MONEY TALK: Stamp duty, stamped out?

Westpac tax expert Chris Plakias takes a look at the proposal to change how property is taxed in NSW. (Getty)

It’s not something that happens very often, if at all, but the New South Wales government is considering a proposal that will cost it billions of dollars.

It has even put a price on it – $11 billion in the first four years alone.

Intrigued? Read on.

The proposal – which is still going through consultation – is a change to the way in which property is taxed in NSW.

Currently, when you buy a property, you need to pay stamp duty – sometimes called transfer duty – and the amount is around 4 per cent of the property’s sale price. So, if you pay $1.2 million for a Sydney abode (the average house price) you’ll fork out around another $50,000 in stamp duty.

But if the proposed changes go ahead, most NSW property buyers would be given a choice – either stick with paying the big upfront cost of stamp duty, or pay a lower annual property tax instead.

The new tax – which would replace land tax, where applicable (generally on properties you own other than your principal place of residence) – would be calculated on what is known as the “unimproved land value”, in other words the value of the land alone without the buildings on it. This is similar to how council rates are set.

Initially, it would apply to 80 per cent of properties, with the top 20 per cent of the market by value (the most expensive properties) still subject to stamp duty. But this could change over time.

And although the government has made it clear that buyers will be given the choice of paying stamp duty or the annual property tax, once a property is subject to the annual property tax it will always be so: all subsequent owners would need to pay the annual property tax.

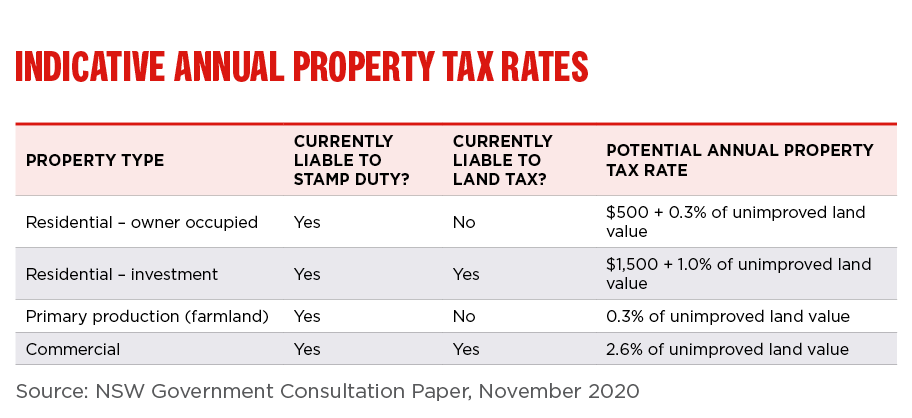

The government has provided an indication of the property tax rates that would apply, although these may well change:

Based on these rates, if you bought and lived in a home on land valued at $630,400 (the average in metropolitan NSW), your annual property tax would be $2391.

So, while there are a lot of variables at play, a simplistic calculation would indicate that if you buy a property in Sydney around the average price, you’d be paying an annual property tax for around 20 years before you reach the equivalent of the upfront stamp duty. For those intending to hold onto property for longer than that, paying stamp duty may still be an attractive option.

Even so, the government is banking on a short term hit to revenue as many people pick the annual tax option – that bit about the reform costing $11bn. However, despite this initial hit to its coffers, over time the government expects that revenue from the annual property tax option will match the forgone stamp duty and be self-funded in the long term.

The spark for this proposed change is that stamp duty – first introduced in NSW in 1865 when house prices were lower and moving homes was rare – is no longer fit for the current generation of home buyers.

It will be no surprise to today’s home buyers that plenty of independent reviews have found that having such a big upfront cost creates a barrier to owning a home.

As the government rightly points out, it’s removal could boost home ownership and introduce more flexibility into the property market, meaning more people would be able to move house more often, adapting their living arrangements around lifestyle decisions or changes to work and family circumstances.

Other economic benefits are also likely to flow, such as increased spending on renovations and home furnishings and spill-over benefits to relevant service industries such as real estate agents, accountants and conveyancers.

But as with any significant tax reform, the proposed change has pros and cons, and still plenty of unknowns and challenges to work through.

For example, when a borrower applies for a home loan, it’s likely they will not know whether they will purchase a property already subject to the annual property tax or, if not, which tax choice they will make – potentially impacting their borrowing power.

Others may wrestle with whether an ongoing annual tax will in fact be more financially beneficial in the long term than a one-off duty.

As the government works its way through these challenges, and releases more modelling about rates and thresholds, there’s no doubt other Australian states will be keenly watching.

The Australian Capital Territory is the only Australian jurisdiction to have moved towards abolishing stamp duty in a staged process started by the ACT government in 2012, and pressure is mounting on other states to follow suit as part of efforts to stimulate COVID-affected economies. In November, the Victorian government announced temporary stamp duty relief measures, but the jury is out about whether it will follow the NSW lead.

And as house prices continue to surge, those in the market will keep a keen eye on the outcome too.

The views expressed are those of the author and do not necessarily reflect those of the Westpac Group. The information in this article is general information only, it does not constitute any recommendation or advice; it has been prepared without taking into account your personal objectives, financial situation or needs and you should consider its appropriateness with regard to these factors before acting on it. Any taxation position described is a general statement and should only be used as a guide. It does not constitute tax advice and is based on current tax laws and our interpretation. Your individual situation may differ and you should seek independent professional tax advice. You should also consider obtaining personalised advice from a professional financial adviser before making any financial decisions in relation to the matters discussed.