Rate cuts. Housing inequality. Deleveraging. Access to credit. Trade concerns.

Sounds like debates raging in Australia. But these issues are also key to the outlook for China. And there’s undoubtedly worrying signs and risks.

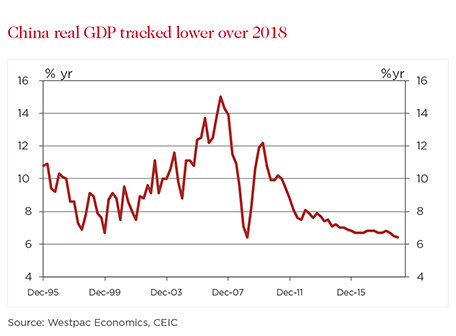

In late 2018, annual growth in China decelerated to a rate reminiscent of the GFC low of March 2009. Unsurprisingly, financial markets are concerned about the economy’s prospects in 2019 and beyond amid trade tensions and slowing global growth.

But it’s important to note that while a broad-based slowdown from deteriorating export demand across manufacturing and – to a lesser extent – services is evident, the key determinant of China’s softer growth has actually been structural change – planned and managed by China’s central government.

Put simply, in pursuit of long–term financial stability and sustainable growth, China’s economic authorities in the past few years focused on the quality of growth, particularly its longevity, environmental impact and reducing wealth inequality.

Given this is at the core of the slowdown, we aren’t as bearish as some observers about the outlook, anticipating GDP growth will be sustained around 6 per cent.

Amid much discussion about “trade wars” and tariffs, it’s worth remembering that the US only receives about 20 per cent of China’s total exports. Put another way, China has considerable scope to grow total goods exports even if US/China trade tensions persist. And the stronger these regional trade linkages become, the greater China’s opportunity to benefit from the export of services as well, particularly education, tourism and business services.

The massive “Belt and Road” initiative will further stimulate these linkages and provide opportunities to diversify China’s export base. Fostering greater education attainment and entrepreneurialism to make ready the workforce for the opportunities to come will be important.

It may surprise some people, but China has developed to the point where it can offshore low-value production to neighbouring countries where wages are lower, bolstering the drive for regional integration. The additional benefit is three-fold: lower production costs maximise the profit that flows back to Chinese investors; production abroad offers firms an opportunity to skirt US tariffs which only apply to exports from China; while capacity is created domestically to develop new industry, which will generate higher income.

These trends have been clearly evident in the investment detail.

The central government’s push for investment decisions to be judged on economic worth saw growth in fixed asset investment across the economy slow to a historically weak annual pace in 2018 of 5.9 per cent, as investment by state-owned enterprises (SOEs) effectively stalled at 1.9 per cent. All of a sudden, historically-troublesome forms of investment, such as poorly-planned infrastructure investment by local government authorities, was sharply curtailed.

But with this one-off initial re-orientation of the economy towards quality having been achieved and overall GDP growth having slowed, authorities are increasingly acting to boost momentum and new investment.

This is happening on two fronts.

First, local government authorities are being encouraged to accelerate their infrastructure plans. But these projects are slated to be funded by new bond issuance – in effect seeing investors act as a check on the quality of investment.

Secondly, the availability of funding to the banking system is being increased materially and its cost reduced, resulting in flow-on benefit to end borrowers. Banks are being encouraged to focus on up-and-coming industries, where there is maximum long-term benefit for China, while loan availability for established businesses and the household sector is also being supported.

China Telecom employees install a 5G base station at a branch office in Lanzhou, Gansu Province of China. (Getty)

However, with risks elevated in the near-term, authorities will likely continue to promote private sector investment. Expected softer growth in consumption – the biggest driver of growth in 2018 – will also need to be closely watched as the effect of US/China trade tensions come to bear on employment and income. As seen in Australia’s February corporate results season, some companies with China operations, such as Blackmores, noted softer consumer sentiment.

