Construction Option Loans

Construction Option Loans (or Building Loans) could help your clients save while building or renovating their home.

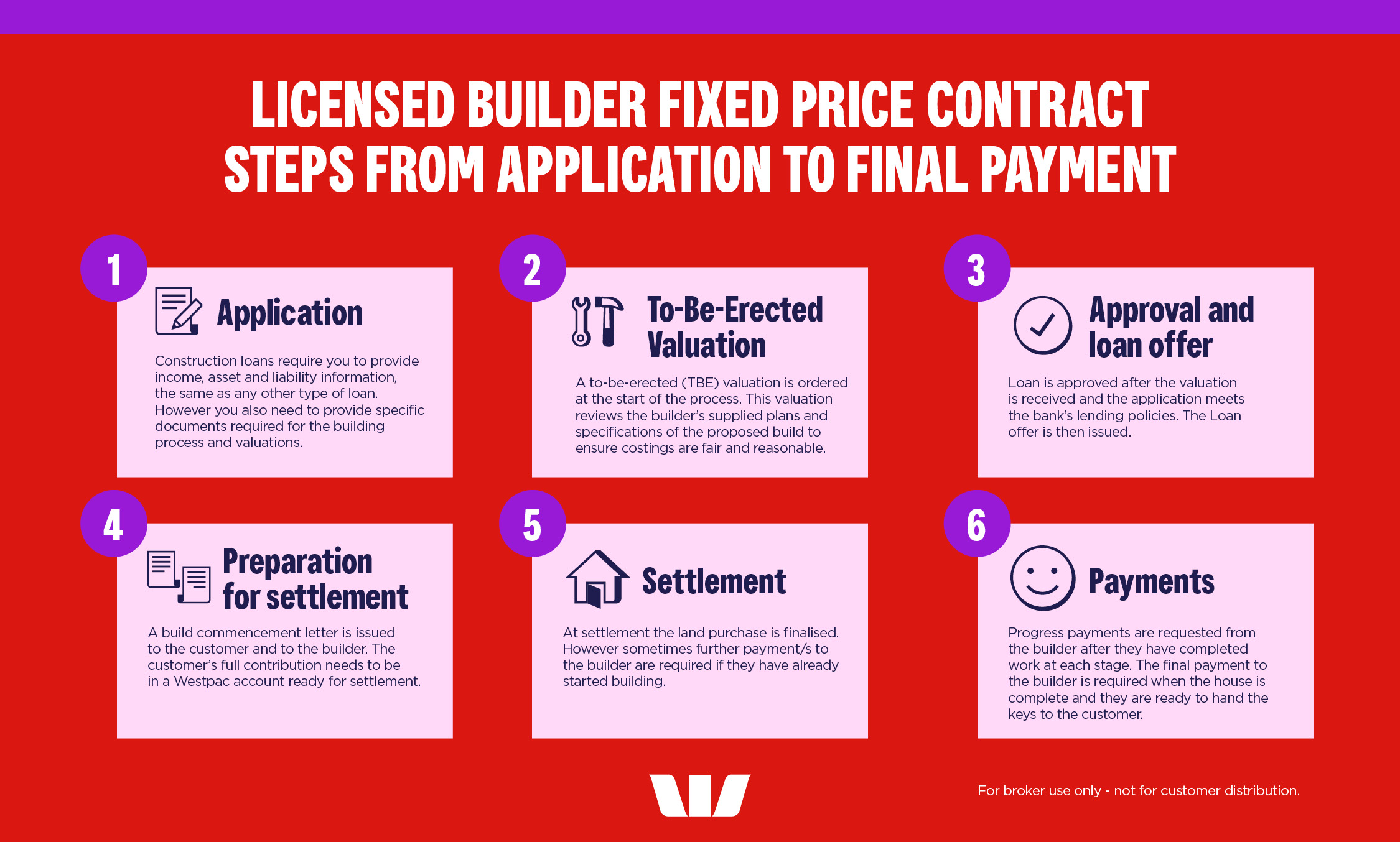

Download this helpful infographic on Construction Loan applications.

