Budget smarter, not harder

We've taken the hard work out of budgeting. See your available cash at a glance, stay organised, or save for something special with our budget planning tool.

See your cash in a flash

Simplify budget planning

No more scrolling through bank statements for the ins and outs of your spending. Our Budget Planner does it for you by analysing past transactions.

Fine tune your spending

Curious where your money goes? Set limits on spend categories to see exactly how much money you spend on food and other monthly expenses.

Plan your saving

Set different savings goals for each budget cycle, so when an expensive week or unexpected cost comes up, you can budget accordingly.

How to set up Budget Planner

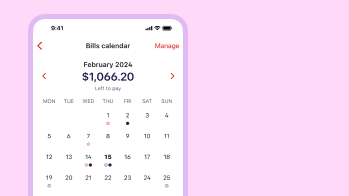

1. Set up Bills Calendar

Search Bills Calendar in the Smart Search bar on your home screen to get started. Follow the prompts to add the bills that will feed into your budget.

2. Start your budget

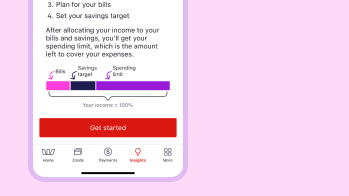

Search Budget or tap Insights at the bottom of your home screen and then tap My Budget to begin.

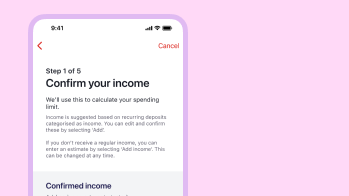

Follow the prompts to confirm your income and set your budget cycle.

3. Sort your bills and savings

Budget Planner automatically includes bills you already have in Bills Calendar. You can opt to exclude them and add in any extras during setup. Once you've confirmed your outgoings, set an optional savings target to track your big expenses.

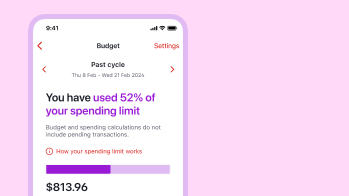

4. Review and manage

Now you can see your spending limit for your chosen budget cycle. Remember to pick which accounts to include and set alerts to remind you when that cycle is over and a new one begins.

What else can I use the Budget Planner for?

1. Future planning

Take a look at your previous budget cycles by navigating back in the Budget Planner so you can compare your spending, set goals and plan for the future.

2. Setting limits

Track your spending in different areas by viewing categories. You can add limits to each category by tapping Add limit and choosing your amount.

3. Staying up-to-date

If you need to change your income, bills or savings targets, tap Settings at the top of your screen and edit the numbers. Your budget will automatically update.

Let's help you get started

To enjoy Budget Planner, Bills Calendar and other Westpac App features, you need to be a Westpac customer

Personalised Insights, right where you need them

Get tips and alerts that help you spot trends, avoid surprises and stay in control of your money. You’ll find them on your Westpac App home screen or in the Insights tab. The more you use our money tools, the smarter and more personalised your insights become.

Ways to budget

Check out our App features

Whether you need to split expenses, organise your bills or save, we’ve got the tools for you.

Frequently asked questions

Your spending limit will automatically change when you update your income or savings targets under Budget settings. Adding or removing bills in your Bills Calendar will also affect your spending limit from cycle to cycle.

Yes, you can edit a category limit and you’ll be asked if you want to change the limit for that cycle or future cycles also.

To get a clear view of your budget it’s good to include all account transactions that impact your spending. All eligible accounts are included by default, but you can remove ones that are not relevant to your budget so they won't appear in your Budget Planner.

Your bills are already included in your Bills Calendar total so to avoid being double counted, they won’t appear in your amount spent and your category spending.

Tapping the arrows on either side of the current cycle header allows you to go back to past cycles and forward to future cycles for up to a year. If you have your bills set up in your calendar, you'll be able to navigate forward and see how these bills impact the amount you'll have left to spend in those cycles.

Things you should know

Read the Westpac Online Banking Terms and Conditions (PDF 619KB) at westpac.com.au before making a decision and consider whether the product is right for you.

iPhone, iPad, iPod touch and Apple Watch are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a Service mark of Apple Inc.

Android, Google Play and the Google Play logo are trademarks of Google LLC.