But from 2020 and beyond, market forces should increasingly take over as the driver and assessor of investment projects. Increased economic and political engagement within Asia should only help to drive successive waves of investment on and offshore over the coming decade.

New investment and industries should lead to income and wealth gains for Chinese households, providing a strong foundation for increased spending and personal investment. This sets the scene for robust aggregate growth over the coming decade, spread across retail, residential construction and financial assets.

What will be important though is that the gains in income and activity are well spread across the nation, down and up the income spectrum. If this is not the case, then household demand may disappoint as the wealthy accumulate assets rather than spend. Like in Australia, housing remains households’ primary asset, but to preserve affordability and opportunity, house price growth needs to spread across the tiers and be aligned to income growth or risk investors profiting from households down the income spectrum.

Beyond the near-term risks related to trade and expected more modest pace of headline GDP growth, the opportunities from China’s continued development remain plentiful for Australia.

Demand for commodity exports, which represent more than 50 per cent of our total exports to China, is likely to remain strong.

Iron ore collects in a stockpile at Fortescue Metals Group's Solomon Hub mining operations in Western Australia’s Pilbara region. (Getty)

Despite trade tensions, the iron ore price is trading around $US90 a tonne, a multi-year high, following the tragic tailings dam incident in Brazil that resulted in supply disruptions. While prices may fall, China’s continued investment in infrastructure and housing will foster ongoing demand for Australia’s key commodity exports of iron ore and coal, particularly given our position as a low-cost, high-quality producer.

The services sector, which already represents almost a quarter of our total exports, also presents further opportunities. As the incomes and wealth of Chinese households grow robustly in the years ahead, education and tourism in Australia holds great promise. Education, for example, can create deep relationships that further develop the links with China and hence the opportunity to grow business services.

Like in Australia, risks are varied and elevated in China. Given Australia’s high exposure to conditions, nerves are understandably being tested amid heightened global volatility and uncertainty.

But longer term, China may very well manage its economic slowdown and transition better than the doubters and doomsayers expect.

Frances Cheung, Westpac’s head of macro strategy, Asia, contributed to this article.

This material contains general commentary, and market colour. This material does not constitute investment advice. This information has been prepared without taking account of your objectives, financial situation or needs. We recommend that you seek your own independent legal or financial advice before proceeding with any investment decision. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The ultimate outcomes may differ substantially from these forecasts. Except where contrary to law, Westpac and its related entities intend by this notice to exclude liability for this information.

After four years with the Reserve Bank of Australia, Elliot joined Westpac in 2010. His background includes analysing economic developments in East Asia, and Australia’s foreign assets and liabilities. Elliot’s current responsibilities include developing Westpac’s structural view for the US and Europe, plus providing a macro-financial perspective on the Australian economy.