Licensed Builder Fixed Price Contract: Steps from Application to Final Payment

1. Application

- Existing lending standards apply

- For single land and build applications, your client’s full contribution is required at settlement

- For separate land and build applications with lengthy delays to build, an Approval in Principle (AIP) for the build should be completed

- Where First Home Owner Grant (FHOG) is being used, arrange for documents to be sent in with the application

2. To-Be-Erected Valuation

- Correct entry into ApplyOnline will ensure a To-Be-Erected valuation is ordered

- Ensure the valuer has all the information required for the valuation by uploading to Valex

3. Approval and Loan Offer

- Review valuation to ensure payment schedule is to industry standard

- Review whether the valuation requires a Quantity Surveyor Report. Please note that a QSR may be required at each progress inspection

- Review risk ratings which require referral to PACE

- Loan Offer is sent once the loan is approved

4. Preparation for Settlement

- Ensure your client has deposited their FULL contribution into a Westpac account ready for settlement

- Return your client’s signed verbal payment authority to allow for phone requests of payments

5. Settlement

- Operations Team manages the land settlement, and the loan then migrates to the payments team post settlement

- If a payment is required to the builder as part of settlement, it will be made to the builder at settlement

6. Payments

- Payments are paid to the builder or reimbursed to your client for amount already paid

- Progress Inspections are required at certain stages and are completed by the valuer

Resources and tips for your client.

Building or renovating can be an overwhelming experience for your clients. Here are some helpful articles and resources you could share with them to help answer some commonly asked questions.

Frequently asked questions

The construction option, also known as a building loan, is a lending option that releases funds to pay a Licensed Builder (or fund your client’s Owner-Builder project) throughout each stage of your client’s build or renovation process.

There are no progress draw fees or additional bank fees with our construction option. As for non-bank fees, your client may need to budget for the following, based on the complexity of their build:

A quantity surveyor report, if the valuer determines they need one.

For full details, check out our construction option guide (PDF 158KB) (PDF 438KB).

We’ll let your client and their builder know by issuing a ’Builders Pack’, containing the info and documents needed during the building phase of their new home or reno.

They let your client use their construction option to pay for specific stages of their build or reno, at various steps of completion. We only charge interest on the amount your client has drawn down, rather than the total construction option amount they’re approved for, which helps keep the cost of their construction option down.

There are various ways progress payments can be requested, all advised within the ‘Builders Pack’.

The final Progress Payment is subject to a satisfactory final inspection from our valuer, confirming the construction’s been completed as per the original plans and specs. You’ll also need a new building insurance policy and a full valuation to be done, along with the following relevant documents:

NSW: Updated Surveyor Report or Certificate of Currency

ACT, VIC, NT: Certificate of Occupancy and Completion

QLD: Completion and Occupancy

SA, WA, TAS: No additional documents

The building process is split into standard construction stages, here’s an example of a 5-stage schedule:

- Foundations/Slab – laying the foundation, levelling the ground, plumbing and waterproofing the foundation.

- Frame – building the frame, partial brickwork, the roofing, trusses and windows.

- Lockup – external walls, lockable windows and doors.

- Fitout – gutters, plumbing, electricity, plasterboards and the partial installation of cupboards.

- Practical completion/final stage – finishing touches, final plumbing, electricity, overall cleaning and final payments for equipment and builders.

At application:

Council approved plans and specifications (or, if not yet approved, a copy of those plans which have been, or are to be submitted to Council for approval).

Signed & dated building contract, including the building stages and schedule of payments

Variations/quotes, if applicable.

Quantity Surveyor Report if requested by the valuer.

Before settlement (drawdown):

Council approved plans and building specifications (if not already provided).

Builders Risk Insurance and a copy of the builder’s ‘Public Liability Insurance’.

Both can obtained from your client's builder.

If your client has equity in their property, they may be able to use it to increase their home loan, without using their to-be-constructed property as security. They might also be able to top up using equity they have in other investment properties or their block of land.

One potential downside is they’ll have to fully draw their home loan from the start. Unlike the construction option, which only charges interest on what they’ve drawn down, a top up will mean they’ll start paying interest on the whole loan at the outset.

