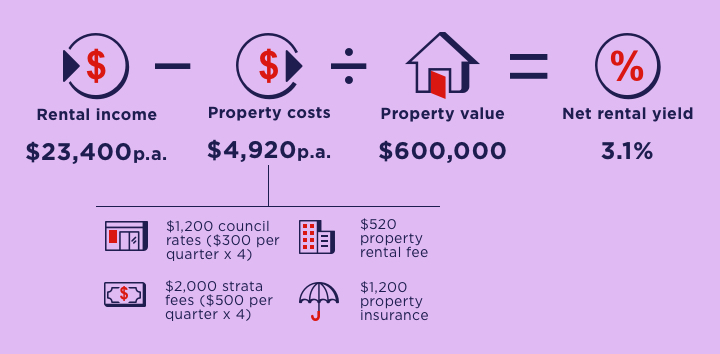

Calculating the net rental yield on a property is more technical and factors in expenses, providing a more realistic figure of a property’s rental return. When calculating the net rental yield, it’s a good idea to factor in:

To calculate the net rental yield, you take the same formula as the gross rental yield, minus your anticipated expenses. We’ll show you the exact calculation below.

Net rental yield example:

The net rental yield is 3.1%

There’s no clear-cut answer on what constitutes a good rental yield – it seems obvious that a higher yield would be better, offering a stronger cash flow. But a high rental yield may come at the cost of lower or slower capital growth potential.

An investment property which has a high rental yield (generally between 8-10%) may mean that it's undervalued. However, a property that returns a low rental yield (between 2-4%) could suggest that it's overvalued.

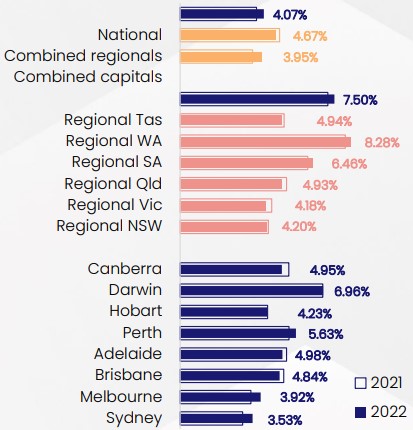

According to CoreLogic, Darwin has experienced the highest gross rental yield for units among the capital cities: 6.96% during the 12 months to Aug 2022, with Perth, Adelaide and Canberra all above 4.9%, and Sydney recording the lowest at 3.53%*.

Overall, Australia’s capital cities generally performed better than regional areas. Regional Western Australia and Regional SA were the leaders in the regions, with rental yields of 8.28% and 6.46% respectively over the last 12 months. Regional Victoria saw the lowest average rental yield at 4.18%*.

As with most things, it comes down to your investment strategy. A property with high rental yield might provide you with steady cash flow but may not have the best capital growth potential. Conversely, while a property with low rental yield might not give you as big a profit or cash flow as you had hoped, it may offer superior capital growth due to being in a popular area or area set for growth.

It’s the million-dollar question that every property investor wants to know - where are the properties with the highest rental yield? Thankfully, there’s free online tools, like our Property Market Research tool, that can help investors understand the latest data on suburbs and properties around the country. Information about expected rental income, rental yield, as well as suburb price trends and demographics all go a long way towards helping you find that perfect investment property.

Gross Rental Yield 12-month average across Australia

Source: CoreLogic unit gross rental yield – 2021 vs 2022 (as of end of August 2022)

As with any investment, there’s a few things to be mindful of when it comes to rental yield. When looking at an investment property, to ensure you will be able to cover all costs, it can be a good idea to work out the net rental yield so you have a more realistic understanding of what your returns might be.

While a property may have a high price point, this doesn’t necessarily translate to achieving a high rental income. In fact, many investors who invest in high-price point properties have a low rental yield, and do not receive enough rental income to cover their costs. This is called negative gearing – which you may have heard of. But why would you do this?

While negative gearing sounds potentially problematic from an investment point of view, there maybe a silver lining. In some circumstances, if your property expenses are higher than the rental income you receive, you may be able to use this loss to reduce your overall taxable income. This could lower the amount of tax you pay, depending on government tax laws and whether you meet the eligibility criteria.

Negative gearing can be more suitable for investors who aren’t reliant on the additional cash flow and are more focused on capital growth potential of their property. For those looking to supplement their regular income with rental income and a positive cash flow (such as retirees), positive gearing may be more attractive, by choosing properties with a high rental yield.

Reach out to your tax adviser for advice.

With the opportunity to grow your wealth, property can be an attractive investment. There are few things to consider however, and that’s where we come in. For more information on how to start your property investment journey, call us on 132 558 or visit a branch to chat to your local Home Finance Manager.

Capital growth is an important factor when it comes to purchasing property or reviewing your investment options.

Whether it’s your first time, or you’re a seasoned property investor, we can provide insights and information that could help you make your decision.

This information is general in nature and has been prepared without taking your personal objectives, circumstances and needs into account. You should consider the appropriateness of the information to your own circumstances and, if necessary, seek appropriate professional advice. Credit provided by Westpac Banking Corporation ABN 33 007 457 141 AFSL and Australian credit licence 233714.