{"topicSelector":[{"tagId":"newsroom:topics/economy","name":"economy","description":"Explore more Economy insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Economy","url":"/news/topic.economy/"},{"tagId":"newsroom:topics/banking","name":"banking","description":"Explore more Banking insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Banking","url":"/news/topic.banking/"},{"tagId":"newsroom:topics/digital","name":"digital","description":"Explore more Digital insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Digital","url":"/news/topic.digital/"},{"tagId":"newsroom:topics/diversity","name":"diversity","description":"Explore more Diversity insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Diversity","url":"/news/topic.diversity/"},{"tagId":"newsroom:topics/community","name":"community","description":"Explore more community insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Community","url":"/news/topic.community/"},{"tagId":"newsroom:topics/workplace","name":"workplace","description":"Explore more workplace insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Workplace","url":"/news/topic.workplace/"},{"tagId":"newsroom:topics/sustainability","name":"sustainability","description":"Explore more sustainability insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Sustainability","url":"/news/topic.sustainability/"},{"tagId":"newsroom:topics/technology","name":"technology","description":"Explore more Technology insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Technology","url":"/news/topic.technology/"},{"tagId":"newsroom:topics/property","name":"property","description":"Explore more Property insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Property","url":"/news/topic.property/"},{"tagId":"newsroom:topics/westpac","name":"westpac","description":"Stories featuring Westpac corporate news.","title":"Westpac","url":"/news/topic.westpac/"},{"tagId":"newsroom:topics/sme","name":"sme","description":"Explore more Small Medium Enterprise insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"SME","url":"/news/topic.sme/"},{"tagId":"newsroom:topics/innovators","name":"innovators","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Innovators","url":"/news/topic.innovators/"},{"tagId":"newsroom:topics/leadership","name":"leadership","description":"Explore more Leadership insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Leadership","url":"/news/topic.leadership/"},{"tagId":"newsroom:topics/covid19","name":"covid19","description":"Stories influenced by the COVID-19 pandemic.","title":"COVID-19","url":"/news/topic.covid19/"},{"tagId":"newsroom:topics/investing","name":"investing","description":"Explore more Innovators insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Investing","url":"/news/topic.investing/"},{"tagId":"newsroom:topics/startups","name":"startups","description":"Explore more Startups insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Startups","url":"/news/topic.startups/"},{"tagId":"newsroom:topics/personalfinance","name":"personalfinance","description":"Explore more insights about personal finance, financial literacy and financial wellbeing. ","title":"Personal finance","url":"/news/topic.personalfinance/"},{"tagId":"newsroom:topics/agribusiness","name":"agribusiness","description":"Explore more Agribusiness insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Agribusiness","url":"/news/topic.agribusiness/"},{"tagId":"newsroom:topics/scams","name":"scams","description":"Stories about the latest cyber scams news and trends. ","title":"Scams","url":"/news/topic.scams/"},{"tagId":"newsroom:topics/billsbites","name":"billsbites","description":"Explore more insights from Bill Evans at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Bill\u0027s Bites","url":"/news/topic.billsbites/"},{"tagId":"newsroom:topics/data","name":"data","description":"Explore more data insights at Westpac Wire.","title":"Data","url":"/news/topic.data/"},{"tagId":"newsroom:topics/environment","name":"environment","description":"Explore more Environment insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Environment","url":"/news/topic.environment/"},{"tagId":"newsroom:topics/payments","name":"payments","description":"Explore more Payments insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Payments","url":"/news/topic.payments/"},{"tagId":"newsroom:topics/fintech","name":"fintech","description":"Explore more Fintech insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Fintech","url":"/news/topic.fintech/"},{"tagId":"newsroom:topics/politics","name":"politics","description":"Explore more Politics insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Politics","url":"/news/topic.politics/"},{"tagId":"newsroom:topics/career","name":"career","description":"Stories providing career insights, tips and trends.","title":"Career","url":"/news/topic.career/"},{"tagId":"newsroom:topics/social-enterprise","name":"social-enterprise","description":"Stories relevant to or featuring social enterprises.","title":"Social enterprise","url":"/news/topic.social-enterprise/"},{"tagId":"newsroom:topics/indigenous","name":"indigenous","description":"Explore