FX BEAT: Westpac’s Callow on the A$ outlook for 2024

Japan is an increasingly popular destination for Australian tourists, with the weakness of the yen meaning it offers good value for money. (Getty)

Japan has been among the top destinations for Australian tourists over the holiday season and the weak yen has played no small part in that.

Aussies are finding that their dollars give them good value in a country whose attractions range from world-class skiing to vibrant cities, great food and child-friendly theme parks.

“The world has been fighting a post-pandemic surge in inflation, but in contrast the Bank of Japan is still not convinced that inflation is on track to rise sustainably to its 2 per cent target,” says Westpac senior currency strategist Sean Callow in a podcast interview. As a result, the central bank is keeping interest rates ultra-low, which in turn makes the yen unattractive to foreign investors.

“The yen has been trading around the 97-98 per Aussie dollar area and Australian visitors are finding that buys them quite a bit of holiday enjoyment in Japan,” Callow adds.

There’s little in the economic outlook to suggest that the yen will strengthen appreciably in the medium-term, Callow says, which is good news for Japan’s booming tourism industry.

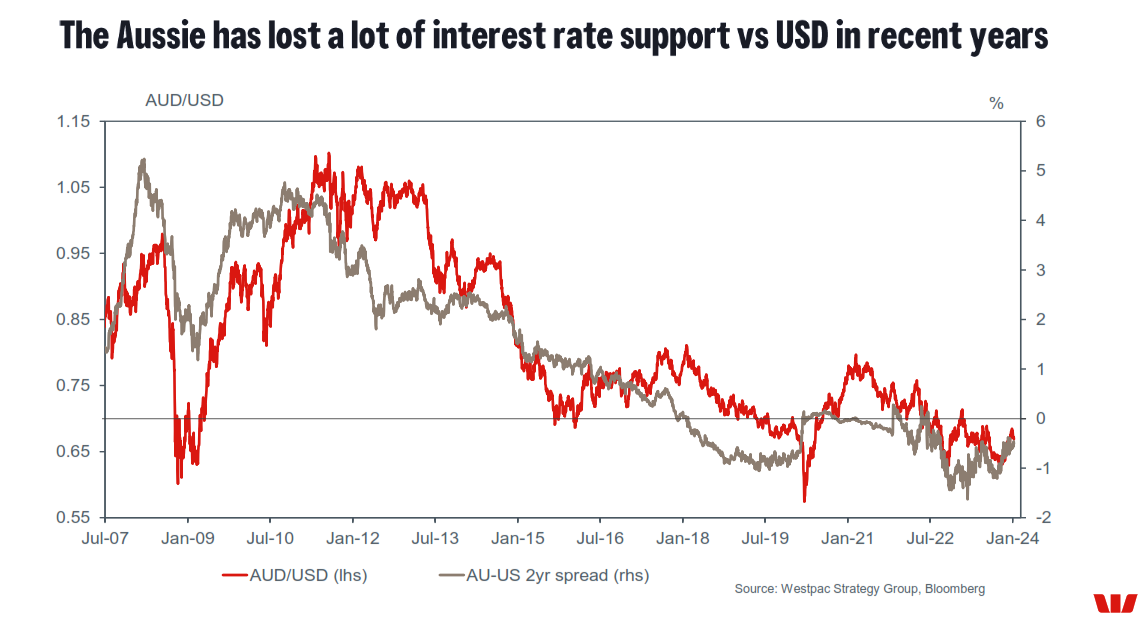

The broader outlook for the Australian dollar in the year ahead is more mixed. The Aussie trended weaker overall in 2023, averaging around 66 cents against the U.S. dollar compared to over 69 cents in 2022.

The primary market driver was interest rate differentials, with the U.S. benchmark fed funds rate settling at 5.50 per cent – a healthy premium to the Reserve Bank of Australia cash rate at 4.35 per cent. Focus in the year ahead will switch to the timing of rate cuts in both countries.

Some of the wind was taken out of the U.S. dollar’s sails in December after Federal Reserve Chairman Jay Powell revealed there had been a discussion about rate cuts at the Fed’s latest policy meeting. However, data since the start of this year has shown the U.S. economy continues to perform well, giving Powell little room for manoeuvre.

“Job creation is still pretty swift - the unemployment rate is below 4 per cent and while inflation is coming down it's still well above the 2 per cent target,” Callow notes. As a result, U.S. bond yields and the greenback have pushed higher again in early 2024.

The Fed policy meeting in March could be a pivotal event, Callow says, with markets currently pricing in around a 50:50 chance of a rate cut.

Australia’s central bank is likely to keep rates on hold in the first half of this year, with Westpac economists forecasting 50 basis points worth of RBA cuts in the second half as inflationary pressures ease.

“Compared to some other central banks that’s more modest, so it probably helps the Aussie dollar a little bit,” says Callow.

Markets are pricing in at least 140 basis points worth of easing from the European Central Bank this year, to help support a Eurozone economy that is teetering on the brink of a shallow recession, Callow says. The UK economy is performing slightly better, although around 100 basis points of rate cuts are still in prospect this year from the Bank of England.

“In terms of those trends, it does look as though the Aussie will probably hold up a bit better against the euro but remain on the weak side against the pound,” Callow says. Sticky inflation has seen the BoE hold its benchmark rate at a relatively high 5.25 per cent, comfortably above the RBA cash rate.

Another driving force behind A$ moves is the economic performance of China – Australia’s most important trading partner.

A Hong Kong court decision in January ordering Evergrande Group, one of China’s biggest property developers, to liquidate its assets has cast a cloud over the country’s growth prospects.

“There’s a lot of concern about China’s financial sector. The property market has been under stress for a number of years,” Callow says. Meanwhile, the Chinese stock market fell to five-year lows in January, even as U.S. stocks were hitting record highs.

That’s triggered concern among policymakers, with the authorities indicating that they’re willing to step in with measures to support the market.

“We're pretty upbeat in terms of overall growth for the Chinese economy, but the question is whether investors share that optimism,” Callow says. Another risk factor is a potential deterioration in U.S.-China trade relations, as U.S. presidential candidates vie to take the toughest stance on China heading into an election later this year.

In terms of overseas destinations, New Zealand could be another place where Aussies find their dollar goes a bit further this year. That’s despite New Zealand interest rates currently sitting well above the RBA cash rate at 5.50 per cent.

“The Aussie does have other factors that are very supportive,” Callow notes. Australia’s large trade surplus, swelled by bumper earnings in the mining industry, contrasts with a trade deficit in New Zealand, while the fiscal position is also stronger.

Westpac economists see sluggish GDP growth of 0.3 per cent for New Zealand over 2024, compared with 1.6 per cent for Australia.

Don't miss

Related articles

Currency markets are choppier in 2026 - and businesses are feeling it

By Haydn Calderwood

Managing Director, Business and Consumer Group