If your client has a 100% offset account, they could move any not-yet-spent construction money over to offset this, but some extra costs might apply.

Fixed price contracts are designed to cap the budget on a construction (which are good for tight budgets).

Cost plus contracts involve trust between your client and their builder. They’ll generally agree on an hourly rate for tradies and their builders, and an extra percentage cost to order and schedule materials (also known as a builder’s margin). On one hand, they’ll have more control over expenditure decisions. On the other, as they near their budget, their builder can have less responsibility should costs overrun.

A non-structural renovation is a cosmetic upgrade, like laying floorboards or repainting the exterior or inside. Generally, the spend shouldn’t be any more than 10% of the home’s value.

A structural renovation’s a substantial change to the home, like moving walls, adding another level or adding an extension. Building codes differ between states and territories, there’s no real spending limit.

Yes. The construction option is available for construction or renos/home improvements using licensed builders (either fixed price or cost plus contracts), or by owner-builders. Includes kit homes, multiple dwellings, transportable homes and house/land packages.

A few years back, home buyers Susan and Mike bought a run-down yet perfectly liveable house on a block of land in the metro suburbs. Renting at the time, they planned on knocking down and rebuilding when they were ready to start a family. Well, that time had come. While checking out display homes and chatting to builders and architects, they realised they needed to talk money with lenders first.

Westpac offered a good interest rate with plenty of freedom, like flexible Progress Payments and Interest Only repayments during construction. They confirmed quotes, signed up their builder to manage the project, and with their $250,000 finance sorted, focused on the fun stuff: colour scheme, furniture and the nursery.

No matter how much planning you do, unexpected costs and delays are sometimes inevitable. So it helps for your clients to know regulations, the process and any tips before they start – check out the Australian Government’s yourhome site.

For a house and land package, the first drawdown would be for the land and subsequent progress draws would cover each stage of building your client’s home.

If your client is just buying land with no building contract, they can apply for a regular Westpac home loan without the construction option.

If they are looking to switch their existing land loan from another lender to Westpac, check out our Rates and Offer page for our current Refinance Cashback offers.

Check out our Construction Loan flyer which outlines the process for brokers and their clients.

The build must be complete 24 months from the date of the loan offer.

Your client’s full contribution is required at settlement.

Yes, they can include additional work in the loan application. I.e. Air Conditioning, Carpets, Landscaping.

Quotes of the additional work will need to be supplied at time of application so they can be included in the valuation of the proposed property.

Yes. If your client qualifies for the FHOG they may utilise it as part of their contribution and the build of their home.

Yes. If your client has signed a Verbal Payment Authority form, they can call our Progress Draw Payments team on 1300 367 483 and request payments as per the Builder’s schedule.

Yes, Owner Builders are able to borrow money to build a home. An Independent Adviser’s Inspection Report or Quantity Surveyor report is required for this type of build at each progress payment request.

We are increasing cash out for non-structural renovations from $100k to $250k for non LMI loans (approved).

Guides and Resources

Residential Construction Loans Guide

Are your clients renovating or building? This handy home loan option is structured around their build, with staged funding.

Residential Construction Loans Flyer

Westpac is here to help if your clients are building or renovating.

Things you should know

Credit Criteria, fees and charges apply. Terms and conditions available on request. Based on Westpac's credit criteria, residential lending is not available for Non-Australian Resident borrowers.

This information's been prepared without taking your clients objectives, needs and overall financial situation into account. For this reason, your client consider the appropriateness of the information and, if necessary, seek appropriate professional advice. This includes any tax consequences arising from any promotions for investors and customers should seek independent advice on any taxation matters.

If any of the information related to (or provided by) Westpac Group that you rely on is printed, downloaded or stored in any manner on your systems, files or otherwise, please ensure that you update your systems and files with the most up-to-date information provided by us and rely only on such updated information.

*Comparison rate: The comparison rate is based on a loan of $150,000 over the term of 25 years. WARNING: This comparison rate is true only for the examples given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

Also see Construction Option Guide FAQs (PDF 158KB) (PDF 438KB)

Westpac Banking Corporation ABN 33 007 457 141 AFSL and Australian credit licence 233714.