more indigenous insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Indigenous","url":"/news/topic.indigenous/"},{"tagId":"newsroom:topics/regulation","name":"regulation","description":"Explore more Regulation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Regulation","url":"/news/topic.regulation/"},{"tagId":"newsroom:topics/wellbeing","name":"wellbeing","description":"Stories featuring wellbeing trends, insights and stories.","title":"Wellbeing","url":"/news/topic.wellbeing/"},{"tagId":"newsroom:topics/superannuation","name":"superannuation","description":"Explore more Superannuation insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Superannuation","url":"/news/topic.superannuation/"},{"tagId":"newsroom:topics/westpac-scholars","name":"westpac-scholars","description":"Stories featuring Westpac Scholars. ","title":"Westpac Scholars","url":"/news/topic.westpac-scholars/"},{"tagId":"newsroom:topics/reinventure","name":"reinventure","description":"Explore more Reinventure insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Reinventure","url":"/news/topic.reinventure/"},{"tagId":"newsroom:topics/asia","name":"asia","description":"Explore more Asia insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Asia","url":"/news/topic.asia/"},{"tagId":"newsroom:topics/podcast","name":"podcast","description":"Explore Westpac Wire\u0027s podcast series.","title":"Podcast","url":"/news/topic.podcast/"},{"tagId":"newsroom:topics/history","name":"history","description":"Stories unearthed from Westpac\u0027s private archival collection. ","title":"History","url":"/news/topic.history/"},{"tagId":"newsroom:topics/businesses-of-tomorrow","name":"businesses-of-tomorrow","description":"Stories featuring Westpac Businesses of Tomorrow program winners. ","title":"Westpac Businesses of Tomorrow","url":"/news/topic.businesses-of-tomorrow/"},{"tagId":"newsroom:topics/tax","name":"tax","description":"Explore more tax insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Tax","url":"/news/topic.tax/"},{"tagId":"newsroom:topics/luciscall","name":"luciscall","description":"Explore more insights from Westpac\u0027s chief economist Luci Ellis at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Luci\u0027s Call","url":"/news/topic.luciscall/"},{"tagId":"newsroom:topics/goodpair","name":"goodpair","description":"Explore more Good Pair stories, showing two people making a big difference together. ","title":"Good Pair","url":"/news/topic.goodpair/"},{"tagId":"newsroom:topics/opinion","name":"opinion","description":"Expert opinions and insights. ","title":"Opinion","url":"/news/topic.opinion/"},{"tagId":"newsroom:topics/currencies","name":"currencies","description":"Stories providing currencies insights, tips and trends.","title":"Currencies","url":"/news/topic.currencies/"},{"tagId":"newsroom:topics/deals","name":"deals","description":"Explore more Deals insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Deals","url":"/news/topic.deals/"},{"tagId":"newsroom:topics/veterans","name":"veterans","description":"Explore more insights about defence force veterans at Westpac Wire.","title":"Veterans","url":"/news/topic.veterans/"},{"tagId":"newsroom:topics/analysis","name":"analysis","description":"Expert analysis on economic news and other trends.","title":"Analysis","url":"/news/topic.analysis/"},{"tagId":"newsroom:topics/IWD","name":"IWD","description":"Stories focusing on International Women\u0027s Day, on 8 March annually. ","title":"IWD ","url":"/news/topic.IWD/"},{"tagId":"newsroom:topics/rework","name":"rework","description":"Stories of businesses pivoting in the face of the COVID-19 pandemic.","title":"Rework","url":"/news/topic.rework/"},{"tagId":"newsroom:topics/10Qs","name":"10Qs","description":"\"10Qs with...\" is a series that asks leaders what makes them tick.","title":"10Qs","url":"/news/topic.10Qs/"},{"tagId":"newsroom:topics/commodities","name":"commodities","description":"Insights into commodities markets.","title":"Commodities","url":"/news/topic.commodities/"},{"tagId":"newsroom:topics/quarterlife","name":"quarterlife","description":"Explore more Quarter Life insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Quarter Life","url":"/news/topic.quarterlife/"},{"tagId":"newsroom:topics/shareholders","name":"shareholders","description":"Stories relevant to Westpac shareholders.","title":"Shareholders","url":"/news/topic.shareholders/"},{"tagId":"newsroom:topics/climate","name":"climate","description":"Explore more climate insights at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"Climate ","url":"/news/topic.climate/"},{"tagId":"newsroom:topics/esg","name":"esg","description":"Explore more insights on environmental, social and governance issues at Westpac Wire. Subscribe to the Westpac Wire newsletter to stay in the know.","title":"ESG","url":"/news/topic.esg/"},{"tagId":"newsroom:topics/boardwalk","name":"boardwalk","description":"A series of in-depth podcast interviews with board directors to find out what\u0027s on their minds. ","title":"Board Walk","url":"/news/topic.boardwalk/"}]}